What is Global Ultra Precision Lathe (UPL) Market?

The Global Ultra Precision Lathe (UPL) Market is a specialized segment within the broader machine tool industry, focusing on lathes that offer extremely high precision in machining tasks. These lathes are designed to produce components with very tight tolerances and superior surface finishes, making them essential in industries where precision is paramount. The UPL market caters to sectors such as aerospace, automotive, electronics, and medical devices, where the demand for high-quality, precision-engineered parts is ever-increasing. The market is driven by technological advancements that enhance the capabilities of these machines, allowing for more complex and intricate designs. Additionally, the growing trend towards miniaturization in various industries has further fueled the demand for ultra-precision lathes. As industries continue to push the boundaries of what is possible with precision engineering, the UPL market is expected to see sustained growth, driven by the need for innovation and efficiency in manufacturing processes. The market's expansion is also supported by the increasing adoption of automation and digital technologies, which enhance the performance and versatility of ultra-precision lathes.

Single-spindle Type, Multi-spindle Type in the Global Ultra Precision Lathe (UPL) Market:

In the Global Ultra Precision Lathe (UPL) Market, there are two primary types of machines: single-spindle and multi-spindle lathes. Single-spindle lathes are designed with one spindle, which holds and rotates the workpiece while various cutting tools perform the machining operations. These machines are ideal for producing high-precision components in smaller quantities, as they offer greater control and flexibility in the machining process. Single-spindle lathes are often used in industries where the production of complex, custom parts is required, such as in aerospace and medical device manufacturing. They are known for their ability to produce parts with exceptional accuracy and surface finish, making them indispensable in applications where precision is critical. On the other hand, multi-spindle lathes are equipped with multiple spindles, allowing them to perform simultaneous machining operations on different workpieces. This capability significantly increases production efficiency and throughput, making multi-spindle lathes ideal for high-volume manufacturing environments. Industries such as automotive and electronics, where large quantities of precision parts are needed, often rely on multi-spindle lathes to meet their production demands. These machines are designed to handle complex machining tasks with speed and precision, reducing cycle times and increasing overall productivity. The choice between single-spindle and multi-spindle lathes depends largely on the specific requirements of the manufacturing process, including the complexity of the parts being produced, the desired production volume, and the level of precision needed. Both types of lathes play a crucial role in the UPL market, catering to the diverse needs of industries that demand high-quality, precision-engineered components. As technology continues to advance, both single-spindle and multi-spindle lathes are expected to evolve, offering even greater capabilities and efficiencies to manufacturers worldwide.

Automotive, Optical, Medical and Biotechnology, Mechanical, Electronics, Aerospace & Defense, Others in the Global Ultra Precision Lathe (UPL) Market:

The Global Ultra Precision Lathe (UPL) Market finds extensive applications across various industries, each with unique requirements for precision-engineered components. In the automotive sector, ultra-precision lathes are used to manufacture critical engine components, transmission parts, and other high-performance elements that require exact specifications and superior surface finishes. The demand for fuel-efficient and high-performance vehicles drives the need for precision machining, making UPLs indispensable in automotive manufacturing. In the optical industry, ultra-precision lathes are employed to produce lenses and other optical components with exceptional clarity and accuracy. The ability to achieve precise geometries and surface finishes is crucial in this sector, where even the slightest deviation can affect the performance of optical systems. The medical and biotechnology fields also rely heavily on ultra-precision lathes to produce intricate components for medical devices, implants, and laboratory equipment. The need for biocompatible materials and precise dimensions makes UPLs essential in ensuring the safety and efficacy of medical products. In the mechanical industry, ultra-precision lathes are used to create components for machinery and equipment that require high levels of accuracy and durability. The electronics industry benefits from UPLs in the production of micro-components and semiconductor devices, where precision is critical to ensure the functionality and reliability of electronic products. The aerospace and defense sectors utilize ultra-precision lathes to manufacture components for aircraft, spacecraft, and defense systems, where precision and reliability are paramount. Finally, other industries, such as telecommunications and energy, also leverage the capabilities of ultra-precision lathes to produce components that meet stringent quality and performance standards. The versatility and precision of UPLs make them a valuable asset across these diverse sectors, driving innovation and efficiency in manufacturing processes.

Global Ultra Precision Lathe (UPL) Market Outlook:

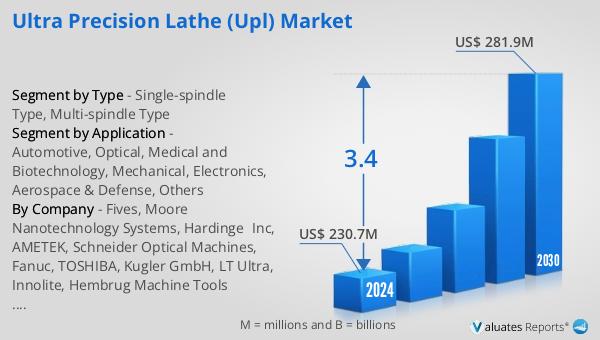

The outlook for the Global Ultra Precision Lathe (UPL) Market indicates a promising growth trajectory over the coming years. Starting from a valuation of approximately US$ 230.7 million in 2024, the market is anticipated to reach around US$ 281.9 million by 2030. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of 3.4% during the forecast period. The steady increase in market size reflects the rising demand for ultra-precision machining solutions across various industries. As sectors such as automotive, aerospace, electronics, and medical devices continue to evolve, the need for high-precision components becomes increasingly critical. This demand is further fueled by advancements in technology, which enhance the capabilities of ultra-precision lathes, allowing manufacturers to produce more complex and intricate parts with greater efficiency. Additionally, the trend towards automation and digitalization in manufacturing processes is expected to drive the adoption of ultra-precision lathes, as these machines offer enhanced performance and versatility. The market's growth is also supported by the increasing focus on quality and precision in manufacturing, as industries strive to meet stringent regulatory standards and customer expectations. Overall, the Global Ultra Precision Lathe (UPL) Market is poised for significant growth, driven by the continuous advancements in precision engineering and the expanding applications of ultra-precision lathes across various sectors.

| Report Metric | Details |

| Report Name | Ultra Precision Lathe (UPL) Market |

| Accounted market size in 2024 | US$ 230.7 million |

| Forecasted market size in 2030 | US$ 281.9 million |

| CAGR | 3.4 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Fives, Moore Nanotechnology Systems, Hardinge,Inc, AMETEK, Schneider Optical Machines, Fanuc, TOSHIBA, Kugler GmbH, LT Ultra, Innolite, Hembrug Machine Tools (Danobat), Mikrotools |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |