What is Global Metal Packaged Thyristors Market?

The Global Metal Packaged Thyristors Market is a specialized segment within the broader semiconductor industry, focusing on devices known as thyristors that are encased in metal packaging. These components are crucial in controlling and converting electrical power in various applications. Metal packaged thyristors are preferred for their durability and ability to handle high voltage and current levels, making them ideal for demanding environments. They are widely used in industries such as automotive, industrial control, and telecommunications, where reliable and efficient power management is essential. The market for these devices is driven by the increasing demand for energy-efficient solutions and the growing adoption of renewable energy sources, which require robust power control systems. As industries continue to modernize and seek more efficient ways to manage power, the demand for metal packaged thyristors is expected to grow, offering opportunities for innovation and development in this niche market. The market's growth is also supported by advancements in technology that enhance the performance and reliability of these devices, ensuring they meet the evolving needs of various sectors.

Bolt Type, Flat Type, Other in the Global Metal Packaged Thyristors Market:

In the Global Metal Packaged Thyristors Market, different types of thyristors are categorized based on their design and application, including Bolt Type, Flat Type, and Other configurations. Bolt Type thyristors are characterized by their robust construction, featuring a bolt-like design that allows for easy mounting and secure connections. These are typically used in applications where high mechanical strength and reliable thermal management are required, such as in heavy industrial machinery and high-power electrical systems. The bolt design ensures that the thyristor can withstand significant mechanical stress and maintain stable performance under varying environmental conditions. Flat Type thyristors, on the other hand, are designed with a flat, compact profile that makes them suitable for applications where space is limited. Their slim design allows for easy integration into compact electronic systems, making them ideal for use in consumer electronics, telecommunications, and computing devices. Despite their smaller size, Flat Type thyristors are engineered to deliver high performance and reliability, ensuring efficient power control in a variety of settings. The Other category encompasses a range of thyristor designs that do not fit neatly into the Bolt or Flat Type classifications. This includes custom-designed thyristors tailored for specific applications, as well as innovative designs that incorporate advanced materials and technologies to enhance performance. These thyristors are often used in specialized applications where unique power control solutions are required, such as in renewable energy systems and advanced industrial automation. The diversity in thyristor designs reflects the wide range of applications and environments in which these devices are used, highlighting the importance of selecting the right type of thyristor for each specific application. As the demand for efficient and reliable power control solutions continues to grow, manufacturers are investing in research and development to create new and improved thyristor designs that meet the evolving needs of the market. This includes exploring new materials and manufacturing techniques that can enhance the performance and durability of thyristors, as well as developing innovative packaging solutions that improve thermal management and reduce the overall size and weight of the devices. By offering a variety of thyristor types, the Global Metal Packaged Thyristors Market is able to cater to the diverse needs of industries ranging from automotive and transportation to industrial control and telecommunications, ensuring that each application has access to the most suitable power control solutions.

Automotive & Transportation, Industrial Control, Computing & Communications, Others in the Global Metal Packaged Thyristors Market:

The Global Metal Packaged Thyristors Market plays a crucial role in various sectors, including Automotive & Transportation, Industrial Control, Computing & Communications, and others. In the automotive and transportation industry, metal packaged thyristors are used in electric vehicles (EVs) and hybrid vehicles to manage power conversion and control. They help in efficiently converting and distributing electrical energy from the battery to the motor, ensuring optimal performance and energy efficiency. Additionally, these thyristors are used in railway systems for controlling power in traction systems, enhancing the reliability and efficiency of train operations. In the industrial control sector, metal packaged thyristors are integral to managing power in machinery and equipment. They are used in motor drives, welding equipment, and power supplies, where precise control of electrical power is essential for maintaining operational efficiency and safety. These thyristors enable smooth and efficient power regulation, reducing energy consumption and minimizing downtime in industrial processes. In the computing and communications sector, metal packaged thyristors are used in power supplies and voltage regulation systems for servers, data centers, and telecommunications equipment. They ensure stable and reliable power delivery, which is critical for maintaining the performance and uptime of these systems. By providing efficient power management, thyristors help in reducing energy costs and improving the overall sustainability of computing and communication infrastructures. Beyond these sectors, metal packaged thyristors find applications in renewable energy systems, such as wind and solar power installations, where they are used to control and convert power generated from renewable sources. They play a vital role in ensuring the efficient integration of renewable energy into the grid, supporting the transition to cleaner and more sustainable energy solutions. The versatility and reliability of metal packaged thyristors make them indispensable in a wide range of applications, driving their demand across various industries. As the need for efficient power management solutions continues to grow, the Global Metal Packaged Thyristors Market is poised to expand, offering innovative solutions to meet the evolving needs of different sectors.

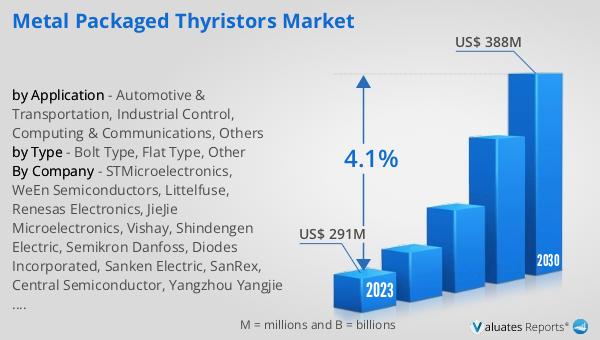

Global Metal Packaged Thyristors Market Outlook:

The outlook for the Global Metal Packaged Thyristors Market indicates a positive growth trajectory over the coming years. In 2023, the market was valued at approximately US$ 291 million, reflecting its significance in the semiconductor industry. Looking ahead, the market is projected to reach around US$ 388 million by 2030, demonstrating a steady compound annual growth rate (CAGR) of 4.1% from 2024 to 2030. This growth is driven by the increasing demand for efficient power management solutions across various industries, including automotive, industrial control, and telecommunications. As industries continue to modernize and adopt more energy-efficient technologies, the need for reliable and high-performance thyristors is expected to rise. The market's expansion is also supported by advancements in technology that enhance the performance and reliability of metal packaged thyristors, ensuring they meet the evolving needs of different sectors. Additionally, the growing focus on renewable energy and sustainable solutions is likely to contribute to the market's growth, as thyristors play a crucial role in managing power in renewable energy systems. Overall, the Global Metal Packaged Thyristors Market is poised for steady growth, driven by the increasing demand for efficient and reliable power control solutions across various industries.

| Report Metric | Details |

| Report Name | Metal Packaged Thyristors Market |

| Accounted market size in 2023 | US$ 291 million |

| Forecasted market size in 2030 | US$ 388 million |

| CAGR | 4.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | STMicroelectronics, WeEn Semiconductors, Littelfuse, Renesas Electronics, JieJie Microelectronics, Vishay, Shindengen Electric, Semikron Danfoss, Diodes Incorporated, Sanken Electric, SanRex, Central Semiconductor, Yangzhou Yangjie Electronic Technology, Macmic Science and Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |