What is Amino Acid Metabolism Disorder Drug - Global Market?

Amino acid metabolism disorder drugs are a specialized segment within the global pharmaceutical market, focusing on treatments for rare genetic disorders that affect the body's ability to metabolize amino acids. These disorders can lead to severe health issues, including developmental delays, neurological problems, and even life-threatening conditions if not managed properly. The market for these drugs is driven by the need for effective treatments that can help manage symptoms and improve the quality of life for patients. With advancements in medical research and technology, new therapies are being developed to target specific metabolic pathways, offering hope for better management of these disorders. The global market for amino acid metabolism disorder drugs is characterized by a growing demand for innovative treatments, driven by increased awareness and diagnosis of these conditions. Pharmaceutical companies are investing in research and development to create more effective and targeted therapies, which is expected to drive market growth in the coming years. As the understanding of these disorders improves, the market is likely to see the introduction of new drugs that offer better efficacy and safety profiles, providing patients with more options for managing their conditions.

Arginine, Folic Acid, Vitamin B6 & B12, Thiamine, Vitamin D, Betaine, Carglumic Acid, Sapropterin Dihydrochloride, Others in the Amino Acid Metabolism Disorder Drug - Global Market:

Amino acid metabolism disorder drugs encompass a range of treatments designed to address specific metabolic deficiencies. Arginine, for instance, is used in the management of urea cycle disorders, where it helps to detoxify ammonia in the body. Folic acid, a B-vitamin, plays a crucial role in the treatment of homocystinuria, a disorder characterized by high levels of homocysteine in the blood. It helps in the conversion of homocysteine to methionine, thereby reducing its levels. Vitamin B6 and B12 are also essential in managing homocystinuria, as they aid in the metabolism of homocysteine. Thiamine, another B-vitamin, is used in the treatment of maple syrup urine disease, a disorder that affects the body's ability to break down certain amino acids. Vitamin D is often prescribed to patients with amino acid metabolism disorders to support bone health, as these conditions can lead to bone density issues. Betaine is used in the treatment of homocystinuria as well, where it helps to lower homocysteine levels by converting it to methionine. Carglumic acid is a drug used in the treatment of hyperammonemia, a condition characterized by high levels of ammonia in the blood, often seen in patients with N-acetylglutamate synthase deficiency. It works by activating the urea cycle, helping to reduce ammonia levels. Sapropterin dihydrochloride is used in the treatment of phenylketonuria (PKU), a disorder where the body cannot break down the amino acid phenylalanine. This drug helps to increase the activity of the enzyme responsible for breaking down phenylalanine, thereby reducing its levels in the blood. Other drugs in this market include enzyme replacement therapies and gene therapies, which are being developed to provide more targeted and effective treatments for these disorders. The global market for amino acid metabolism disorder drugs is driven by the need for these specialized treatments, as well as ongoing research and development efforts to improve existing therapies and discover new ones. As awareness and diagnosis of these disorders increase, the demand for effective treatments is expected to grow, driving market expansion.

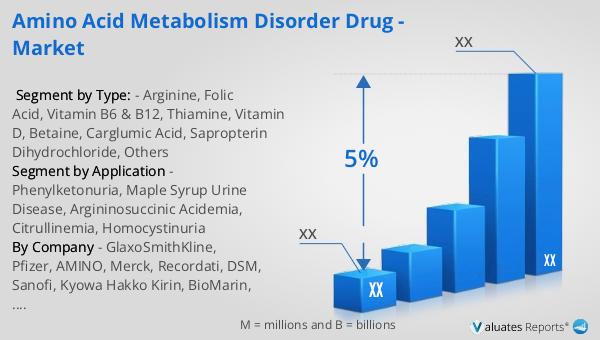

Phenylketonuria, Maple Syrup Urine Disease, Argininosuccinic Acidemia, Citrullinemia, Homocystinuria in the Amino Acid Metabolism Disorder Drug - Global Market:

Amino acid metabolism disorder drugs play a crucial role in managing various rare genetic disorders. In the case of phenylketonuria (PKU), these drugs help to manage the levels of phenylalanine in the blood, preventing the accumulation of this amino acid, which can lead to severe neurological damage if left untreated. Sapropterin dihydrochloride is one such drug used in PKU management, as it enhances the activity of the enzyme responsible for breaking down phenylalanine. For maple syrup urine disease, a disorder that affects the breakdown of branched-chain amino acids, thiamine is often used as part of the treatment regimen. This vitamin helps to support the metabolic pathways involved in amino acid breakdown, reducing the risk of toxic buildup. Argininosuccinic acidemia and citrullinemia are urea cycle disorders that lead to the accumulation of ammonia in the blood. Drugs like arginine and carglumic acid are used to help detoxify ammonia and support the urea cycle, preventing the harmful effects of hyperammonemia. In the case of homocystinuria, a disorder characterized by high levels of homocysteine, treatments often include a combination of folic acid, vitamin B6, vitamin B12, and betaine. These nutrients help to lower homocysteine levels by supporting its conversion to methionine, thereby reducing the risk of complications such as cardiovascular issues and developmental delays. The use of these drugs in managing amino acid metabolism disorders is critical, as they provide targeted therapies that address the specific metabolic deficiencies present in each condition. By doing so, they help to improve patient outcomes and quality of life, highlighting the importance of continued research and development in this field.

Amino Acid Metabolism Disorder Drug - Global Market Outlook:

The outlook for the amino acid metabolism disorder drug market is closely tied to the broader trends in the global pharmaceutical industry. In 2022, the global pharmaceutical market was valued at approximately 1,475 billion USD, with an expected compound annual growth rate (CAGR) of 5% over the next six years. This growth is indicative of the increasing demand for innovative and effective treatments across various therapeutic areas, including rare genetic disorders like amino acid metabolism disorders. In comparison, the chemical drug market, which forms a significant part of the pharmaceutical industry, was estimated to grow from 1,005 billion USD in 2018 to 1,094 billion USD in 2022. This growth reflects the ongoing advancements in drug development and the introduction of new therapies that address unmet medical needs. The amino acid metabolism disorder drug market is expected to benefit from these trends, as pharmaceutical companies continue to invest in research and development to create more targeted and effective treatments. As awareness and diagnosis of these disorders increase, the demand for specialized drugs is likely to grow, contributing to the overall expansion of the market. The focus on improving patient outcomes and quality of life through innovative therapies will remain a key driver of growth in this segment, underscoring the importance of continued investment in this area.

| Report Metric | Details |

| Report Name | Amino Acid Metabolism Disorder Drug - Market |

| CAGR | 5% |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | GlaxoSmithKline, Pfizer, AMINO, Merck, Recordati, DSM, Sanofi, Kyowa Hakko Kirin, BioMarin, Swedish Orphan Biovitrum, Shine Star (Hubei) Biological Engineering |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |