What is Global Polyhydroxyalkanoate (PHA) for Rigid and Flexible Packaging Market?

Global Polyhydroxyalkanoate (PHA) for Rigid and Flexible Packaging Market is a fascinating area of study within the broader field of sustainable materials. PHAs are a family of biodegradable polymers produced by microbial fermentation of sugars or lipids. These materials have gained significant attention due to their potential to replace conventional plastics, which are often derived from non-renewable resources and contribute to environmental pollution. In the context of packaging, PHAs offer a promising alternative for both rigid and flexible applications. Rigid packaging refers to containers that maintain their shape, such as bottles and jars, while flexible packaging includes materials like films and bags that can easily change shape. The versatility of PHAs makes them suitable for a wide range of packaging needs, from food and beverage containers to personal care products. As consumers and industries alike become more environmentally conscious, the demand for sustainable packaging solutions like PHAs is expected to grow. This market is driven by the increasing awareness of environmental issues, regulatory pressures to reduce plastic waste, and technological advancements that make PHA production more cost-effective.

PHB-Poly(3-hydroxybutyrate), PHBV-poly(3-hydroxybutyrate-co-3-hydroxyvalerate), P34HB-poly(3-hydroxybutyrate-co-4-hydroxybutyrate), PHBHHxpoly(3-hydroxybutyrate-co-3-hydroxyhexanoate) in the Global Polyhydroxyalkanoate (PHA) for Rigid and Flexible Packaging Market:

PHB, or Poly(3-hydroxybutyrate), is one of the most well-known types of PHA and is often used in the packaging industry due to its biodegradability and physical properties that are similar to conventional plastics like polypropylene. PHB is produced by bacterial fermentation and is known for its high crystallinity, which gives it excellent mechanical strength and thermal stability. This makes it suitable for applications in rigid packaging where durability is essential. However, PHB can be brittle, which limits its use in flexible packaging applications. To overcome this limitation, copolymers like PHBV, P34HB, and PHBHHx have been developed. PHBV, or Poly(3-hydroxybutyrate-co-3-hydroxyvalerate), is a copolymer that incorporates 3-hydroxyvalerate units into the PHB chain. This modification reduces the crystallinity of the polymer, making it more flexible and less brittle than pure PHB. As a result, PHBV is more suitable for flexible packaging applications, such as films and bags, where flexibility and toughness are required. P34HB, or Poly(3-hydroxybutyrate-co-4-hydroxybutyrate), is another copolymer that enhances the flexibility of PHB by incorporating 4-hydroxybutyrate units. This copolymer is particularly useful in applications where a balance between rigidity and flexibility is needed, such as in semi-rigid packaging. PHBHHx, or Poly(3-hydroxybutyrate-co-3-hydroxyhexanoate), is a copolymer that includes 3-hydroxyhexanoate units, which further improve the flexibility and impact resistance of the material. This makes PHBHHx an excellent choice for flexible packaging applications that require high performance, such as in the packaging of delicate or high-value products. The development of these copolymers has expanded the range of applications for PHAs in the packaging industry, allowing them to compete more effectively with traditional plastics. As the technology for producing these materials continues to advance, it is likely that their use in both rigid and flexible packaging will increase, driven by the growing demand for sustainable and environmentally friendly packaging solutions.

Rigid Packaging, Flexible Packaging in the Global Polyhydroxyalkanoate (PHA) for Rigid and Flexible Packaging Market:

The usage of Global Polyhydroxyalkanoate (PHA) in the packaging industry is primarily divided into two categories: rigid packaging and flexible packaging. In rigid packaging, PHAs are used to create containers that maintain their shape and provide protection to the contents. This includes products like bottles, jars, and caps, which require materials that are strong, durable, and resistant to impact. PHAs are particularly well-suited for these applications due to their excellent mechanical properties and biodegradability. They offer a sustainable alternative to traditional plastics like PET and HDPE, which are commonly used in rigid packaging but are not biodegradable. The use of PHAs in rigid packaging is driven by the increasing demand for environmentally friendly packaging solutions, as well as regulatory pressures to reduce plastic waste. In flexible packaging, PHAs are used to create materials that can easily change shape, such as films, bags, and wraps. These applications require materials that are flexible, lightweight, and have good barrier properties to protect the contents from moisture, oxygen, and other environmental factors. PHAs are well-suited for these applications due to their flexibility and biodegradability. They offer a sustainable alternative to traditional flexible packaging materials like LDPE and PP, which are not biodegradable and contribute to environmental pollution. The use of PHAs in flexible packaging is driven by the growing demand for sustainable packaging solutions, as well as the increasing awareness of environmental issues among consumers and industries. As the technology for producing PHAs continues to advance, it is likely that their use in both rigid and flexible packaging will increase, driven by the growing demand for sustainable and environmentally friendly packaging solutions.

Global Polyhydroxyalkanoate (PHA) for Rigid and Flexible Packaging Market Outlook:

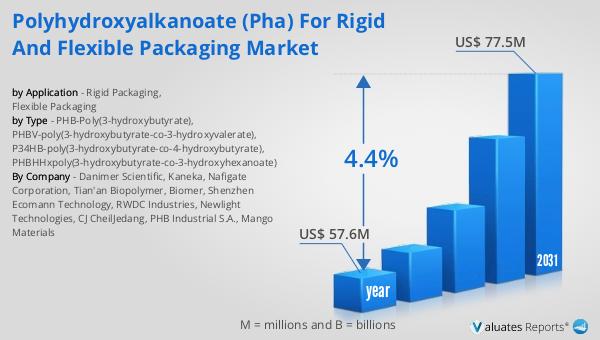

The global market for Polyhydroxyalkanoate (PHA) in the realm of rigid and flexible packaging is on a promising trajectory. In 2024, the market was valued at approximately US$ 57.6 million. Looking ahead, projections indicate that by 2031, the market is expected to expand to a revised size of US$ 77.5 million. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 4.4% over the forecast period. This upward trend reflects the increasing demand for sustainable packaging solutions as industries and consumers alike become more environmentally conscious. The shift towards biodegradable materials like PHA is driven by the need to reduce plastic waste and its impact on the environment. As regulatory pressures mount and technological advancements make PHA production more cost-effective, the market is poised for continued growth. The versatility of PHAs, which can be used in both rigid and flexible packaging applications, further enhances their appeal. As the market evolves, it is expected that PHAs will play an increasingly important role in the packaging industry, offering a sustainable alternative to traditional plastics.

| Report Metric | Details |

| Report Name | Polyhydroxyalkanoate (PHA) for Rigid and Flexible Packaging Market |

| Accounted market size in year | US$ 57.6 million |

| Forecasted market size in 2031 | US$ 77.5 million |

| CAGR | 4.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Danimer Scientific, Kaneka, Nafigate Corporation, Tian'an Biopolymer, Biomer, Shenzhen Ecomann Technology, RWDC Industries, Newlight Technologies, CJ CheilJedang, PHB Industrial S.A., Mango Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |