What is Molybdenum-99 & Technetium-99m - Global Market?

Molybdenum-99 (Mo-99) and Technetium-99m (Tc-99m) are crucial isotopes in the field of nuclear medicine, playing a significant role in diagnostic imaging. Mo-99 is a parent isotope that decays to produce Tc-99m, which is widely used in medical imaging procedures. Tc-99m is favored for its ideal physical properties, including a short half-life of about six hours and the emission of gamma rays, which are suitable for imaging without causing excessive radiation exposure to patients. The global market for Mo-99 and Tc-99m is driven by the increasing demand for diagnostic imaging procedures, particularly in the detection and management of various diseases such as cancer and cardiovascular conditions. The market is characterized by a few key players who dominate the production and supply of these isotopes, ensuring their availability for medical use worldwide. The demand for Mo-99 and Tc-99m is expected to grow as healthcare systems continue to expand and the need for advanced diagnostic tools increases. This growth is supported by technological advancements in nuclear medicine and the ongoing development of new imaging techniques that rely on these isotopes. The market's expansion is also influenced by regulatory frameworks and initiatives aimed at ensuring the safe and efficient production and distribution of Mo-99 and Tc-99m.

Radioactive Source, Radiopharmaceutical in the Molybdenum-99 & Technetium-99m - Global Market:

Radioactive sources and radiopharmaceuticals based on Molybdenum-99 and Technetium-99m are integral to the global market, particularly in the realm of nuclear medicine. These isotopes are essential for creating radiopharmaceuticals used in diagnostic imaging and therapeutic procedures. Mo-99, as a parent isotope, decays to produce Tc-99m, which is the most widely used radioisotope in medical imaging. Tc-99m is employed in a variety of diagnostic tests, including bone scans, cardiac stress tests, and cancer detection, due to its favorable characteristics such as a short half-life and the emission of gamma rays suitable for imaging. The global market for these isotopes is driven by the increasing prevalence of chronic diseases, the aging population, and the growing demand for non-invasive diagnostic procedures. The production of Mo-99 is primarily carried out in nuclear reactors, and its supply chain is complex, involving multiple stages from production to distribution. The market is dominated by a few key players who ensure the availability of these isotopes for medical use worldwide. The demand for Mo-99 and Tc-99m is expected to grow as healthcare systems expand and the need for advanced diagnostic tools increases. This growth is supported by technological advancements in nuclear medicine and the ongoing development of new imaging techniques that rely on these isotopes. Regulatory frameworks and initiatives aimed at ensuring the safe and efficient production and distribution of Mo-99 and Tc-99m also influence the market's expansion. The market faces challenges such as the need for sustainable production methods, the management of radioactive waste, and the development of alternative isotopes to reduce reliance on nuclear reactors. Despite these challenges, the market for Mo-99 and Tc-99m continues to grow, driven by the increasing demand for diagnostic imaging procedures and the ongoing advancements in nuclear medicine. The future of the market will likely be shaped by innovations in production technologies, regulatory changes, and the development of new applications for these isotopes in medical and scientific research.

Medical, Santific Research, Others in the Molybdenum-99 & Technetium-99m - Global Market:

The usage of Molybdenum-99 and Technetium-99m in the global market spans several key areas, including medical applications, scientific research, and other sectors. In the medical field, Tc-99m is predominantly used for diagnostic imaging, making it an indispensable tool in nuclear medicine. It is employed in a wide range of procedures, such as bone scans, cardiac imaging, and cancer detection, due to its ideal properties, including a short half-life and the emission of gamma rays suitable for imaging. The demand for Tc-99m in medical imaging is driven by the increasing prevalence of chronic diseases, the aging population, and the growing need for non-invasive diagnostic procedures. In scientific research, Mo-99 and Tc-99m are used in various studies to understand biological processes and develop new diagnostic and therapeutic techniques. Researchers utilize these isotopes to investigate the behavior of different compounds in the body, study disease mechanisms, and evaluate the efficacy of new treatments. The use of Mo-99 and Tc-99m in research is supported by advancements in nuclear medicine and the development of new imaging technologies. Beyond medical and scientific applications, Mo-99 and Tc-99m are also used in other sectors, such as industrial radiography and environmental monitoring. In industrial radiography, these isotopes are used to inspect the integrity of materials and structures, ensuring safety and quality in various industries. In environmental monitoring, they are employed to track the movement of pollutants and study environmental processes. The global market for Mo-99 and Tc-99m is driven by the increasing demand for these isotopes in medical, scientific, and industrial applications. The market is characterized by a few key players who dominate the production and supply of these isotopes, ensuring their availability for various uses worldwide. The demand for Mo-99 and Tc-99m is expected to grow as healthcare systems expand, research activities increase, and the need for advanced diagnostic and monitoring tools rises. This growth is supported by technological advancements in nuclear medicine, the development of new applications for these isotopes, and regulatory frameworks that ensure their safe and efficient production and distribution.

Molybdenum-99 & Technetium-99m - Global Market Outlook:

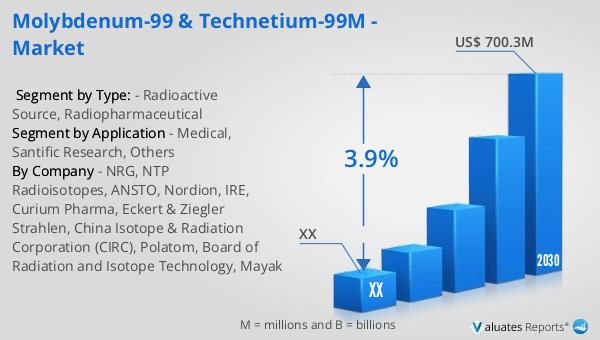

In 2023, the global market for Molybdenum-99 and Technetium-99m was valued at approximately $532.8 million, with projections indicating a growth to around $700.3 million by 2030. This growth represents a compound annual growth rate (CAGR) of 3.9% from 2024 to 2030. The market is primarily driven by a few major manufacturers, including NRG, IRE, and NTP, which collectively hold about 61% of the market share. North America emerges as the largest regional market, accounting for approximately 54% of the global share, followed by Europe and the Asia-Pacific region, which hold shares of about 23% and 20%, respectively. The predominant application of Mo-99 and Tc-99m is in medical imaging, which constitutes about 98% of the market's application share. This significant usage in medical imaging underscores the critical role these isotopes play in diagnostic procedures, particularly in detecting and managing various health conditions. The market's growth is fueled by the increasing demand for advanced diagnostic tools and the expansion of healthcare systems worldwide. As the market continues to evolve, it is expected to be shaped by technological advancements, regulatory changes, and the development of new applications for Mo-99 and Tc-99m in medical and scientific fields.

| Report Metric | Details |

| Report Name | Molybdenum-99 & Technetium-99m - Market |

| Forecasted market size in 2030 | US$ 700.3 million |

| CAGR | 3.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | NRG, NTP Radioisotopes, ANSTO, Nordion, IRE, Curium Pharma, Eckert & Ziegler Strahlen, China Isotope & Radiation Corporation (CIRC), Polatom, Board of Radiation and Isotope Technology, Mayak |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |