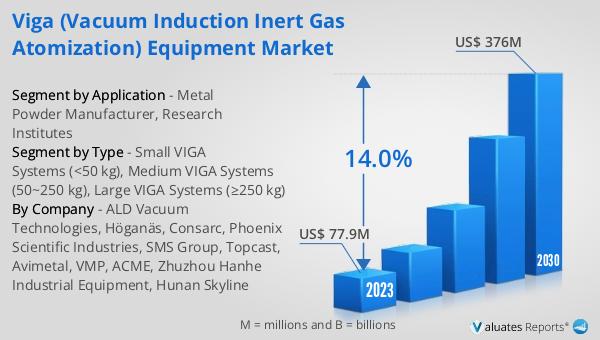

What is Global Helicobacter Pylori Breath Testers Market?

The Global Helicobacter Pylori Breath Testers Market is a specialized segment within the medical diagnostics industry, focusing on non-invasive testing methods for detecting Helicobacter pylori infections. Helicobacter pylori is a type of bacteria that infects the stomach lining and is associated with various gastrointestinal diseases, including peptic ulcers and gastric cancer. The breath test is a preferred diagnostic tool because it is simple, safe, and effective, providing results without the need for invasive procedures like endoscopy. The market for these breath testers is driven by the increasing prevalence of H. pylori infections worldwide, growing awareness about the importance of early diagnosis, and advancements in medical technology that enhance the accuracy and reliability of these tests. The breath test works by measuring isotopes in the breath after the patient ingests a urea solution, which the bacteria metabolize, releasing carbon dioxide that can be detected in the breath. This market is poised for growth as healthcare providers and patients alike seek more efficient and less invasive diagnostic options. The demand for these testers is also fueled by the rising healthcare expenditure and the expansion of healthcare infrastructure in emerging economies.

13C-UBT System, 14C-UBT System in the Global Helicobacter Pylori Breath Testers Market:

The 13C-UBT System and 14C-UBT System are two primary technologies used in the Global Helicobacter Pylori Breath Testers Market, each with distinct characteristics and applications. The 13C-UBT System utilizes a non-radioactive isotope of carbon, making it a safer option for a broader range of patients, including children and pregnant women. This system involves the patient ingesting a urea solution labeled with 13C, which, if H. pylori is present, is metabolized by the bacteria, releasing 13C-labeled carbon dioxide that can be measured in the patient's breath. The non-radioactive nature of the 13C-UBT System makes it highly favorable in clinical settings, where patient safety is a top priority. On the other hand, the 14C-UBT System uses a radioactive isotope of carbon, 14C, which is also ingested in a urea solution. The presence of H. pylori leads to the release of 14C-labeled carbon dioxide, which is then detected in the breath. While the 14C-UBT System is highly accurate and cost-effective, its use is often limited to adult patients due to the radioactive nature of the isotope, albeit at very low and safe levels. Both systems are integral to the market, offering healthcare providers options based on patient needs and institutional capabilities. The choice between the two often depends on factors such as patient demographics, healthcare regulations, and the availability of testing equipment. The 13C-UBT System is generally preferred in regions with stringent regulations regarding radioactive materials, while the 14C-UBT System might be more prevalent in areas where cost constraints are a significant consideration. The technological advancements in both systems have led to improved sensitivity and specificity, making them reliable tools for diagnosing H. pylori infections. As the market evolves, there is a continuous push towards enhancing the efficiency of these systems, reducing the time required for testing, and minimizing any potential discomfort for patients. The integration of digital technologies and data analytics is also becoming more common, allowing for better tracking of test results and patient outcomes. This integration is particularly beneficial in large healthcare facilities where managing patient data efficiently is crucial. Overall, the 13C-UBT and 14C-UBT Systems represent the forefront of non-invasive diagnostic testing for H. pylori, each contributing uniquely to the market's growth and development.

Hospital, Physical Examination Center, Others in the Global Helicobacter Pylori Breath Testers Market:

The usage of Global Helicobacter Pylori Breath Testers Market spans various healthcare settings, including hospitals, physical examination centers, and other medical facilities, each playing a crucial role in the diagnosis and management of H. pylori infections. In hospitals, these breath testers are often part of the routine diagnostic procedures for patients presenting with symptoms of gastrointestinal distress, such as abdominal pain, bloating, or indigestion. Hospitals benefit from the non-invasive nature of the breath test, which allows for quick and accurate diagnosis without the need for more invasive procedures like endoscopy. This is particularly advantageous in emergency settings or for patients who are not suitable candidates for invasive diagnostics. In physical examination centers, the breath test is commonly used as part of routine health check-ups, especially in regions with a high prevalence of H. pylori infections. These centers focus on preventive healthcare, and the breath test serves as an effective tool for early detection, allowing for timely intervention and treatment. The ease of administration and rapid results make it an ideal choice for busy examination centers that handle a large volume of patients. Other medical facilities, such as private clinics and specialized gastroenterology centers, also utilize these breath testers to provide targeted diagnostic services. In these settings, the breath test is often used in conjunction with other diagnostic tools to provide a comprehensive assessment of the patient's gastrointestinal health. The versatility of the breath test, combined with its high accuracy, makes it a valuable asset in the diagnostic toolkit of healthcare providers. Additionally, the breath test is increasingly being used in research settings to study the epidemiology of H. pylori infections and to evaluate the effectiveness of various treatment regimens. This research is crucial for developing new strategies to combat H. pylori and reduce its associated health risks. Overall, the widespread use of Helicobacter Pylori Breath Testers across different healthcare settings underscores their importance in modern medical diagnostics, providing a reliable, non-invasive, and efficient method for detecting H. pylori infections.

Global Helicobacter Pylori Breath Testers Market Outlook:

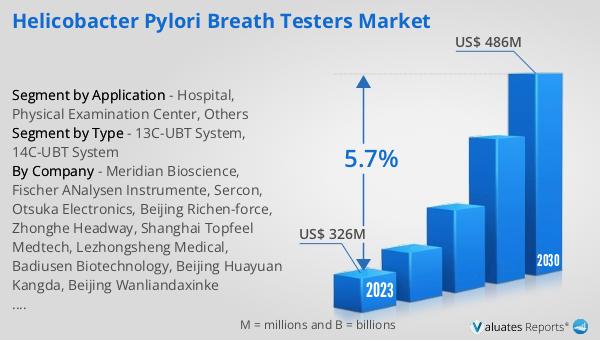

The outlook for the Global Helicobacter Pylori Breath Testers Market is promising, with significant growth anticipated over the coming years. In 2023, the market was valued at approximately US$ 326 million, reflecting the increasing demand for non-invasive diagnostic solutions for H. pylori infections. By 2030, the market is expected to reach around US$ 486 million, driven by a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2024 to 2030. This growth trajectory highlights the expanding recognition of the importance of early and accurate diagnosis of H. pylori infections, which are linked to serious gastrointestinal conditions. The market's expansion is supported by advancements in breath testing technologies, which enhance the accuracy and reliability of test results, making them more appealing to healthcare providers and patients alike. Additionally, the increasing prevalence of H. pylori infections globally, coupled with rising healthcare expenditures and improved healthcare infrastructure, particularly in emerging economies, is expected to fuel market growth. As healthcare systems continue to prioritize patient safety and comfort, the demand for non-invasive diagnostic tools like breath testers is likely to increase. The market's growth is also influenced by the ongoing efforts to integrate digital technologies and data analytics into diagnostic processes, improving the efficiency and effectiveness of H. pylori testing. Overall, the Global Helicobacter Pylori Breath Testers Market is poised for significant growth, driven by technological advancements, increasing awareness, and the rising need for efficient diagnostic solutions.

| Report Metric | Details |

| Report Name | Helicobacter Pylori Breath Testers Market |

| Accounted market size in 2023 | US$ 326 million |

| Forecasted market size in 2030 | US$ 486 million |

| CAGR | 5.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Meridian Bioscience, Fischer ANalysen Instrumente, Sercon, Otsuka Electronics, Beijing Richen-force, Zhonghe Headway, Shanghai Topfeel Medtech, Lezhongsheng Medical, Badiusen Biotechnology, Beijing Huayuan Kangda, Beijing Wanliandaxinke Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |