What is Pharmaceutical Aseptic Filling Equipment - Global Market?

Pharmaceutical aseptic filling equipment is a crucial component in the global pharmaceutical industry, ensuring that medications are filled into containers in a sterile environment to prevent contamination. This equipment is designed to handle various forms of pharmaceuticals, including liquids, powders, and other formulations, maintaining their sterility throughout the filling process. The global market for this equipment is driven by the increasing demand for safe and effective medications, as well as the growing complexity of pharmaceutical formulations that require precise and sterile handling. Aseptic filling equipment is used extensively in the production of vaccines, biologics, and other sensitive drugs that must remain free from microbial contamination to ensure patient safety. The market is characterized by continuous technological advancements aimed at improving the efficiency, accuracy, and reliability of aseptic filling processes. As pharmaceutical companies strive to meet stringent regulatory standards and enhance their production capabilities, the demand for advanced aseptic filling equipment is expected to grow, making it a vital segment within the broader pharmaceutical manufacturing industry.

Fully Automatic, Semi-Automatic in the Pharmaceutical Aseptic Filling Equipment - Global Market:

In the realm of pharmaceutical aseptic filling equipment, the distinction between fully automatic and semi-automatic systems is significant, each offering unique advantages and applications. Fully automatic aseptic filling equipment is designed to operate with minimal human intervention, providing a high level of precision and efficiency. These systems are equipped with advanced robotics and automation technologies that enable them to handle large volumes of pharmaceutical products with consistent accuracy. Fully automatic systems are ideal for large-scale production environments where speed and precision are paramount. They are often integrated with other automated processes, such as sterilization and packaging, to create a seamless production line that minimizes the risk of contamination and human error. On the other hand, semi-automatic aseptic filling equipment requires some level of human involvement, typically in the setup and monitoring of the filling process. While they may not match the speed and efficiency of fully automatic systems, semi-automatic machines offer greater flexibility and are often more cost-effective for smaller production runs or specialized applications. These systems allow operators to make adjustments and oversee the filling process, which can be advantageous in situations where customization or frequent changes in production are required. Both fully automatic and semi-automatic systems play a crucial role in the pharmaceutical industry, catering to different production needs and helping manufacturers maintain the sterility and quality of their products. The choice between these systems often depends on factors such as production volume, budget, and the specific requirements of the pharmaceutical products being filled. As the global market for pharmaceutical aseptic filling equipment continues to evolve, manufacturers are increasingly seeking solutions that offer a balance between automation, flexibility, and cost-effectiveness. This has led to the development of hybrid systems that combine elements of both fully automatic and semi-automatic equipment, providing a versatile option for pharmaceutical companies looking to optimize their production processes. These hybrid systems are designed to offer the best of both worlds, allowing for high-speed production while still accommodating the need for customization and adaptability. As technology continues to advance, the line between fully automatic and semi-automatic systems is becoming increasingly blurred, with manufacturers striving to create equipment that meets the diverse needs of the pharmaceutical industry.

Liquid, Powder in the Pharmaceutical Aseptic Filling Equipment - Global Market:

Pharmaceutical aseptic filling equipment is essential for the sterile filling of both liquid and powder formulations, each presenting unique challenges and requirements. In the case of liquid pharmaceuticals, aseptic filling equipment must ensure that the liquid is transferred into containers without any microbial contamination. This is achieved through the use of advanced filtration systems, cleanroom environments, and precise filling mechanisms that maintain the sterility of the liquid throughout the process. Liquid aseptic filling equipment is commonly used for vaccines, injectable drugs, and other liquid medications that require strict adherence to sterility standards. The equipment is designed to handle various viscosities and volumes, providing flexibility for different types of liquid formulations. On the other hand, aseptic filling equipment for powders involves a different set of challenges, as powders can be more difficult to handle and require specialized equipment to ensure accurate dosing and sterility. Powder aseptic filling equipment is equipped with features such as vacuum systems, dust containment, and precise dosing mechanisms to prevent contamination and ensure the correct amount of powder is filled into each container. This type of equipment is often used for antibiotics, inhalable medications, and other powder-based pharmaceuticals that require aseptic processing. Both liquid and powder aseptic filling equipment are integral to the pharmaceutical industry, enabling manufacturers to produce safe and effective medications that meet regulatory standards. As the demand for complex and sensitive pharmaceutical formulations continues to grow, the need for advanced aseptic filling equipment that can handle both liquids and powders with precision and reliability is becoming increasingly important. Manufacturers are investing in research and development to create innovative solutions that address the unique challenges of aseptic filling for different types of pharmaceutical products. This includes the development of equipment that can seamlessly switch between liquid and powder filling, providing greater flexibility and efficiency for pharmaceutical companies. As the global market for pharmaceutical aseptic filling equipment expands, the focus on improving the capabilities and performance of these systems will remain a key priority for manufacturers and industry stakeholders.

Pharmaceutical Aseptic Filling Equipment - Global Market Outlook:

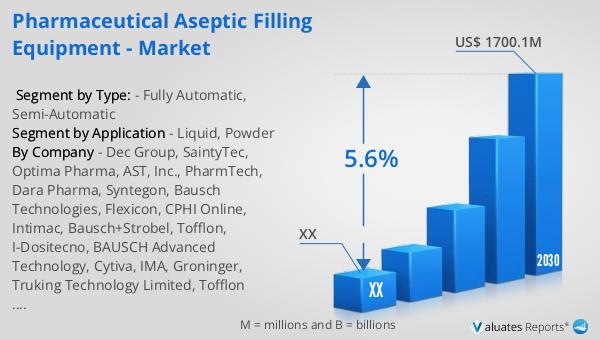

The global market for pharmaceutical aseptic filling equipment was valued at approximately $1,176 million in 2023 and is projected to grow to around $1,700.1 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.6% during the forecast period from 2024 to 2030. This growth is driven by the ongoing advancements and applications of aseptic packaging technology, which is increasingly being adopted across various industries, including pharmaceuticals, cosmetics, seasonings, and canned food. The demand for aseptic filling equipment is fueled by the need for safe and sterile packaging solutions that can preserve the integrity and efficacy of sensitive products. As industries continue to prioritize product safety and quality, the adoption of aseptic filling equipment is expected to rise, contributing to the market's expansion. The pharmaceutical sector, in particular, is a major driver of this growth, as the production of vaccines, biologics, and other sterile medications requires highly specialized equipment to ensure compliance with stringent regulatory standards. Additionally, the cosmetics and food industries are recognizing the benefits of aseptic packaging in extending shelf life and maintaining product quality, further boosting the demand for aseptic filling equipment. As a result, the global market for pharmaceutical aseptic filling equipment is poised for significant growth, driven by the increasing adoption of aseptic packaging technology across multiple sectors.

| Report Metric | Details |

| Report Name | Pharmaceutical Aseptic Filling Equipment - Market |

| Forecasted market size in 2030 | US$ 1700.1 million |

| CAGR | 5.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Dec Group, SaintyTec, Optima Pharma, AST, Inc., PharmTech, Dara Pharma, Syntegon, Bausch Technologies, Flexicon, CPHI Online, Intimac, Bausch+Strobel, Tofflon, I-Dositecno, BAUSCH Advanced Technology, Cytiva, IMA, Groninger, Truking Technology Limited, Tofflon Science and Technology Group Co.,Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |