What is Global Vascular Interventional Apparatus Market?

The Global Vascular Interventional Apparatus Market refers to the worldwide industry focused on the development, production, and distribution of medical devices used in minimally invasive procedures to treat vascular diseases. These devices are crucial in managing conditions that affect the blood vessels, such as blockages, aneurysms, and other vascular disorders. The market encompasses a wide range of products, including stents, catheters, guidewires, and balloons, which are used by healthcare professionals to perform procedures that improve blood flow and reduce the risk of complications associated with vascular diseases. The demand for these devices is driven by the increasing prevalence of cardiovascular diseases, advancements in medical technology, and the growing preference for minimally invasive procedures over traditional surgical methods. As healthcare systems worldwide continue to focus on improving patient outcomes and reducing healthcare costs, the Global Vascular Interventional Apparatus Market is expected to experience significant growth, offering new opportunities for innovation and expansion in the medical device industry.

Cardiovascular Interventional Apparatus, Cerebrovascular Interventional Apparatus, Peripheral Vascular Interventional Devices in the Global Vascular Interventional Apparatus Market:

Cardiovascular Interventional Apparatus refers to medical devices specifically designed to address issues related to the heart and its surrounding blood vessels. These devices play a critical role in the treatment of cardiovascular diseases, which are among the leading causes of death globally. Common cardiovascular interventional devices include stents, which are used to keep arteries open; balloons, which help to widen narrowed blood vessels; and catheters, which are used to deliver treatments directly to the heart or blood vessels. These devices are often used in procedures such as angioplasty, where a balloon is inserted into a blocked artery and inflated to restore blood flow. The demand for cardiovascular interventional apparatus is driven by the increasing prevalence of heart diseases, advancements in medical technology, and the growing preference for minimally invasive procedures. Cerebrovascular Interventional Apparatus, on the other hand, focuses on the treatment of conditions affecting the blood vessels in the brain. These devices are used to manage conditions such as aneurysms, arteriovenous malformations, and strokes. Common cerebrovascular interventional devices include coils, which are used to block blood flow to an aneurysm; stents, which help to keep blood vessels open; and embolic protection devices, which are used to capture and remove debris during procedures. The demand for cerebrovascular interventional apparatus is driven by the increasing incidence of stroke and other cerebrovascular diseases, as well as advancements in imaging technology that allow for more precise and effective treatments. Peripheral Vascular Interventional Devices are used to treat conditions affecting the blood vessels outside of the heart and brain, such as those in the legs, arms, and abdomen. These devices are used to manage conditions such as peripheral artery disease, deep vein thrombosis, and varicose veins. Common peripheral vascular interventional devices include stents, balloons, and atherectomy devices, which are used to remove plaque from blood vessels. The demand for peripheral vascular interventional devices is driven by the increasing prevalence of peripheral vascular diseases, advancements in medical technology, and the growing preference for minimally invasive procedures. Overall, the Global Vascular Interventional Apparatus Market is characterized by a wide range of devices that are used to treat various vascular conditions, with each category of devices playing a critical role in improving patient outcomes and reducing the risk of complications associated with vascular diseases.

Hospital, Clinic, Others in the Global Vascular Interventional Apparatus Market:

The usage of Global Vascular Interventional Apparatus Market in hospitals is extensive, as these medical facilities are often the primary centers for performing complex vascular procedures. Hospitals are equipped with advanced medical technology and staffed by highly trained healthcare professionals, making them ideal settings for the use of vascular interventional devices. These devices are used in a variety of procedures, including angioplasty, stent placement, and thrombectomy, to treat conditions such as coronary artery disease, peripheral artery disease, and stroke. The availability of a wide range of vascular interventional devices in hospitals allows healthcare professionals to tailor treatments to the specific needs of each patient, improving outcomes and reducing the risk of complications. In clinics, the usage of vascular interventional apparatus is also significant, although the range of procedures performed may be more limited compared to hospitals. Clinics often focus on

| Report Metric | Details |

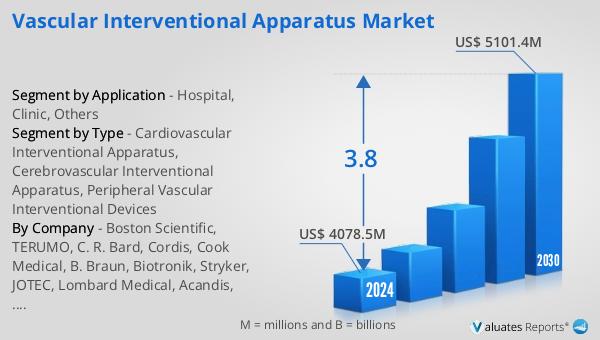

| Report Name | Vascular Interventional Apparatus Market |

| Accounted market size in 2024 | US$ 4078.5 million |

| Forecasted market size in 2030 | US$ 5101.4 million |

| CAGR | 3.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Boston Scientific, TERUMO, C. R. Bard, Cordis, Cook Medical, B. Braun, Biotronik, Stryker, JOTEC, Lombard Medical, Acandis, ELLA-CS, Balt, Concentric, Lepu Medical, MicroPort, LifeTech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |