What is Global GaAs RF Switches Market?

The Global GaAs RF Switches Market refers to the worldwide industry focused on the production and sale of gallium arsenide (GaAs) radio frequency (RF) switches. These switches are integral components in various electronic devices, enabling the routing of RF signals between different paths. GaAs RF switches are favored for their high-speed performance, low insertion loss, and excellent isolation properties, making them ideal for applications requiring rapid signal switching and minimal signal degradation. The market encompasses a wide range of industries, including telecommunications, aerospace, defense, and consumer electronics, where these switches are used to enhance the performance and efficiency of RF systems. As technology advances and the demand for faster, more reliable wireless communication grows, the Global GaAs RF Switches Market is expected to expand, driven by innovations in semiconductor technology and the increasing adoption of RF solutions in emerging applications. The market's growth is also fueled by the rising need for advanced communication systems in various sectors, highlighting the importance of GaAs RF switches in modern electronic infrastructure.

Absorptive Type, Reflective Type in the Global GaAs RF Switches Market:

In the Global GaAs RF Switches Market, switches are primarily categorized into two types: absorptive and reflective. Absorptive RF switches, also known as matched switches, are designed to maintain a constant impedance across all ports, regardless of the switch's state. This characteristic ensures minimal signal reflection and distortion, making absorptive switches ideal for applications where signal integrity is paramount. They are commonly used in test and measurement equipment, where precise signal control is crucial. Absorptive switches are also favored in systems where the prevention of signal reflection is necessary to avoid interference with other components. On the other hand, reflective RF switches, also known as unmatched switches, do not maintain a constant impedance across all ports. Instead, they reflect the signal back to the source when the switch is in the off state. Reflective switches are typically used in applications where signal reflection is not a concern or can be managed effectively. They are often employed in simpler RF systems where cost and size are more critical than signal integrity. Reflective switches are generally more compact and cost-effective than absorptive switches, making them suitable for consumer electronics and other cost-sensitive applications. The choice between absorptive and reflective switches in the Global GaAs RF Switches Market depends on the specific requirements of the application, including factors such as signal integrity, cost, size, and complexity. As the demand for high-performance RF systems continues to grow, manufacturers are focusing on developing advanced GaAs RF switches that offer improved performance, reliability, and efficiency. This includes innovations in switch design, materials, and manufacturing processes to meet the evolving needs of various industries. The Global GaAs RF Switches Market is characterized by a diverse range of products, each tailored to meet the specific demands of different applications. This diversity is driven by the need for specialized solutions that can address the unique challenges of each industry. As a result, manufacturers are investing in research and development to create GaAs RF switches that offer superior performance, reliability, and cost-effectiveness. The market is also influenced by technological advancements in semiconductor manufacturing, which are enabling the production of smaller, more efficient, and more powerful GaAs RF switches. These advancements are helping to drive the adoption of GaAs RF switches in new and emerging applications, further expanding the market's reach. As the Global GaAs RF Switches Market continues to evolve, it is expected to play a critical role in the development of next-generation RF systems, supporting the growing demand for faster, more reliable wireless communication and advanced electronic devices.

Wireless Communications, Aerospace & Defense, Industrial & Automotive, Others in the Global GaAs RF Switches Market:

The Global GaAs RF Switches Market finds extensive usage across various sectors, including wireless communications, aerospace and defense, industrial and automotive, and others. In wireless communications, GaAs RF switches are crucial for enabling efficient signal routing in devices such as smartphones, tablets, and wireless routers. They help optimize the performance of these devices by ensuring rapid and reliable switching between different frequency bands and communication protocols. This is particularly important in the era of 5G and beyond, where the demand for high-speed, low-latency wireless communication is ever-increasing. In the aerospace and defense sector, GaAs RF switches are used in radar systems, satellite communications, and electronic warfare systems. Their ability to handle high-frequency signals with minimal loss and distortion makes them ideal for these applications, where precision and reliability are critical. In industrial and automotive applications, GaAs RF switches are used in various systems, including industrial automation, vehicle-to-everything (V2X) communication, and advanced driver-assistance systems (ADAS). These switches help improve the efficiency and performance of these systems by enabling seamless communication and data transfer. In other sectors, GaAs RF switches are used in medical devices, test and measurement equipment, and consumer electronics, where their high-speed performance and reliability are essential. The versatility and performance of GaAs RF switches make them a valuable component in a wide range of applications, driving their adoption across multiple industries. As technology continues to advance and the demand for high-performance RF systems grows, the Global GaAs RF Switches Market is expected to expand, offering new opportunities for innovation and growth.

Global GaAs RF Switches Market Outlook:

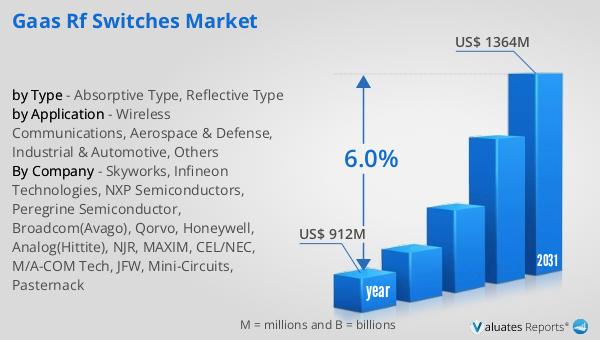

The global market for GaAs RF Switches was valued at $912 million in 2024 and is anticipated to grow to a revised size of $1,364 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.0% over the forecast period. This growth trajectory underscores the increasing demand for GaAs RF switches across various industries, driven by the need for advanced communication systems and high-performance electronic devices. The market's expansion is fueled by technological advancements in semiconductor manufacturing, which are enabling the production of more efficient and powerful GaAs RF switches. As industries continue to adopt these switches for their superior performance and reliability, the market is poised for significant growth. The projected increase in market size highlights the importance of GaAs RF switches in modern electronic infrastructure and their role in supporting the development of next-generation RF systems. As the demand for faster, more reliable wireless communication and advanced electronic devices continues to rise, the Global GaAs RF Switches Market is expected to play a critical role in meeting these needs, offering new opportunities for innovation and growth.

| Report Metric | Details |

| Report Name | GaAs RF Switches Market |

| Accounted market size in year | US$ 912 million |

| Forecasted market size in 2031 | US$ 1364 million |

| CAGR | 6.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Skyworks, Infineon Technologies, NXP Semiconductors, Peregrine Semiconductor, Broadcom(Avago), Qorvo, Honeywell, Analog(Hittite), NJR, MAXIM, CEL/NEC, M/A-COM Tech, JFW, Mini-Circuits, Pasternack |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |