What is Active Stylus Driver Chip - Global Market?

The Active Stylus Driver Chip is a crucial component in the global market, primarily used in devices that require precise touch input, such as tablets, smartphones, and digital drawing pads. This chip enables the stylus to communicate effectively with the device, ensuring accurate and responsive input. As technology advances, the demand for more sophisticated and efficient stylus driver chips has increased, driving growth in this market. These chips are designed to support various functionalities, including pressure sensitivity, tilt recognition, and palm rejection, enhancing the user experience. The global market for active stylus driver chips is expanding as more industries adopt digital solutions that require precise input methods. This growth is fueled by the increasing popularity of digital art, note-taking applications, and the integration of stylus functionality in educational and professional settings. As a result, manufacturers are investing in research and development to produce chips that offer better performance, lower power consumption, and compatibility with a wide range of devices. The active stylus driver chip market is poised for significant growth as it continues to evolve and adapt to the changing needs of consumers and industries worldwide.

Single Channel, Dual Channel, Four Channel, Others in the Active Stylus Driver Chip - Global Market:

The Active Stylus Driver Chip market is segmented based on the number of channels it supports, which determines the chip's capability to handle multiple inputs simultaneously. Single-channel chips are the most basic type, designed to manage input from one stylus at a time. These chips are typically used in devices where only one user is expected to interact with the screen at any given moment, such as personal tablets or smartphones. They offer a cost-effective solution for manufacturers and are sufficient for most consumer applications. However, as the demand for more interactive and collaborative digital experiences grows, the limitations of single-channel chips become apparent. Dual-channel chips, on the other hand, can handle input from two styluses simultaneously. This capability is particularly useful in educational settings where two students might work on a digital whiteboard together or in professional environments where collaboration is key. Dual-channel chips provide a balance between cost and functionality, making them a popular choice for mid-range devices. Four-channel chips take this a step further, allowing for input from up to four styluses at once. This feature is ideal for large interactive displays used in conference rooms, design studios, or classrooms where multiple users need to interact with the screen simultaneously. The ability to support multiple inputs enhances the collaborative experience and allows for more dynamic and engaging interactions. Finally, there are chips categorized as "Others," which may support even more channels or offer specialized functionalities tailored to specific applications. These chips are often used in niche markets or high-end devices where advanced features are required. As the market for active stylus driver chips continues to grow, manufacturers are exploring new ways to enhance the capabilities of these chips, whether by increasing the number of channels they support or by integrating additional features that improve the user experience. This ongoing innovation is driven by the increasing demand for more interactive and immersive digital experiences across various industries. As a result, the market for active stylus driver chips is becoming more diverse, with a wide range of options available to meet the specific needs of different applications and user groups.

Cell Phone, Computer, Automobile Electronics, Others in the Active Stylus Driver Chip - Global Market:

Active Stylus Driver Chips are increasingly being used across various sectors, including cell phones, computers, automobile electronics, and other areas, due to their ability to enhance user interaction with digital devices. In cell phones, these chips enable precise touch input, allowing users to draw, write, and navigate their devices with greater accuracy. This functionality is particularly appealing to artists, designers, and professionals who require a high level of precision in their work. The integration of active stylus technology in smartphones also supports the growing trend of mobile productivity, enabling users to perform tasks such as note-taking and document editing on the go. In the realm of computers, active stylus driver chips are essential for devices like tablets and convertible laptops, where touch input is a primary mode of interaction. These chips facilitate a seamless transition between traditional keyboard and mouse input and stylus-based input, offering users a versatile and intuitive computing experience. The use of active stylus technology in computers is particularly beneficial in creative industries, where digital drawing and design applications are prevalent. In automobile electronics, active stylus driver chips are being used to enhance the functionality of in-car touchscreens and infotainment systems. By enabling precise touch input, these chips allow drivers and passengers to interact with the vehicle's digital interface more effectively, improving the overall user experience. This technology is also being explored for use in advanced driver-assistance systems (ADAS), where accurate input can enhance safety and navigation features. Beyond these specific applications, active stylus driver chips are finding use in a variety of other areas, including education, healthcare, and retail. In educational settings, these chips enable interactive learning experiences through digital whiteboards and tablets, allowing students and teachers to engage with content in new and innovative ways. In healthcare, active stylus technology is being used to improve the accuracy of digital medical records and facilitate telemedicine consultations. In retail, these chips are being integrated into point-of-sale systems and digital kiosks to enhance customer interaction and streamline transactions. As the demand for more interactive and intuitive digital experiences continues to grow, the use of active stylus driver chips is expected to expand across a wide range of industries and applications.

Active Stylus Driver Chip - Global Market Outlook:

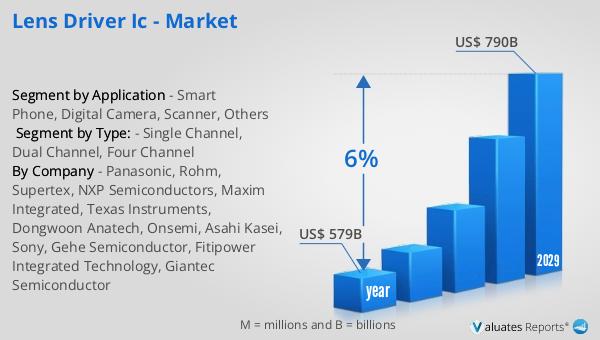

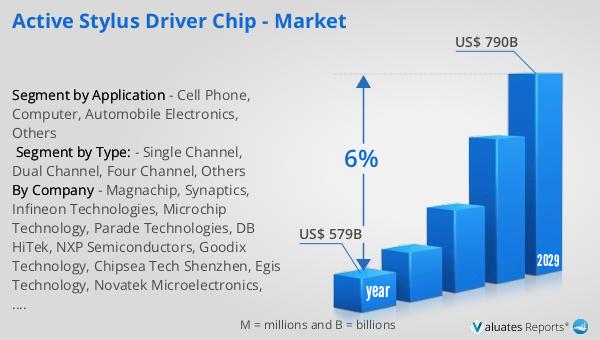

The semiconductor market, a critical component of the global technology landscape, was valued at approximately $579 billion in 2022. This market is projected to grow significantly, reaching an estimated $790 billion by 2029. This growth trajectory represents a compound annual growth rate (CAGR) of 6% over the forecast period. The expansion of the semiconductor market is driven by several factors, including the increasing demand for advanced electronic devices, the proliferation of the Internet of Things (IoT), and the ongoing development of new technologies such as artificial intelligence and 5G. As these technologies become more integrated into everyday life, the need for more powerful and efficient semiconductor solutions continues to rise. This growth is also supported by the increasing adoption of digital solutions across various industries, from automotive to healthcare, where semiconductors play a crucial role in enabling new functionalities and improving performance. Additionally, the semiconductor industry is benefiting from ongoing investments in research and development, which are driving innovation and leading to the creation of more advanced and efficient chips. As a result, the semiconductor market is poised for continued growth, with significant opportunities for companies that can capitalize on these trends and deliver cutting-edge solutions to meet the evolving needs of consumers and industries worldwide.

| Report Metric | Details |

| Report Name | Active Stylus Driver Chip - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Magnachip, Synaptics, Infineon Technologies, Microchip Technology, Parade Technologies, DB HiTek, NXP Semiconductors, Goodix Technology, Chipsea Tech Shenzhen, Egis Technology, Novatek Microelectronics, Raydium Semiconductor, FocalTech Systems, ELAN Microelectronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |