What is Global Acute Kidney Injury Treatment & Management Market?

The Global Acute Kidney Injury (AKI) Treatment & Management Market is a specialized segment within the broader healthcare industry, focusing on the diagnosis, treatment, and management of acute kidney injury. AKI is a sudden episode of kidney failure or damage that happens within a few hours or days, causing waste products to build up in the blood and making it hard for the kidneys to maintain the right balance of fluid in the body. This market encompasses a range of products and services, including pharmaceuticals, medical devices, and therapeutic procedures aimed at restoring kidney function and preventing further damage. The market is driven by factors such as the increasing prevalence of chronic diseases like diabetes and hypertension, which are major risk factors for AKI, as well as advancements in medical technology and a growing awareness of kidney health. Healthcare providers, including hospitals and clinics, are key players in this market, utilizing various treatment modalities to manage AKI effectively. The market is also influenced by regulatory policies, healthcare infrastructure, and the availability of skilled healthcare professionals. Overall, the Global Acute Kidney Injury Treatment & Management Market plays a crucial role in improving patient outcomes and reducing the burden of kidney-related diseases worldwide.

Prerenal Acute Kidney Injury, Intrinsic Renal Acute Kidney Injury, Postrenal Acute Kidney Injury in the Global Acute Kidney Injury Treatment & Management Market:

Prerenal Acute Kidney Injury (AKI) is one of the primary types of AKI, characterized by a decrease in blood flow to the kidneys, which can lead to impaired kidney function. This condition is often caused by factors such as dehydration, heart failure, or significant blood loss, which reduce the volume of blood reaching the kidneys. In the Global Acute Kidney Injury Treatment & Management Market, prerenal AKI is addressed through interventions that aim to restore adequate blood flow and volume to the kidneys. Treatment strategies may include fluid replacement therapy, medications to improve heart function, and measures to control blood pressure. The market for prerenal AKI management is driven by the need for rapid diagnosis and intervention to prevent progression to more severe kidney damage. Intrinsic Renal Acute Kidney Injury, on the other hand, involves direct damage to the kidneys themselves, often due to conditions such as acute tubular necrosis, glomerulonephritis, or exposure to nephrotoxic drugs. The treatment and management of intrinsic renal AKI within the global market focus on identifying and addressing the underlying cause of kidney damage. This may involve discontinuing harmful medications, administering corticosteroids or other immunosuppressive agents, and providing supportive care to maintain kidney function. The market for intrinsic renal AKI management is influenced by advancements in diagnostic techniques and the development of targeted therapies that address specific causes of kidney injury. Postrenal Acute Kidney Injury occurs when there is an obstruction in the urinary tract that prevents urine from leaving the kidneys, leading to increased pressure and potential kidney damage. Common causes of postrenal AKI include kidney stones, tumors, or an enlarged prostate. The Global Acute Kidney Injury Treatment & Management Market addresses postrenal AKI through interventions aimed at relieving the obstruction and restoring normal urine flow. This may involve surgical procedures, the use of catheters, or medications to reduce prostate size. The market for postrenal AKI management is driven by the need for timely intervention to prevent permanent kidney damage and the development of innovative techniques to address urinary tract obstructions. Overall, the Global Acute Kidney Injury Treatment & Management Market encompasses a wide range of products and services tailored to the specific needs of patients with prerenal, intrinsic renal, and postrenal AKI. The market is characterized by ongoing research and development efforts aimed at improving diagnostic accuracy, expanding treatment options, and enhancing patient outcomes. As the understanding of AKI continues to evolve, the market is expected to adapt and grow, providing healthcare providers with the tools and resources needed to effectively manage this complex condition.

Hospitals, Ambulatory Surgical Centers, Others in the Global Acute Kidney Injury Treatment & Management Market:

The Global Acute Kidney Injury Treatment & Management Market plays a vital role in various healthcare settings, including hospitals, ambulatory surgical centers, and other medical facilities. In hospitals, the management of acute kidney injury is a critical component of patient care, particularly in intensive care units where patients are at a higher risk of developing AKI due to severe illness or complex medical procedures. Hospitals utilize a range of diagnostic tools, such as blood tests and imaging studies, to identify AKI early and implement appropriate treatment strategies. These may include fluid management, dialysis, and the use of medications to support kidney function. The market for AKI treatment in hospitals is driven by the need for comprehensive care and the availability of advanced medical technologies that facilitate early detection and intervention. Ambulatory surgical centers also contribute to the Global Acute Kidney Injury Treatment & Management Market by providing outpatient care for patients undergoing surgical procedures that may pose a risk of AKI. These centers focus on minimizing the risk of kidney injury through careful preoperative assessment and postoperative monitoring. The market for AKI management in ambulatory surgical centers is influenced by the growing trend towards outpatient surgeries and the need for efficient, cost-effective care. In addition to hospitals and ambulatory surgical centers, other healthcare facilities, such as dialysis centers and specialized kidney clinics, play a significant role in the Global Acute Kidney Injury Treatment & Management Market. These facilities provide targeted care for patients with AKI, offering services such as dialysis, nutritional counseling, and ongoing monitoring of kidney function. The market for AKI treatment in these settings is driven by the increasing prevalence of kidney disease and the demand for specialized care that addresses the unique needs of patients with acute kidney injury. Overall, the Global Acute Kidney Injury Treatment & Management Market is integral to the delivery of high-quality healthcare across various settings, ensuring that patients receive timely and effective treatment for this potentially life-threatening condition.

Global Acute Kidney Injury Treatment & Management Market Outlook:

The global pharmaceutical market was valued at approximately 1,475 billion USD in 2022, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth trajectory highlights the expanding demand for pharmaceutical products and innovations in healthcare. In comparison, the chemical drug market has shown a steady increase, growing from 1,005 billion USD in 2018 to an estimated 1,094 billion USD in 2022. This growth in the chemical drug sector underscores the ongoing importance of traditional pharmaceuticals within the broader market landscape. The expansion of these markets is driven by several factors, including advancements in drug development, increasing prevalence of chronic diseases, and a growing global population that requires diverse healthcare solutions. Additionally, the rise of personalized medicine and biotechnology is contributing to the evolution of the pharmaceutical industry, offering new opportunities for growth and innovation. As the market continues to evolve, stakeholders across the healthcare spectrum are poised to benefit from the increased availability and accessibility of pharmaceutical products, ultimately enhancing patient care and outcomes worldwide.

| Report Metric | Details |

| Report Name | Acute Kidney Injury Treatment & Management Market |

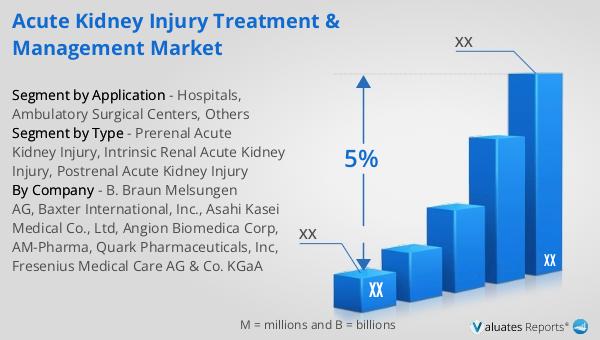

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | B. Braun Melsungen AG, Baxter International, Inc., Asahi Kasei Medical Co., Ltd, Angion Biomedica Corp, AM-Pharma, Quark Pharmaceuticals, Inc, Fresenius Medical Care AG & Co. KGaA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |