What is Global Rock Mechanics Testing System Market?

The Global Rock Mechanics Testing System Market is a specialized segment within the broader field of geotechnical engineering and material testing. This market focuses on the development, production, and distribution of testing systems designed to evaluate the mechanical properties of rocks. These systems are crucial for understanding the behavior of rock materials under various conditions, which is essential for applications in construction, mining, oil and gas exploration, and civil engineering projects. The testing systems typically include equipment for measuring parameters such as compressive strength, tensile strength, shear strength, and elasticity of rock samples. The insights gained from these tests help engineers and geologists make informed decisions about the suitability of rock materials for specific projects, ensuring safety and efficiency. As infrastructure development and resource extraction activities continue to grow globally, the demand for advanced rock mechanics testing systems is expected to rise, driving innovation and technological advancements in this market. The market is characterized by a mix of established players and emerging companies, all striving to offer more accurate, reliable, and user-friendly testing solutions to meet the evolving needs of their clients.

Semi-automatic, Fully Automatic in the Global Rock Mechanics Testing System Market:

The Global Rock Mechanics Testing System Market is segmented into two main categories based on the level of automation: semi-automatic and fully automatic systems. Semi-automatic rock mechanics testing systems require some level of manual intervention during the testing process. These systems are typically more affordable and offer flexibility for users who prefer to have control over certain aspects of the testing procedure. They are equipped with basic automation features that assist in data collection and analysis, but the user is responsible for setting up the test parameters and initiating the tests. Semi-automatic systems are often favored by smaller laboratories or institutions with budget constraints, as they provide a cost-effective solution without compromising on the accuracy of the results. On the other hand, fully automatic rock mechanics testing systems are designed to perform tests with minimal human intervention. These systems are equipped with advanced software and hardware that allow for the complete automation of the testing process, from sample preparation to data analysis. Fully automatic systems are ideal for high-throughput laboratories and large-scale projects where efficiency and consistency are paramount. They offer precise control over test conditions and parameters, ensuring repeatability and reliability of results. The integration of sophisticated sensors and data acquisition systems in fully automatic systems enables real-time monitoring and analysis, providing users with immediate insights into the mechanical properties of rock samples. This level of automation not only enhances productivity but also reduces the potential for human error, making fully automatic systems a preferred choice for industries that require high precision and accuracy. The choice between semi-automatic and fully automatic systems depends on several factors, including budget, testing requirements, and the scale of operations. While semi-automatic systems offer a balance between cost and functionality, fully automatic systems provide unparalleled efficiency and accuracy, albeit at a higher cost. As technology continues to advance, the gap between these two categories is expected to narrow, with semi-automatic systems incorporating more automated features and fully automatic systems becoming more affordable. This evolution will likely lead to increased adoption of rock mechanics testing systems across various industries, as organizations seek to optimize their testing processes and improve the quality of their results.

Laboratory, University, Construction Company, Others in the Global Rock Mechanics Testing System Market:

The Global Rock Mechanics Testing System Market finds its applications across various sectors, including laboratories, universities, construction companies, and other industries. In laboratories, these testing systems are essential for conducting detailed analyses of rock samples. Laboratories, whether independent or part of larger organizations, utilize these systems to perform a wide range of tests that determine the mechanical properties of rocks. The data obtained from these tests are crucial for research and development activities, quality control, and compliance with industry standards. Laboratories often require high-precision equipment to ensure the accuracy and reliability of their results, making rock mechanics testing systems an indispensable tool in their operations. Universities also play a significant role in the Global Rock Mechanics Testing System Market. Academic institutions use these systems for educational and research purposes, providing students and researchers with hands-on experience in testing and analyzing rock materials. The insights gained from these studies contribute to the advancement of knowledge in geotechnical engineering and related fields. Universities often collaborate with industry partners to conduct research projects that address real-world challenges, further driving the demand for advanced testing systems. In the construction industry, rock mechanics testing systems are used to assess the suitability of rock materials for various construction projects. Construction companies rely on these systems to evaluate the strength and stability of rock foundations, ensuring the safety and durability of structures such as buildings, bridges, and tunnels. The data obtained from these tests help engineers make informed decisions about the design and construction of infrastructure projects, minimizing the risk of structural failures. Other industries, such as mining and oil and gas exploration, also benefit from the use of rock mechanics testing systems. In mining, these systems are used to evaluate the stability of rock formations and assess the potential for rock bursts or collapses, ensuring the safety of mining operations. In the oil and gas industry, rock mechanics testing systems help in the evaluation of reservoir rocks, aiding in the optimization of extraction processes and the assessment of potential drilling sites. Overall, the Global Rock Mechanics Testing System Market serves a diverse range of industries, each with unique requirements and applications. The versatility and reliability of these systems make them a valuable asset for organizations seeking to enhance their understanding of rock materials and improve the quality and safety of their projects.

Global Rock Mechanics Testing System Market Outlook:

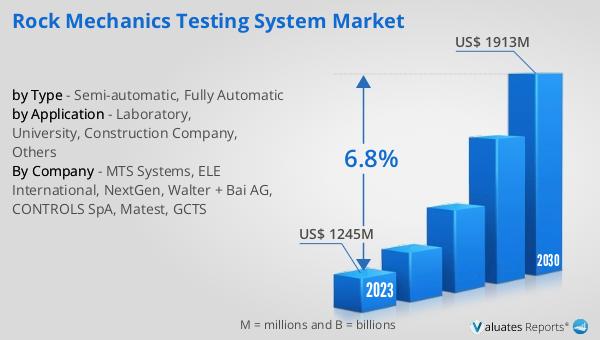

The outlook for the Global Rock Mechanics Testing System Market indicates a promising growth trajectory. In 2023, the market was valued at approximately USD 1,245 million, reflecting its significant role in various industries that require precise testing of rock materials. By 2030, the market is projected to reach around USD 1,913 million, driven by a compound annual growth rate (CAGR) of 6.8% during the forecast period from 2024 to 2030. This growth can be attributed to the increasing demand for advanced testing systems across sectors such as construction, mining, and oil and gas exploration. As infrastructure development and resource extraction activities continue to expand globally, the need for accurate and reliable rock mechanics testing systems becomes more critical. The market's expansion is also supported by technological advancements that enhance the efficiency and accuracy of testing systems, making them more accessible to a wider range of users. Additionally, the growing emphasis on safety and quality in construction and resource extraction projects further fuels the demand for these systems. As a result, the Global Rock Mechanics Testing System Market is poised for substantial growth, offering opportunities for both established players and new entrants to innovate and capture market share.

| Report Metric | Details |

| Report Name | Rock Mechanics Testing System Market |

| Accounted market size in 2023 | US$ 1245 million |

| Forecasted market size in 2030 | US$ 1913 million |

| CAGR | 6.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | MTS Systems, ELE International, NextGen, Walter + Bai AG, CONTROLS SpA, Matest, GCTS |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |