What is Medical Grade RTV Silicone Adhesive - Global Market?

Medical Grade RTV Silicone Adhesive is a specialized adhesive used in the healthcare industry, known for its versatility and reliability. RTV stands for "Room Temperature Vulcanizing," which means this silicone adhesive cures at room temperature, making it convenient for various applications. This adhesive is particularly valued in the medical field due to its biocompatibility, flexibility, and resistance to extreme temperatures and chemicals. It is used in the manufacturing of medical devices, ensuring that components are securely bonded without compromising the safety or functionality of the device. The global market for Medical Grade RTV Silicone Adhesive is expanding as the demand for advanced medical devices increases. This growth is driven by the rising need for minimally invasive surgical procedures and the development of innovative medical technologies. As healthcare standards continue to rise globally, the demand for high-quality, reliable adhesives like Medical Grade RTV Silicone Adhesive is expected to grow, supporting the production of safer and more effective medical devices. This adhesive plays a crucial role in ensuring the durability and performance of medical equipment, making it an essential component in the healthcare industry.

Single Component Silicone Adhesive, Double Component Silicone Adhesive in the Medical Grade RTV Silicone Adhesive - Global Market:

Single Component Silicone Adhesive and Double Component Silicone Adhesive are two primary types of Medical Grade RTV Silicone Adhesives, each with distinct characteristics and applications. Single Component Silicone Adhesive is a ready-to-use adhesive that cures upon exposure to moisture in the air. This type of adhesive is particularly advantageous in medical applications due to its ease of use and quick curing time. It is often used in situations where speed and convenience are critical, such as in emergency repairs or quick assembly processes. The single component adhesive is ideal for bonding medical device components that require a strong, flexible bond without the need for mixing or additional curing agents. Its simplicity and efficiency make it a popular choice in the fast-paced medical environment. On the other hand, Double Component Silicone Adhesive requires mixing two separate components before application. This type of adhesive offers greater control over the curing process and can be tailored to specific requirements by adjusting the ratio of the components. Double Component Silicone Adhesive is often used in applications where a more precise and customizable bond is needed. It provides superior strength and durability, making it suitable for critical medical applications where reliability is paramount. This adhesive is commonly used in the assembly of complex medical devices that require a robust and long-lasting bond. The ability to customize the adhesive properties makes it an attractive option for manufacturers looking to meet specific performance criteria. Both Single and Double Component Silicone Adhesives are integral to the Medical Grade RTV Silicone Adhesive market, each serving unique purposes in the healthcare industry. The choice between the two depends on the specific requirements of the application, such as the need for speed, strength, or customization. As the global market for medical devices continues to grow, the demand for these adhesives is expected to rise, driven by the need for reliable and efficient bonding solutions. The versatility and performance of these adhesives make them indispensable in the production of medical devices, contributing to the advancement of healthcare technologies and improving patient outcomes.

Hospital, Clinic, Others in the Medical Grade RTV Silicone Adhesive - Global Market:

Medical Grade RTV Silicone Adhesive is widely used in various healthcare settings, including hospitals, clinics, and other medical facilities, due to its exceptional properties and versatility. In hospitals, this adhesive is crucial for the assembly and maintenance of medical devices and equipment. It is used in the production of devices such as catheters, respiratory masks, and surgical instruments, where a strong and reliable bond is essential. The adhesive's biocompatibility ensures that it does not cause adverse reactions when in contact with human tissue, making it safe for use in critical medical applications. Additionally, its resistance to sterilization processes, such as autoclaving, makes it ideal for use in hospital environments where hygiene and safety are paramount. In clinics, Medical Grade RTV Silicone Adhesive is used for a variety of applications, including the repair and maintenance of medical equipment. Its quick curing time and ease of use make it suitable for on-the-spot repairs, ensuring that equipment remains operational and minimizing downtime. This adhesive is also used in the assembly of diagnostic devices and tools, where precision and reliability are crucial. The flexibility and durability of the adhesive ensure that bonded components can withstand the rigors of daily use in a clinical setting, contributing to the overall efficiency and effectiveness of healthcare delivery. Beyond hospitals and clinics, Medical Grade RTV Silicone Adhesive finds applications in other areas of the healthcare industry. It is used in the production of wearable medical devices, such as fitness trackers and health monitors, where a secure and flexible bond is necessary to ensure comfort and functionality. The adhesive's ability to withstand environmental factors, such as moisture and temperature fluctuations, makes it suitable for use in these devices, which are often exposed to varying conditions. Additionally, it is used in the manufacturing of prosthetics and orthotics, where a strong and reliable bond is essential for the performance and longevity of the device. Overall, the use of Medical Grade RTV Silicone Adhesive in hospitals, clinics, and other healthcare settings highlights its importance in the medical industry. Its unique properties make it an indispensable tool for ensuring the safety, reliability, and effectiveness of medical devices and equipment. As the demand for advanced healthcare solutions continues to grow, the role of this adhesive in supporting the development and maintenance of medical technologies is expected to expand, contributing to improved patient care and outcomes.

Medical Grade RTV Silicone Adhesive - Global Market Outlook:

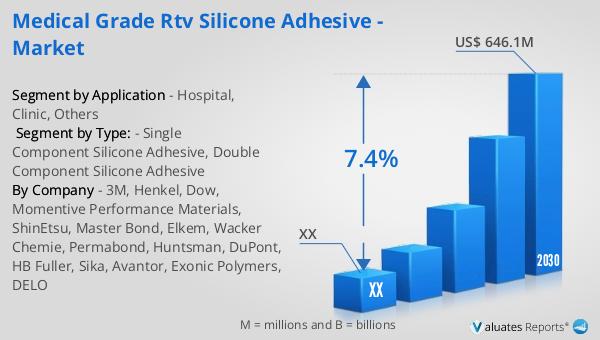

The global market for Medical Grade RTV Silicone Adhesive was valued at approximately US$ 379 million in 2023. It is projected to grow significantly, reaching an estimated size of US$ 646.1 million by 2030, with a compound annual growth rate (CAGR) of 7.4% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for high-quality adhesives in the medical industry, driven by advancements in medical technology and the rising need for reliable bonding solutions. In comparison, the global market for medical devices is estimated to be worth US$ 603 billion in 2023, with a projected CAGR of 5% over the next six years. This indicates a robust growth trajectory for both the adhesive and medical device markets, highlighting the critical role of Medical Grade RTV Silicone Adhesive in supporting the development and production of innovative medical technologies. As healthcare standards continue to rise globally, the demand for these adhesives is expected to increase, contributing to the overall growth of the medical industry. The expanding market for Medical Grade RTV Silicone Adhesive underscores its importance in ensuring the safety, reliability, and effectiveness of medical devices, ultimately enhancing patient care and outcomes.

| Report Metric | Details |

| Report Name | Medical Grade RTV Silicone Adhesive - Market |

| Forecasted market size in 2030 | US$ 646.1 million |

| CAGR | 7.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | 3M, Henkel, Dow, Momentive Performance Materials, ShinEtsu, Master Bond, Elkem, Wacker Chemie, Permabond, Huntsman, DuPont, HB Fuller, Sika, Avantor, Exonic Polymers, DELO |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |