What is Polymer Flocculants - Global Market?

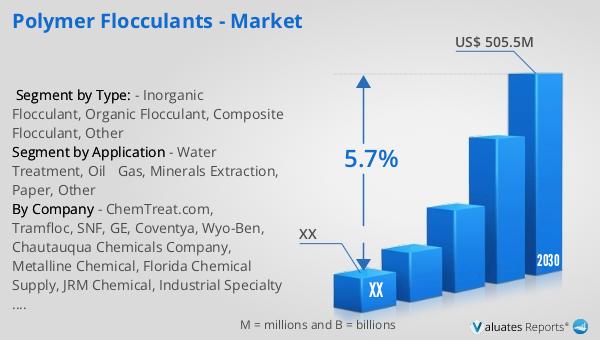

Polymer flocculants are specialized chemicals used to enhance the process of solid-liquid separation in various industries. These substances work by aggregating suspended particles in liquids, making them easier to remove. The global market for polymer flocculants is driven by the increasing demand for clean water and efficient waste management solutions. As industries expand and environmental regulations become stricter, the need for effective water treatment solutions grows. Polymer flocculants are particularly valued for their ability to improve the clarity of water and reduce the presence of contaminants. They are used in a variety of applications, including water treatment, oil and gas, mineral extraction, and paper manufacturing. The market is characterized by a diverse range of products, each tailored to specific industrial needs. As technology advances, the development of more efficient and environmentally friendly flocculants is expected to continue, further driving market growth. The global market for polymer flocculants was estimated to be worth US$ 344.8 million in 2023 and is projected to reach a size of US$ 505.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2024 to 2030.

Inorganic Flocculant, Organic Flocculant, Composite Flocculant, Other in the Polymer Flocculants - Global Market:

Inorganic flocculants are typically composed of metal salts such as aluminum sulfate and ferric chloride. These compounds are widely used due to their cost-effectiveness and efficiency in treating wastewater. Inorganic flocculants work by neutralizing the charges on suspended particles, allowing them to clump together and settle out of the liquid. They are particularly effective in removing heavy metals and other contaminants from industrial effluents. However, the use of inorganic flocculants can result in the production of large volumes of sludge, which can be a challenge to manage. Organic flocculants, on the other hand, are based on natural or synthetic polymers. These flocculants are often preferred for their ability to form larger and more stable flocs, which can be more easily removed from the liquid. Organic flocculants are used in a variety of applications, including municipal water treatment and the paper industry. They are also valued for their lower environmental impact compared to inorganic flocculants. Composite flocculants are a combination of inorganic and organic materials, designed to leverage the advantages of both types. These flocculants offer improved performance in terms of floc size and stability, making them suitable for challenging water treatment scenarios. The development of composite flocculants is an area of active research, with the aim of creating more efficient and sustainable solutions. Other types of polymer flocculants include those based on biopolymers, which are derived from natural sources such as plants and microorganisms. These flocculants are gaining attention for their biodegradability and potential to reduce the environmental impact of water treatment processes. As the global market for polymer flocculants continues to grow, the demand for innovative and sustainable solutions is expected to drive further advancements in this field.

Water Treatment, Oil &Gas, Minerals Extraction, Paper, Other in the Polymer Flocculants - Global Market:

Polymer flocculants play a crucial role in various industries by facilitating the separation of solids from liquids. In the water treatment sector, they are used to improve the clarity and quality of drinking water and to treat wastewater before it is discharged into the environment. Polymer flocculants help remove suspended solids, organic matter, and other contaminants, making the water safe for consumption and reducing the environmental impact of industrial effluents. In the oil and gas industry, polymer flocculants are used to treat produced water, which is a byproduct of oil and gas extraction. These flocculants help remove oil, grease, and other impurities from the water, allowing it to be reused or safely discharged. In mineral extraction, polymer flocculants are used to separate valuable minerals from the surrounding ore. They help improve the efficiency of the extraction process by enhancing the settling and dewatering of mineral slurries. In the paper industry, polymer flocculants are used to improve the retention of fibers and fillers, enhancing the quality and strength of the final product. They also help reduce the amount of water used in the papermaking process, contributing to more sustainable production practices. Other applications of polymer flocculants include food and beverage processing, where they are used to clarify liquids and improve product quality. As industries continue to seek more efficient and sustainable solutions, the demand for polymer flocculants is expected to grow, driving further innovation and development in this field.

Polymer Flocculants - Global Market Outlook:

The global market for polymer flocculants was valued at approximately US$ 344.8 million in 2023, with expectations to grow to around US$ 505.5 million by 2030. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 5.7% from 2024 to 2030. The North American market for polymer flocculants, although not specified in exact figures, is also projected to experience growth during this period. The increasing demand for effective water treatment solutions, driven by industrial expansion and stricter environmental regulations, is a key factor contributing to this market growth. As industries such as oil and gas, mineral extraction, and paper manufacturing continue to expand, the need for efficient and sustainable flocculant solutions is expected to rise. The development of new and improved polymer flocculants, including those based on biopolymers and composite materials, is likely to further drive market growth. As the global market for polymer flocculants evolves, companies are focusing on innovation and sustainability to meet the changing needs of their customers and to comply with environmental regulations. This focus on innovation is expected to result in the development of more efficient and environmentally friendly flocculant solutions, further supporting market growth.

| Report Metric | Details |

| Report Name | Polymer Flocculants - Market |

| Forecasted market size in 2030 | US$ 505.5 million |

| CAGR | 5.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | ChemTreat.com, Tramfloc, SNF, GE, Coventya, Wyo-Ben, Chautauqua Chemicals Company, Metalline Chemical, Florida Chemical Supply, JRM Chemical, Industrial Specialty Chemicals, Sabo Industrial, Polymer Ventures, SchmuCorp, Aqua Ben Corporation, Aquatic BioScience, Avista Technologies, QualiChem Incorporated, Integrated Engineers, Aquamark, Jayem Engineers |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |