What is Global Medical Oxidized Cellulose Market?

The Global Medical Oxidized Cellulose Market is a specialized segment within the broader medical devices industry, focusing on the production and application of oxidized cellulose products. Oxidized cellulose is a chemically modified form of cellulose, which is a natural polymer derived from plant sources. This material is primarily used in the medical field for its hemostatic properties, meaning it helps to stop bleeding. When applied to a bleeding site, oxidized cellulose acts as a physical barrier and promotes clotting, making it an essential tool in surgical procedures. The market for oxidized cellulose is driven by the increasing demand for advanced wound care products and the rising number of surgical procedures worldwide. Additionally, the growing awareness of the benefits of using biodegradable and biocompatible materials in medical applications further fuels the market's growth. As healthcare systems continue to evolve and prioritize patient safety and recovery, the demand for effective hemostatic agents like oxidized cellulose is expected to rise, making this market a critical component of the global medical landscape.

Textile, Powder in the Global Medical Oxidized Cellulose Market:

In the Global Medical Oxidized Cellulose Market, textile and powder forms of oxidized cellulose are two primary product types that cater to different medical needs. Textile-based oxidized cellulose products are typically used in surgical settings as hemostatic agents. These textiles are woven or non-woven fabrics that can be applied directly to a bleeding site. They are designed to conform to the wound's shape, providing an effective barrier to control bleeding. The textile form is particularly useful in surgeries where precision and adaptability are crucial, such as in cardiovascular or orthopedic procedures. The fabric's structure allows it to absorb blood and fluids, facilitating clot formation and promoting healing. On the other hand, powder-based oxidized cellulose is used in situations where a more flexible application is needed. The powder form can be sprinkled over a bleeding area, making it ideal for irregular or hard-to-reach wounds. This form is often used in dental surgeries or minor surgical procedures where quick and efficient hemostasis is required. The powder's fine particles adhere to the wound surface, creating a matrix that supports clotting and reduces bleeding. Both textile and powder forms of oxidized cellulose are valued for their biocompatibility and biodegradability, ensuring they do not cause adverse reactions in patients. The choice between textile and powder forms depends on the specific medical scenario and the surgeon's preference. As the demand for minimally invasive procedures and advanced wound care solutions grows, the market for both forms of oxidized cellulose is expected to expand. Manufacturers are continually innovating to improve the efficacy and usability of these products, ensuring they meet the evolving needs of healthcare professionals and patients alike. The versatility and effectiveness of oxidized cellulose in various medical applications underscore its importance in the global medical market.

Surgery, Stomatology, Other in the Global Medical Oxidized Cellulose Market:

The usage of Global Medical Oxidized Cellulose Market products spans several critical areas, including surgery, stomatology, and other medical fields. In surgery, oxidized cellulose is primarily used as a hemostatic agent to control bleeding during and after procedures. Its ability to conform to different wound shapes and absorb fluids makes it an invaluable tool in complex surgeries, such as cardiovascular, orthopedic, and neurosurgical operations. Surgeons rely on oxidized cellulose to minimize blood loss, reduce the risk of complications, and enhance patient recovery. The material's biocompatibility ensures it integrates well with human tissue, reducing the likelihood of adverse reactions. In stomatology, or dental medicine, oxidized cellulose is used to manage bleeding during dental surgeries and extractions. The powder form is particularly popular in this field due to its ease of application and effectiveness in controlling bleeding in small, confined areas. Dentists use oxidized cellulose to ensure patient comfort and safety, promoting faster healing and reducing the risk of infection. Beyond surgery and stomatology, oxidized cellulose finds applications in other medical areas, such as wound care and gynecology. In wound care, it is used to manage chronic wounds, burns, and ulcers, providing a protective barrier that supports healing and prevents infection. In gynecology, oxidized cellulose is used during procedures like cesarean sections and hysterectomies to control bleeding and improve surgical outcomes. The material's versatility and effectiveness make it a valuable asset in various medical disciplines, contributing to improved patient care and outcomes. As the healthcare industry continues to advance, the demand for reliable and efficient hemostatic agents like oxidized cellulose is expected to grow, further solidifying its role in modern medicine.

Global Medical Oxidized Cellulose Market Outlook:

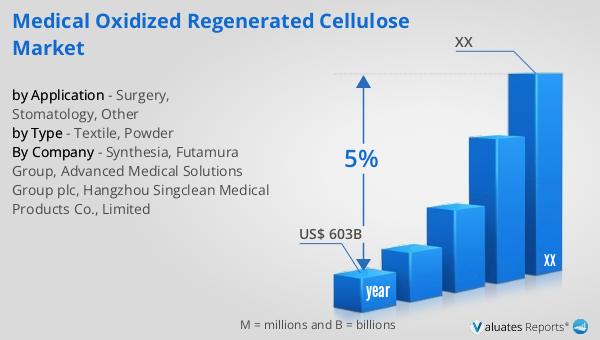

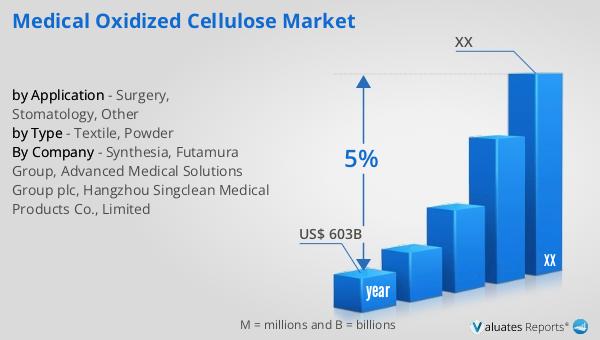

Based on our research, the global market for medical devices, which includes the Global Medical Oxidized Cellulose Market, is projected to reach approximately US$ 603 billion in 2023. This market is anticipated to experience a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, the rising number of surgical procedures, and the growing demand for advanced medical technologies. As healthcare systems worldwide strive to improve patient outcomes and reduce healthcare costs, the adoption of innovative medical devices, including oxidized cellulose products, is expected to rise. The market's expansion is also supported by technological advancements and the development of new materials that enhance the performance and safety of medical devices. Additionally, the increasing focus on minimally invasive procedures and personalized medicine is driving the demand for specialized medical products that cater to specific patient needs. As a result, the Global Medical Oxidized Cellulose Market is poised for significant growth, contributing to the overall expansion of the medical devices industry. This positive market outlook reflects the ongoing efforts of manufacturers, healthcare providers, and policymakers to enhance the quality and accessibility of healthcare services worldwide.

| Report Metric | Details |

| Report Name | Medical Oxidized Cellulose Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Synthesia, Futamura Group, Advanced Medical Solutions Group plc, Hangzhou Singclean Medical Products Co., Limited |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |