What is Global Medical Sampling Swabs Market?

The Global Medical Sampling Swabs Market is a crucial segment within the broader medical devices industry, focusing on the production and distribution of swabs used for collecting samples from the human body. These swabs are essential tools in medical diagnostics, enabling healthcare professionals to collect samples from various parts of the body for testing and analysis. The market encompasses a wide range of swabs, including those used for nasal, throat, anal, and gynecological sampling, among others. The demand for medical sampling swabs has been significantly influenced by the increasing need for accurate and efficient diagnostic tools, especially in the wake of global health challenges such as the COVID-19 pandemic. The market is characterized by continuous innovation, with manufacturers striving to develop swabs that offer better sample collection efficiency, comfort for patients, and compatibility with advanced diagnostic technologies. As healthcare systems worldwide continue to emphasize the importance of early and accurate diagnosis, the Global Medical Sampling Swabs Market is expected to play a pivotal role in supporting these efforts, ensuring that healthcare providers have access to the necessary tools to deliver high-quality care.

Nasal Swabs, Throat Swabs, Anal Swabs, Gynecological Sampling Swab, Others in the Global Medical Sampling Swabs Market:

Nasal swabs are a critical component of the Global Medical Sampling Swabs Market, primarily used for collecting samples from the nasal cavity. These swabs are designed to be inserted into the nostril to collect secretions from the upper respiratory tract, which are then analyzed for the presence of pathogens such as viruses and bacteria. Nasal swabs have gained significant attention due to their role in COVID-19 testing, where they are used to detect the presence of the SARS-CoV-2 virus. The design of nasal swabs is crucial, as they need to be flexible enough to navigate the nasal passages while being sturdy enough to collect an adequate sample. Throat swabs, on the other hand, are used to collect samples from the back of the throat. These swabs are commonly used to diagnose infections such as strep throat and other respiratory illnesses. The swab is gently rubbed against the tonsils and the back of the throat to collect mucus and cells, which are then tested for pathogens. Anal swabs are less commonly discussed but are used in specific diagnostic procedures, particularly for detecting gastrointestinal infections and certain sexually transmitted infections. These swabs are inserted into the rectum to collect samples from the lower gastrointestinal tract. Gynecological sampling swabs are used in the collection of cervical and vaginal samples, primarily for Pap smears and HPV testing. These swabs are designed to be gentle yet effective in collecting cells from the cervix and vaginal walls. Other types of swabs in the market include those used for wound sampling, ear and eye swabs, and environmental sampling swabs used in healthcare settings to monitor cleanliness and sterility. Each type of swab is designed with specific features to optimize sample collection for its intended use, ensuring that healthcare providers can obtain accurate and reliable diagnostic results. The diversity of swabs available in the Global Medical Sampling Swabs Market reflects the wide range of diagnostic needs in modern healthcare, highlighting the importance of these tools in disease detection and management.

Scientific Research, Medical Test, Others in the Global Medical Sampling Swabs Market:

The usage of swabs in the Global Medical Sampling Swabs Market extends beyond traditional medical testing, playing a vital role in scientific research and other applications. In scientific research, swabs are used to collect samples for various studies, including microbiological research, environmental monitoring, and genetic studies. Researchers rely on swabs to obtain samples from different environments, such as soil, water, and surfaces, to study microbial communities and their interactions with the environment. Swabs are also used in forensic science to collect DNA samples from crime scenes, helping to identify suspects and solve criminal cases. In medical testing, swabs are indispensable tools for diagnosing a wide range of conditions. They are used to collect samples for testing respiratory infections, sexually transmitted infections, and other infectious diseases. Swabs are also used in routine screenings, such as Pap smears, to detect precancerous changes in cervical cells. The accuracy and reliability of swab-based testing have made them a cornerstone of modern diagnostics, enabling healthcare providers to make informed decisions about patient care. Beyond scientific research and medical testing, swabs are used in various other applications, including food safety testing, where they are used to collect samples from food products and surfaces to detect contamination. Swabs are also used in veterinary medicine to collect samples from animals for diagnostic testing. The versatility and effectiveness of swabs in collecting samples make them an essential tool in many fields, supporting efforts to improve health and safety across different sectors. The Global Medical Sampling Swabs Market continues to evolve, driven by advancements in technology and the growing demand for accurate and efficient diagnostic tools. As new applications for swabs emerge, the market is expected to expand, offering new opportunities for innovation and growth.

Global Medical Sampling Swabs Market Outlook:

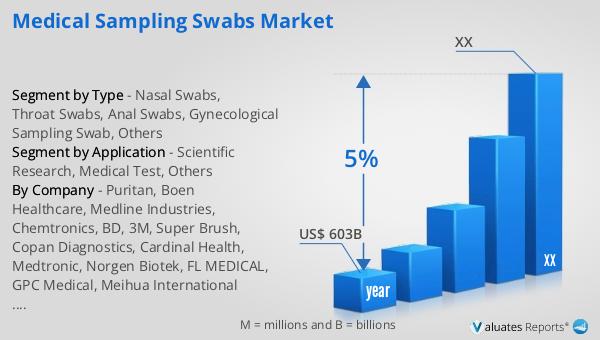

Our research indicates that the global market for medical devices, which includes the Global Medical Sampling Swabs Market, is projected to reach an estimated value of $603 billion in 2023. This market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing demand for advanced diagnostic tools, the rising prevalence of chronic diseases, and the growing emphasis on early and accurate diagnosis. The medical devices market encompasses a wide range of products, including diagnostic equipment, surgical instruments, and medical sampling swabs, among others. The continuous innovation in medical technology and the increasing adoption of digital health solutions are also contributing to the growth of the market. As healthcare systems worldwide strive to improve patient outcomes and reduce healthcare costs, the demand for efficient and reliable medical devices is expected to rise. The Global Medical Sampling Swabs Market, as a part of this broader market, is poised to benefit from these trends, with manufacturers focusing on developing swabs that offer better performance and patient comfort. The market's growth is also supported by the increasing awareness of the importance of regular health screenings and the need for effective diagnostic tools in managing public health challenges. As the market continues to evolve, it presents significant opportunities for companies to innovate and expand their product offerings, ensuring that healthcare providers have access to the best tools for delivering high-quality care.

| Report Metric | Details |

| Report Name | Medical Sampling Swabs Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Puritan, Boen Healthcare, Medline Industries, Chemtronics, BD, 3M, Super Brush, Copan Diagnostics, Cardinal Health, Medtronic, Norgen Biotek, FL MEDICAL, GPC Medical, Meihua International Medical Technologies, Jiangsu PROVINCE Jianerkang Madical Dressing, Fujian Haiyao, Jiangsu HanHeng Medical Technology, Zhejiang Jiaxin Medical, Fukehai Technology (Suzhou), Miraclean Technology, Taizhou Mairuijie Medical Packaging |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |