What is Wrap Around Labeling Machine - Global Market?

The Wrap Around Labeling Machine is a crucial component in the global packaging industry, designed to apply labels around the circumference of cylindrical containers. These machines are widely used across various sectors, including food and beverage, pharmaceuticals, and chemicals, due to their efficiency and precision. The global market for Wrap Around Labeling Machines is driven by the increasing demand for packaged goods, which necessitates efficient labeling solutions. These machines offer several advantages, such as high-speed operation, accuracy, and the ability to handle different container sizes and shapes. As consumer preferences shift towards more aesthetically pleasing and informative packaging, the demand for advanced labeling solutions like wrap around labeling machines is expected to grow. Additionally, technological advancements in labeling machinery, such as the integration of automation and digital printing, are further propelling the market. The global market for these machines is characterized by a mix of established players and new entrants, all striving to innovate and capture a larger market share. As industries continue to expand and evolve, the need for efficient and versatile labeling solutions will likely sustain the growth of the Wrap Around Labeling Machine market.

Fully Automatic, Semi-automatic in the Wrap Around Labeling Machine - Global Market:

In the realm of Wrap Around Labeling Machines, the distinction between fully automatic and semi-automatic machines is significant, each catering to different operational needs and scales of production. Fully automatic wrap around labeling machines are designed for high-volume production environments where speed and precision are paramount. These machines are equipped with advanced features such as automated label application, container handling, and alignment systems, which minimize human intervention and maximize efficiency. They are ideal for large-scale manufacturers who require consistent labeling quality and high throughput. The integration of cutting-edge technologies, such as machine learning and IoT, in fully automatic machines allows for real-time monitoring and adjustments, ensuring optimal performance and reducing downtime. On the other hand, semi-automatic wrap around labeling machines are more suited for small to medium-sized enterprises or production lines where flexibility and cost-effectiveness are prioritized. These machines require some level of manual operation, such as loading and unloading containers, but still offer automated label application. Semi-automatic machines are often favored by businesses that produce a diverse range of products in smaller batches, as they allow for quick changeovers and adjustments. While they may not match the speed of fully automatic machines, semi-automatic machines provide a balance between efficiency and affordability, making them an attractive option for many businesses. The choice between fully automatic and semi-automatic wrap around labeling machines ultimately depends on the specific needs and resources of a business. Factors such as production volume, budget, and the complexity of labeling requirements play a crucial role in determining the most suitable option. As the global market for wrap around labeling machines continues to grow, manufacturers are increasingly offering customizable solutions to meet the diverse needs of their clients. This trend is likely to drive further innovation and competition in the market, as companies strive to develop machines that offer the best combination of speed, accuracy, and cost-effectiveness.

Pharmaceutical, Chemical, Food, Industry, Others in the Wrap Around Labeling Machine - Global Market:

Wrap Around Labeling Machines play a vital role in various industries, each with unique requirements and challenges. In the pharmaceutical industry, these machines are essential for ensuring that products are accurately labeled with critical information such as dosage instructions, expiration dates, and batch numbers. The precision and reliability of wrap around labeling machines help pharmaceutical companies comply with stringent regulatory standards and maintain product safety. In the chemical industry, where products often come in cylindrical containers, wrap around labeling machines provide a reliable solution for applying labels that withstand harsh environmental conditions. These machines ensure that labels remain intact and legible, even when exposed to chemicals or extreme temperatures. The food industry also benefits significantly from wrap around labeling machines, as they enable manufacturers to efficiently label a wide range of products, from beverages to canned goods. The ability to handle different container sizes and shapes makes these machines versatile and adaptable to the diverse needs of the food sector. Additionally, the demand for attractive and informative packaging in the food industry drives the need for advanced labeling solutions. Beyond these specific industries, wrap around labeling machines are used in various other sectors, including cosmetics, personal care, and household products. In these industries, the machines help companies enhance their brand image and provide consumers with essential product information. The versatility and efficiency of wrap around labeling machines make them an indispensable tool for businesses looking to improve their packaging processes and meet the evolving demands of consumers. As industries continue to innovate and expand, the role of wrap around labeling machines in ensuring efficient and accurate labeling will remain crucial.

Wrap Around Labeling Machine - Global Market Outlook:

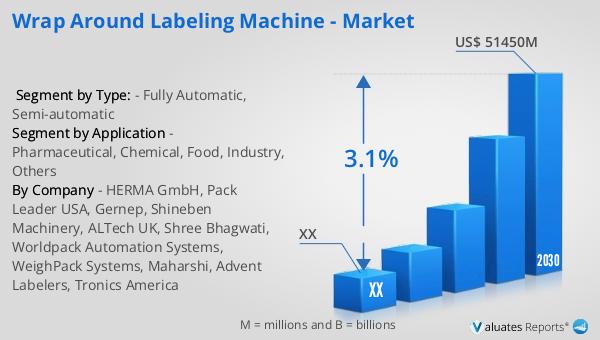

The global market for Wrap Around Labeling Machines was valued at approximately $41,270 million in 2023, with projections indicating a growth to around $51,450 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.1% during the forecast period from 2024 to 2030. The North American segment of this market was also assessed in 2023, although specific figures were not provided. However, it is anticipated to experience growth at a certain CAGR throughout the same forecast period. This market expansion is driven by the increasing demand for efficient and precise labeling solutions across various industries, including pharmaceuticals, chemicals, and food and beverage. The integration of advanced technologies, such as automation and digital printing, is further enhancing the capabilities of wrap around labeling machines, making them more attractive to manufacturers. As consumer preferences continue to evolve, the need for aesthetically pleasing and informative packaging is expected to sustain the demand for these machines. The competitive landscape of the global market for wrap around labeling machines is characterized by a mix of established players and new entrants, all striving to innovate and capture a larger market share. This dynamic environment is likely to drive further advancements in labeling technology, ensuring that the market remains robust and competitive in the coming years.

| Report Metric | Details |

| Report Name | Wrap Around Labeling Machine - Market |

| Forecasted market size in 2030 | US$ 51450 million |

| CAGR | 3.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | HERMA GmbH, Pack Leader USA, Gernep, Shineben Machinery, ALTech UK, Shree Bhagwati, Worldpack Automation Systems, WeighPack Systems, Maharshi, Advent Labelers, Tronics America |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |