What is CPU Card Chips - Global Market?

CPU card chips are a crucial component in the global market, serving as the brain of smart cards used in various applications. These chips are embedded in cards to provide secure data processing and storage capabilities. They are designed to handle complex computations and store sensitive information, making them ideal for applications that require high security and reliability. The global market for CPU card chips is driven by the increasing demand for secure and efficient payment systems, identification cards, and access control systems. With advancements in technology, these chips have become more powerful, enabling faster processing speeds and enhanced security features. The market is also influenced by the growing adoption of contactless payment systems, which require sophisticated chip technology to ensure secure transactions. As industries continue to digitize and prioritize security, the demand for CPU card chips is expected to rise, making them a vital component in the global semiconductor market.

Contact, Contactless in the CPU Card Chips - Global Market:

Contact and contactless technologies are two primary methods of interaction for CPU card chips in the global market. Contact-based CPU card chips require physical contact with a reader to function. These cards have a visible chip on the surface that must be inserted into a card reader to establish a connection. The reader then powers the chip and facilitates data exchange. This method is commonly used in credit and debit cards, where the card is inserted into a point-of-sale terminal to complete a transaction. Contact-based cards are known for their reliability and security, as the physical connection reduces the risk of data interception. However, they can be less convenient compared to contactless options, as they require precise alignment and insertion into a reader. On the other hand, contactless CPU card chips use radio frequency identification (RFID) or near-field communication (NFC) technology to communicate with a reader without physical contact. These cards have an embedded antenna that allows them to interact with a reader when brought within a certain proximity, usually a few centimeters. Contactless cards are widely used in public transportation systems, access control, and payment systems due to their convenience and speed. Users can simply tap or wave their card near a reader to complete a transaction, making them ideal for high-traffic environments where quick processing is essential. The adoption of contactless technology is growing rapidly, driven by the demand for faster and more convenient payment methods. Both contact and contactless CPU card chips offer distinct advantages and are chosen based on the specific requirements of the application. Contact-based cards are preferred in scenarios where security is paramount, and the risk of unauthorized access needs to be minimized. They are also favored in environments where the card needs to be physically retained, such as in ATMs. Contactless cards, however, are gaining popularity due to their ease of use and the seamless experience they offer to users. They are particularly beneficial in situations where speed and convenience are prioritized, such as in public transport systems and retail environments. The global market for CPU card chips is witnessing a shift towards contactless technology, driven by consumer demand for faster and more efficient payment solutions. This trend is supported by advancements in chip technology, which have improved the security and performance of contactless cards. As a result, many industries are transitioning from traditional contact-based systems to contactless solutions to enhance user experience and streamline operations. Despite the growing popularity of contactless technology, contact-based cards continue to hold a significant share of the market, particularly in applications where security and reliability are critical. The coexistence of both technologies in the market highlights the diverse needs of consumers and industries, ensuring that CPU card chips remain a vital component in the global semiconductor landscape.

Bus Card, Bank Card, Social Security Card, Access Card, Others in the CPU Card Chips - Global Market:

CPU card chips are utilized in various applications across the global market, including bus cards, bank cards, social security cards, access cards, and others. In the transportation sector, CPU card chips are embedded in bus cards to facilitate seamless and efficient fare collection. These cards allow passengers to quickly tap their card on a reader when boarding, deducting the fare automatically. This system not only speeds up the boarding process but also reduces the need for cash transactions, enhancing convenience for both passengers and operators. The use of CPU card chips in bus cards is particularly beneficial in urban areas with high passenger volumes, where quick and efficient fare collection is essential. In the banking sector, CPU card chips are a critical component of bank cards, including credit and debit cards. These chips provide enhanced security features, such as encryption and authentication, to protect sensitive financial information during transactions. The use of CPU card chips in bank cards has significantly reduced the risk of fraud and unauthorized access, making them a preferred choice for consumers and financial institutions alike. The chips enable secure communication between the card and the point-of-sale terminal, ensuring that transactions are processed safely and efficiently. Social security cards also benefit from the integration of CPU card chips, which enhance the security and functionality of these cards. By embedding a chip in social security cards, governments can store and manage sensitive personal information securely. This technology allows for the implementation of advanced security measures, such as biometric authentication, to verify the identity of cardholders. The use of CPU card chips in social security cards helps prevent identity theft and ensures that only authorized individuals can access social security benefits. Access cards are another area where CPU card chips are widely used. These cards are employed in various settings, including office buildings, hotels, and secure facilities, to control access to restricted areas. The chips enable secure communication between the card and the access control system, ensuring that only authorized individuals can enter specific areas. The use of CPU card chips in access cards enhances security and simplifies the management of access permissions, making them an essential tool for organizations seeking to protect their assets and personnel. Beyond these specific applications, CPU card chips are also used in a variety of other areas, such as loyalty cards, healthcare cards, and identification cards. In each of these applications, the chips provide secure data processing and storage capabilities, enabling organizations to offer enhanced services and improve operational efficiency. The versatility and security features of CPU card chips make them a valuable asset in the global market, driving their adoption across a wide range of industries. As technology continues to evolve, the use of CPU card chips is expected to expand, offering new opportunities for innovation and growth in the global market.

CPU Card Chips - Global Market Outlook:

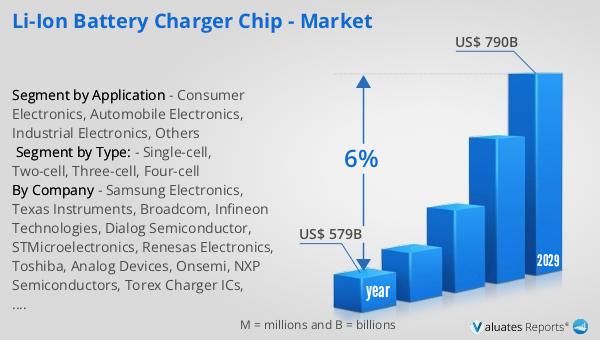

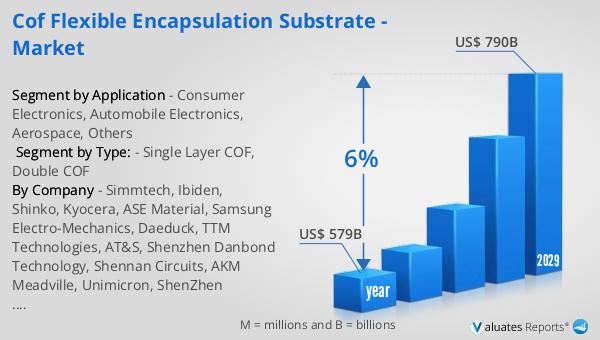

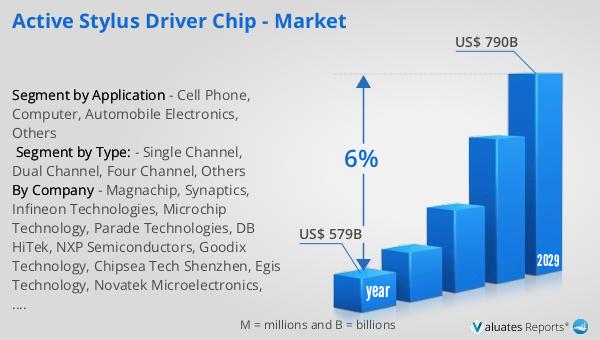

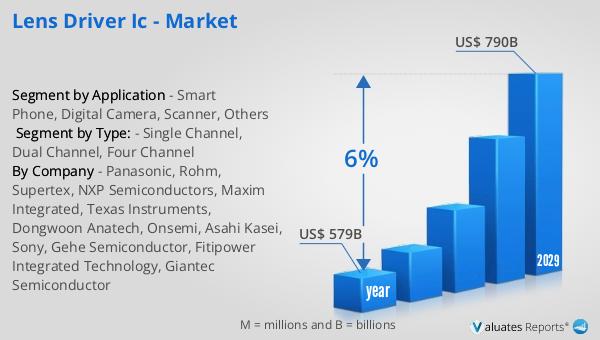

The semiconductor market, which includes CPU card chips, is experiencing significant growth. In 2022, the global market for semiconductors was valued at approximately $579 billion. This figure is projected to rise to $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for advanced semiconductor technologies across various industries, including consumer electronics, automotive, telecommunications, and healthcare. The rise in demand for smart devices, electric vehicles, and 5G technology is contributing to the expansion of the semiconductor market. Additionally, the growing focus on digital transformation and the Internet of Things (IoT) is further fueling the demand for semiconductors, as these technologies rely heavily on advanced chip solutions. The market's growth is also supported by continuous advancements in semiconductor manufacturing processes, which are enabling the production of more powerful and efficient chips. As industries continue to innovate and adopt new technologies, the demand for semiconductors, including CPU card chips, is expected to remain strong, driving further growth in the global market. This positive outlook highlights the critical role that semiconductors play in enabling technological advancements and shaping the future of various industries.

| Report Metric | Details |

| Report Name | CPU Card Chips - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | NXP Semiconductors, Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, Intel, Xilinx, Renesas, Mitsubishi, Unigroup Guoxin Microelectronics, Shanghai Fudan Microelectronics Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |