What is Global Automotive Seat Belt Retractor Market?

The Global Automotive Seat Belt Retractor Market is a crucial segment within the automotive industry, focusing on the development and production of seat belt retractors. These retractors are essential components of a vehicle's safety system, designed to secure passengers by locking the seat belt in place during sudden stops or collisions. The market encompasses a wide range of retractors, including emergency locking retractors, automatic locking retractors, and switchable retractors, each serving specific functions to enhance passenger safety. As automotive safety regulations become more stringent worldwide, the demand for advanced seat belt retractors is on the rise. Manufacturers are investing in research and development to innovate and improve the functionality and reliability of these devices. The market is also influenced by the increasing production of vehicles globally, as well as the growing awareness among consumers about the importance of vehicle safety features. As a result, the Global Automotive Seat Belt Retractor Market is poised for significant growth, driven by technological advancements and the continuous evolution of safety standards in the automotive sector.

Emergency Locking Retractors, Automatic Locking Retractors, Switchable Retractors in the Global Automotive Seat Belt Retractor Market:

Emergency Locking Retractors (ELRs) are a vital component of the Global Automotive Seat Belt Retractor Market. These retractors are designed to lock the seat belt in place during sudden stops or collisions, preventing passengers from being thrown forward. ELRs operate by using a sensor that detects rapid deceleration, triggering the locking mechanism. This type of retractor is commonly used in passenger vehicles, providing an essential layer of safety for occupants. Automatic Locking Retractors (ALRs), on the other hand, are designed to lock the seat belt at a specific length, ensuring that it remains tight and secure. ALRs are particularly useful for securing child safety seats, as they prevent the seat belt from loosening over time. This feature is crucial for maintaining the safety of young passengers, who require additional protection. Switchable Retractors offer the flexibility of both ELR and ALR functions, allowing users to switch between modes depending on their needs. This versatility makes switchable retractors a popular choice for a wide range of vehicles, as they can accommodate different passenger requirements. The development and production of these retractors are influenced by various factors, including technological advancements, regulatory requirements, and consumer preferences. Manufacturers are continually innovating to enhance the performance and reliability of these devices, ensuring that they meet the evolving safety standards in the automotive industry. The demand for advanced retractors is also driven by the increasing production of vehicles worldwide, as well as the growing awareness among consumers about the importance of vehicle safety features. As a result, the Global Automotive Seat Belt Retractor Market is expected to experience significant growth, with manufacturers focusing on developing retractors that offer enhanced safety, comfort, and convenience for passengers.

Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles in the Global Automotive Seat Belt Retractor Market:

The usage of Global Automotive Seat Belt Retractor Market products varies across different types of vehicles, including passenger vehicles, light commercial vehicles, and heavy commercial vehicles. In passenger vehicles, seat belt retractors play a crucial role in ensuring the safety of occupants. These vehicles are equipped with advanced retractors that provide both comfort and security, adapting to the needs of different passengers. The retractors are designed to lock the seat belt in place during sudden stops or collisions, preventing passengers from being thrown forward. This feature is essential for protecting occupants in the event of an accident, reducing the risk of injury. In light commercial vehicles, seat belt retractors are equally important, as these vehicles are often used for transporting goods and passengers. The retractors ensure that both the driver and passengers are securely fastened, minimizing the risk of injury in the event of a collision. Additionally, the retractors help to keep cargo secure, preventing it from shifting during transit. In heavy commercial vehicles, such as trucks and buses, seat belt retractors are designed to withstand the demands of long-distance travel and heavy loads. These retractors are built to provide maximum safety and durability, ensuring that drivers and passengers are protected during their journeys. The retractors are also designed to accommodate the unique needs of commercial drivers, who may require additional comfort and support during long hours on the road. Overall, the Global Automotive Seat Belt Retractor Market plays a vital role in enhancing the safety and security of vehicles across different segments, contributing to the overall safety of road users.

Global Automotive Seat Belt Retractor Market Outlook:

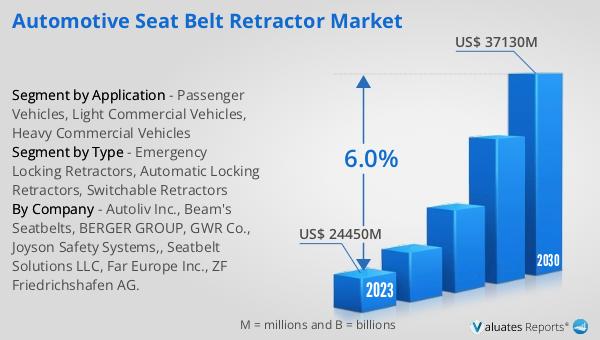

The global Automotive Seat Belt Retractor market is anticipated to witness substantial growth over the coming years. Starting from a valuation of approximately US$ 26,110 million in 2024, the market is expected to reach around US$ 37,130 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 6.0% during the forecast period. The increase in market size can be attributed to several factors, including the rising production of vehicles globally and the growing emphasis on vehicle safety features. As safety regulations become more stringent worldwide, manufacturers are compelled to enhance the safety features of their vehicles, including the integration of advanced seat belt retractors. Additionally, consumer awareness regarding the importance of vehicle safety is on the rise, further driving the demand for reliable and efficient seat belt retractors. The market's growth is also supported by technological advancements in the automotive industry, which have led to the development of innovative retractors that offer improved performance and reliability. As a result, the Global Automotive Seat Belt Retractor Market is poised for significant expansion, with manufacturers focusing on meeting the evolving safety standards and consumer preferences in the automotive sector.

| Report Metric | Details |

| Report Name | Automotive Seat Belt Retractor Market |

| Accounted market size in 2024 | US$ 26110 million |

| Forecasted market size in 2030 | US$ 37130 million |

| CAGR | 6.0 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Autoliv Inc., Beam's Seatbelts, BERGER GROUP, GWR Co., Joyson Safety Systems,, Seatbelt Solutions LLC, Far Europe Inc., ZF Friedrichshafen AG. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |