What is Global Multimedia Integrated Circuit (Multimedia IC) Market?

The Global Multimedia Integrated Circuit (Multimedia IC) Market is a dynamic and rapidly evolving sector that plays a crucial role in the functioning of various electronic devices. Multimedia ICs are specialized semiconductor chips designed to handle multimedia data, including audio, video, and graphics. These integrated circuits are essential components in a wide range of consumer electronics, enabling devices to process and display multimedia content efficiently. The market for multimedia ICs is driven by the increasing demand for high-quality audio and video experiences in devices such as smartphones, tablets, televisions, and automotive infotainment systems. As technology advances, the need for more sophisticated and efficient multimedia processing capabilities continues to grow, leading to the development of more advanced multimedia ICs. These chips are designed to deliver enhanced performance, lower power consumption, and improved integration with other components, making them indispensable in the modern digital landscape. The global multimedia IC market is characterized by intense competition among key players, who are constantly innovating to meet the ever-changing demands of consumers and industries. As a result, the market is poised for significant growth, driven by the increasing adoption of multimedia-rich applications and the proliferation of connected devices.

Graphics IC, Audio IC in the Global Multimedia Integrated Circuit (Multimedia IC) Market:

Graphics ICs and Audio ICs are two critical components within the Global Multimedia Integrated Circuit (Multimedia IC) Market, each serving distinct yet complementary roles in the processing and delivery of multimedia content. Graphics ICs, also known as graphics processing units (GPUs), are specialized circuits designed to accelerate the rendering of images, animations, and video. They are essential for delivering high-quality visual experiences in devices such as smartphones, tablets, computers, and gaming consoles. The demand for advanced graphics ICs is driven by the increasing popularity of high-definition content, virtual reality, and augmented reality applications, which require powerful processing capabilities to deliver seamless and immersive experiences. Graphics ICs are designed to handle complex calculations and data processing tasks, enabling devices to render detailed and realistic images with minimal latency. As a result, they play a crucial role in enhancing the visual quality and performance of multimedia applications. On the other hand, Audio ICs are specialized circuits designed to process and deliver high-quality audio signals. They are used in a wide range of devices, including smartphones, tablets, televisions, and automotive infotainment systems, to provide clear and immersive sound experiences. Audio ICs are responsible for tasks such as audio signal conversion, amplification, and processing, ensuring that audio content is delivered with minimal distortion and maximum clarity. The demand for advanced audio ICs is driven by the increasing popularity of high-resolution audio content and the growing consumer preference for superior sound quality in electronic devices. As a result, manufacturers are continuously innovating to develop audio ICs that offer enhanced performance, lower power consumption, and improved integration with other components. In the context of the Global Multimedia Integrated Circuit (Multimedia IC) Market, both Graphics ICs and Audio ICs are essential for delivering high-quality multimedia experiences. They work together to ensure that devices can process and deliver rich and immersive audio-visual content, meeting the ever-growing demands of consumers and industries. The market for these components is characterized by rapid technological advancements and intense competition among key players, who are constantly striving to develop more efficient and powerful solutions. As the demand for multimedia-rich applications continues to grow, the importance of Graphics ICs and Audio ICs in the global multimedia IC market is expected to increase, driving further innovation and growth in the sector.

Set Top Box, Television, Automotive, Smart Phone, Tablet, Others in the Global Multimedia Integrated Circuit (Multimedia IC) Market:

The Global Multimedia Integrated Circuit (Multimedia IC) Market finds extensive applications across various sectors, including Set Top Boxes, Televisions, Automotive, Smartphones, Tablets, and others. In Set Top Boxes, multimedia ICs are crucial for decoding and processing digital signals, enabling the delivery of high-quality audio and video content to televisions. These integrated circuits ensure seamless streaming and playback of multimedia content, enhancing the viewing experience for consumers. As the demand for high-definition and on-demand content continues to rise, the role of multimedia ICs in Set Top Boxes becomes increasingly important, driving innovation and growth in this segment. In the realm of Televisions, multimedia ICs are essential for processing and displaying high-definition video and audio content. They enable televisions to deliver vibrant and lifelike images, as well as immersive sound experiences, meeting the growing consumer demand for superior audio-visual quality. With the advent of smart TVs and the increasing popularity of streaming services, the need for advanced multimedia ICs in televisions is more significant than ever. These integrated circuits play a vital role in enhancing the performance and functionality of modern televisions, making them indispensable components in the consumer electronics market. The Automotive sector also benefits significantly from the Global Multimedia Integrated Circuit (Multimedia IC) Market. In-vehicle infotainment systems rely on multimedia ICs to deliver high-quality audio and video content, providing passengers with an engaging and enjoyable experience. These integrated circuits enable features such as navigation, entertainment, and connectivity, enhancing the overall driving experience. As the automotive industry continues to evolve, with a focus on connected and autonomous vehicles, the demand for advanced multimedia ICs is expected to grow, driving further innovation and development in this sector. In Smartphones and Tablets, multimedia ICs are critical for delivering high-quality audio-visual experiences. They enable these devices to process and display high-definition video and audio content, supporting a wide range of applications, from streaming services to gaming and virtual reality. As consumers increasingly demand superior multimedia experiences on their mobile devices, the importance of multimedia ICs in smartphones and tablets continues to grow. These integrated circuits play a crucial role in enhancing the performance and functionality of mobile devices, making them essential components in the modern digital landscape. Beyond these specific applications, the Global Multimedia Integrated Circuit (Multimedia IC) Market also finds usage in various other sectors, including gaming consoles, wearable devices, and home entertainment systems. In each of these areas, multimedia ICs are essential for delivering high-quality audio-visual experiences, meeting the diverse needs and preferences of consumers. As technology continues to advance and the demand for multimedia-rich applications grows, the role of multimedia ICs in these sectors is expected to expand, driving further innovation and growth in the global multimedia IC market.

Global Multimedia Integrated Circuit (Multimedia IC) Market Outlook:

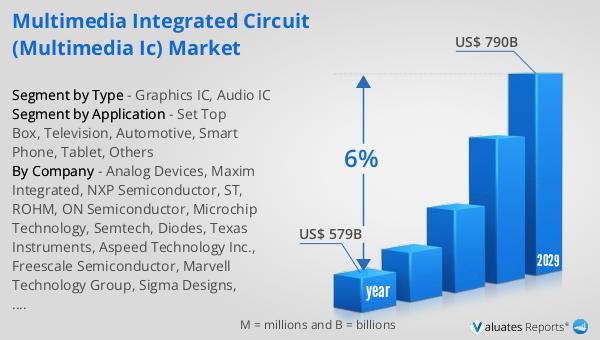

The global semiconductor market, which encompasses the Global Multimedia Integrated Circuit (Multimedia IC) Market, was valued at approximately $579 billion in 2022. This market is projected to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is indicative of the increasing demand for semiconductor components across various industries, driven by the proliferation of connected devices and the growing need for advanced processing capabilities. Semiconductors are the backbone of modern electronics, enabling the development of a wide range of applications, from consumer electronics to automotive and industrial systems. The projected growth of the semiconductor market highlights the critical role that these components play in the digital economy, as well as the ongoing innovation and development within the industry. As the demand for high-performance and energy-efficient semiconductor solutions continues to rise, the market is expected to witness significant advancements in technology and manufacturing processes. This growth trajectory underscores the importance of semiconductors in shaping the future of technology and driving economic development across the globe.

| Report Metric | Details |

| Report Name | Multimedia Integrated Circuit (Multimedia IC) Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Analog Devices, Maxim Integrated, NXP Semiconductor, ST, ROHM, ON Semiconductor, Microchip Technology, Semtech, Diodes, Texas Instruments, Aspeed Technology Inc., Freescale Semiconductor, Marvell Technology Group, Sigma Designs, Samsung, Apple, Broadcom |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |