What is Global O-ring for Semiconductor Sealing Market?

The Global O-ring for Semiconductor Sealing Market is a specialized segment within the broader semiconductor industry, focusing on the production and application of O-rings used for sealing purposes in semiconductor manufacturing processes. O-rings are circular, elastomeric rings that serve as mechanical gaskets, providing a seal at the interface between two or more parts. In the semiconductor industry, these O-rings are crucial for maintaining the integrity of various processes by preventing leaks and contamination. They are used in equipment that handles gases, chemicals, and other materials essential for semiconductor fabrication. The demand for high-quality O-rings is driven by the need for precision and reliability in semiconductor manufacturing, where even the smallest contamination can lead to significant defects in the final product. As the semiconductor industry continues to grow, driven by advancements in technology and increasing demand for electronic devices, the market for O-rings in this sector is also expected to expand. This growth is further supported by the development of new materials and technologies that enhance the performance and durability of O-rings, making them more suitable for the demanding conditions of semiconductor manufacturing.

FFKM, FKM, FVMQ, VMQ, Others in the Global O-ring for Semiconductor Sealing Market:

In the Global O-ring for Semiconductor Sealing Market, several materials are commonly used to manufacture O-rings, each offering distinct properties that make them suitable for specific applications. FFKM, or perfluoroelastomer, is known for its exceptional chemical resistance and thermal stability, making it ideal for use in harsh environments where exposure to aggressive chemicals and high temperatures is common. This material is often used in processes that involve plasma or other reactive gases, as it can withstand the corrosive effects without degrading. FKM, or fluoroelastomer, is another popular material, valued for its excellent resistance to heat, chemicals, and oil. It is often used in applications where a balance between performance and cost is required, as it offers good durability at a more affordable price point compared to FFKM. FVMQ, or fluorosilicone rubber, combines the properties of silicone and fluoroelastomer, providing good resistance to fuels and oils while maintaining flexibility at low temperatures. This makes it suitable for applications where temperature fluctuations are a concern. VMQ, or silicone rubber, is known for its excellent thermal stability and flexibility, making it ideal for applications that require a wide operating temperature range. However, it is less resistant to chemicals compared to FFKM and FKM, so its use is typically limited to less aggressive environments. Other materials used in the production of O-rings for semiconductor sealing include EPDM (ethylene propylene diene monomer) and NBR (nitrile butadiene rubber), which offer good resistance to water and certain chemicals but may not perform as well in high-temperature or highly reactive environments. The choice of material for O-rings in the semiconductor industry depends on several factors, including the specific requirements of the application, the operating environment, and cost considerations. As the industry continues to evolve, there is ongoing research and development aimed at improving the performance of these materials, ensuring that they can meet the increasingly demanding requirements of semiconductor manufacturing processes.

Plasma Process, Thermal Process, Wet Chemical Process in the Global O-ring for Semiconductor Sealing Market:

The Global O-ring for Semiconductor Sealing Market plays a critical role in various semiconductor manufacturing processes, including plasma processes, thermal processes, and wet chemical processes. In plasma processes, O-rings are used to seal the chambers where plasma is generated and maintained. These processes involve the use of ionized gases to etch or deposit materials onto semiconductor wafers, and maintaining a stable environment is crucial for achieving precise results. O-rings made from materials like FFKM are often used in these applications due to their ability to withstand the corrosive effects of plasma and high temperatures. In thermal processes, such as oxidation and diffusion, O-rings are used to seal furnaces and other equipment where wafers are exposed to high temperatures. The primary function of the O-rings in these processes is to prevent the ingress of contaminants that could affect the quality of the wafers. Materials like VMQ and FKM are commonly used in thermal processes due to their excellent thermal stability and resistance to heat. In wet chemical processes, O-rings are used to seal equipment that handles various chemicals used for cleaning, etching, and developing semiconductor wafers. These processes require O-rings that can resist the corrosive effects of acids, bases, and solvents, making materials like FFKM and FVMQ suitable choices. The performance of O-rings in these applications is critical, as any failure in the sealing system can lead to contamination, equipment damage, and costly downtime. As semiconductor manufacturing becomes more advanced, the demand for high-performance O-rings that can meet the stringent requirements of these processes continues to grow. Manufacturers are constantly working to develop new materials and designs that enhance the durability and reliability of O-rings, ensuring that they can withstand the challenging conditions of semiconductor production.

Global O-ring for Semiconductor Sealing Market Outlook:

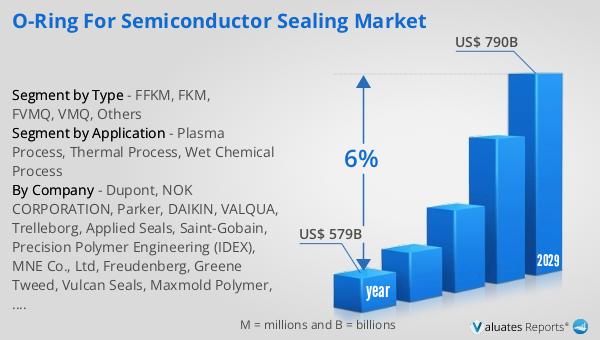

The global semiconductor market was valued at approximately $579 billion in 2022, and it is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for semiconductors across various industries, including consumer electronics, automotive, telecommunications, and industrial applications. As technology continues to advance, the need for more sophisticated and efficient semiconductor components is rising, leading to increased production and innovation within the industry. The expansion of the semiconductor market is also supported by the growing adoption of emerging technologies such as artificial intelligence, the Internet of Things (IoT), and 5G, which require advanced semiconductor solutions to function effectively. As a result, the demand for high-quality O-rings used in semiconductor manufacturing is expected to grow in tandem with the overall market. These O-rings are essential for ensuring the integrity and reliability of semiconductor production processes, as they prevent leaks and contamination that could compromise the quality of the final products. As the semiconductor industry continues to evolve, the Global O-ring for Semiconductor Sealing Market is poised to play a crucial role in supporting its growth and development.

| Report Metric | Details |

| Report Name | O-ring for Semiconductor Sealing Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Dupont, NOK CORPORATION, Parker, DAIKIN, VALQUA, Trelleborg, Applied Seals, Saint-Gobain, Precision Polymer Engineering (IDEX), MNE Co., Ltd, Freudenberg, Greene Tweed, Vulcan Seals, Maxmold Polymer, Ceetak, MITSUBISHI CABLE INDUSTRIES, MFC Sealing Technology, Shanghai Xinmi Technology, Northern Engineering (Sheffield) Ltd, Sigma Seals & Gaskets, AIR WATER MACH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |