What is Pigmented Lesion Treatment Laser - Global Market?

Pigmented Lesion Treatment Laser is a specialized technology used in the medical field to address skin conditions characterized by abnormal pigmentation. These lasers work by targeting melanin, the pigment responsible for skin color, and breaking it down, which helps in reducing the appearance of pigmented lesions such as age spots, freckles, and birthmarks. The global market for Pigmented Lesion Treatment Lasers is expanding due to increasing awareness about skin health and the rising demand for aesthetic treatments. Technological advancements have led to the development of more efficient and safer laser devices, which are driving their adoption across various regions. The market is also influenced by the growing prevalence of skin disorders and the increasing disposable income of consumers, which allows for more spending on cosmetic procedures. As more people seek non-invasive solutions for skin imperfections, the demand for these laser treatments is expected to continue growing. The market is characterized by a variety of products catering to different skin types and conditions, making it a versatile solution in the dermatological field.

Mobile, Fixed in the Pigmented Lesion Treatment Laser - Global Market:

The Pigmented Lesion Treatment Laser market can be broadly categorized into mobile and fixed systems, each serving distinct needs and settings. Mobile laser systems are designed for flexibility and convenience, allowing practitioners to move the equipment easily between different treatment rooms or even different locations. This portability is particularly beneficial for clinics that offer a wide range of services or for practitioners who provide on-site treatments at various locations. Mobile systems are often compact and lightweight, making them ideal for smaller practices or those with limited space. They are equipped with advanced features that ensure effective treatment while maintaining ease of use. On the other hand, fixed laser systems are typically found in larger medical facilities or specialized dermatology clinics. These systems are usually more robust and offer a higher level of precision and power, making them suitable for treating a broader range of pigmented lesions. Fixed systems are often integrated into a dedicated treatment room, providing a stable and controlled environment for procedures. They are designed to handle a higher volume of patients and can be equipped with additional features for enhanced performance. Both mobile and fixed systems are essential in the global market, catering to different segments of healthcare providers. The choice between mobile and fixed systems depends on various factors, including the size of the practice, the range of services offered, and the specific needs of the patient population. As the demand for pigmented lesion treatments continues to rise, both types of systems are expected to see increased adoption. The market is also witnessing innovations in laser technology, with manufacturers focusing on improving the efficacy, safety, and user-friendliness of their products. This includes the development of lasers that can target multiple types of pigmentation issues and those that offer faster treatment times with minimal discomfort. The competition in the market is driving companies to differentiate their products through unique features and capabilities, which is beneficial for consumers as it leads to better treatment options. Overall, the mobile and fixed segments of the Pigmented Lesion Treatment Laser market are integral to meeting the diverse needs of healthcare providers and patients worldwide.

Hospital, Specialist Clinic, Others in the Pigmented Lesion Treatment Laser - Global Market:

Pigmented Lesion Treatment Lasers are widely used in various healthcare settings, including hospitals, specialist clinics, and other facilities, each offering unique advantages and challenges. In hospitals, these lasers are part of a comprehensive dermatology department, where they are used to treat a wide range of skin conditions. Hospitals benefit from having a multidisciplinary team of healthcare professionals, which allows for a holistic approach to patient care. The availability of advanced diagnostic tools and the ability to manage complex cases make hospitals a preferred choice for patients with severe or multiple pigmented lesions. However, the high patient volume and the need for coordination among different departments can sometimes lead to longer waiting times for treatment. Specialist clinics, on the other hand, focus exclusively on dermatological treatments, providing a more personalized and specialized service. These clinics often have shorter waiting times and offer a more intimate setting for patients. The staff at specialist clinics are usually highly trained in the latest laser technologies and techniques, ensuring high-quality care. The focus on dermatology allows these clinics to stay updated with the latest advancements in laser treatments, offering patients access to cutting-edge technology. However, the cost of treatment at specialist clinics can be higher compared to hospitals, which may be a consideration for some patients. Other facilities, such as medical spas and cosmetic centers, also offer pigmented lesion treatments, often as part of a broader range of aesthetic services. These facilities cater to patients looking for non-medical cosmetic improvements and typically offer a more relaxed and luxurious environment. The emphasis on customer experience and satisfaction is high, with many facilities offering personalized treatment plans and follow-up care. However, the level of medical oversight in these settings may not be as comprehensive as in hospitals or specialist clinics, which could be a concern for patients with more complex skin conditions. Despite these differences, the common goal across all these settings is to provide effective and safe treatment for pigmented lesions, improving the skin's appearance and boosting patient confidence. The choice of facility often depends on the patient's specific needs, preferences, and budget, with each setting offering unique benefits that cater to different aspects of patient care.

Pigmented Lesion Treatment Laser - Global Market Outlook:

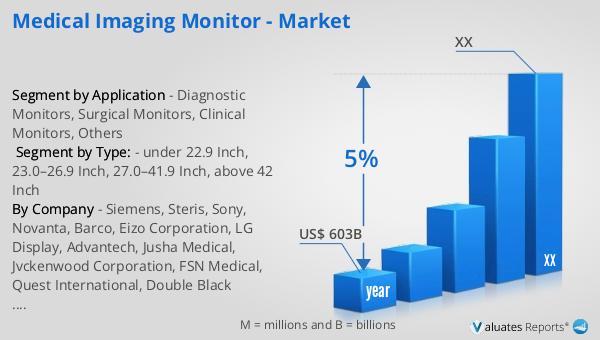

The global pharmaceutical market was valued at approximately 1,475 billion USD in 2022, and it is projected to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth reflects the increasing demand for pharmaceutical products worldwide, driven by factors such as an aging population, the prevalence of chronic diseases, and advancements in drug development. In comparison, the chemical drug market has shown a steady increase, rising from 1,005 billion USD in 2018 to an estimated 1,094 billion USD in 2022. This growth in the chemical drug sector highlights the ongoing importance of traditional pharmaceuticals in the global market, even as new therapies and biologics gain traction. The expansion of both markets underscores the dynamic nature of the pharmaceutical industry, where innovation and adaptation are key to meeting the evolving needs of patients and healthcare providers. As the industry continues to grow, companies are investing in research and development to bring new and improved treatments to market, addressing a wide range of health conditions and improving patient outcomes. The competitive landscape of the pharmaceutical market is characterized by a mix of established players and emerging companies, each striving to capture a share of this lucrative market.

| Report Metric | Details |

| Report Name | Pigmented Lesion Treatment Laser - Market |

| CAGR | 5% |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Advalight, Alma Lasers, AMT Engineering, Asclepion Laser Technologies, Beijing Nubway S and T Development, Beijing Sincoheren, Bison Medical, Blue-Moon, Bluecore Company, Candela Corporation, Cutera, Cynosure, DDC Technologies, Deka, Eufoton Medicalasers, Fotona |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |