What is Global Cable and Cable Assemblies for Semiconductor Equipment Market?

The Global Cable and Cable Assemblies for Semiconductor Equipment Market is a specialized segment within the broader electronics and semiconductor industry. This market focuses on the production and distribution of cables and cable assemblies specifically designed for semiconductor manufacturing equipment. These cables and assemblies are crucial for ensuring the seamless operation of semiconductor fabrication processes, which involve highly sophisticated and sensitive machinery. The market encompasses a wide range of products, including sensor and signal connectivity cables, power connectivity cables, motor connectivity cables, Ethernet connectivity cables, and RF connectivity cables, among others. These components are essential for transmitting data, power, and signals between various parts of semiconductor equipment, thereby enabling precise control and monitoring of manufacturing processes. The demand for these specialized cables and assemblies is driven by the continuous advancements in semiconductor technology, which require increasingly complex and reliable connectivity solutions. As the semiconductor industry continues to grow and evolve, the Global Cable and Cable Assemblies for Semiconductor Equipment Market is expected to play a critical role in supporting the development and production of next-generation semiconductor devices.

Sensor & Signal Connectivity, Power Connectivity, Motor Connectivity, Ethernet Connectivity, RF Connectivity, Others in the Global Cable and Cable Assemblies for Semiconductor Equipment Market:

Sensor and signal connectivity cables are vital components in the Global Cable and Cable Assemblies for Semiconductor Equipment Market. These cables are designed to transmit data from various sensors to the control systems of semiconductor manufacturing equipment. They ensure accurate monitoring and control of parameters such as temperature, pressure, and chemical composition, which are crucial for maintaining the quality and efficiency of semiconductor fabrication processes. Power connectivity cables, on the other hand, are responsible for delivering electrical power to different parts of the semiconductor equipment. These cables must be highly reliable and capable of handling high voltages and currents to ensure the uninterrupted operation of the machinery. Motor connectivity cables are used to connect motors and drives within the semiconductor equipment. These cables must be flexible and durable to withstand the constant movement and vibrations associated with motor operations. Ethernet connectivity cables are essential for enabling high-speed data communication between different components of the semiconductor equipment. They support the integration of advanced control systems and facilitate real-time data exchange, which is critical for optimizing the manufacturing processes. RF connectivity cables are used for transmitting radio frequency signals within the semiconductor equipment. These cables must have excellent shielding properties to prevent signal interference and ensure accurate data transmission. Other types of cables and assemblies in this market include those designed for specific applications such as high-temperature environments, cleanroom conditions, and corrosive atmospheres. Each type of cable and assembly plays a unique role in ensuring the smooth and efficient operation of semiconductor manufacturing equipment. The continuous advancements in semiconductor technology drive the demand for more sophisticated and reliable connectivity solutions, making the Global Cable and Cable Assemblies for Semiconductor Equipment Market a dynamic and rapidly evolving industry.

Front-End Processes, Back-End Processes, Fab Support Equipment in the Global Cable and Cable Assemblies for Semiconductor Equipment Market:

The usage of Global Cable and Cable Assemblies for Semiconductor Equipment Market is integral to various stages of semiconductor manufacturing, including front-end processes, back-end processes, and fab support equipment. In front-end processes, which involve the initial stages of semiconductor fabrication such as wafer processing, lithography, and etching, cables and cable assemblies are used to connect and control various equipment. These cables ensure precise data transmission and power delivery, enabling accurate control of the fabrication processes. For instance, sensor and signal connectivity cables are used to monitor critical parameters such as temperature and pressure during wafer processing, while power connectivity cables ensure the reliable operation of lithography and etching equipment. In back-end processes, which include assembly, packaging, and testing of semiconductor devices, cables and cable assemblies are used to connect testing equipment, packaging machinery, and other tools. Ethernet connectivity cables, for example, facilitate high-speed data communication between testing equipment and control systems, ensuring accurate and efficient testing of semiconductor devices. Motor connectivity cables are used to drive packaging machinery, ensuring precise and reliable assembly of semiconductor devices. Fab support equipment, which includes various auxiliary systems such as chemical delivery systems, vacuum pumps, and cleanroom facilities, also relies on specialized cables and cable assemblies. These cables ensure the reliable operation of support equipment, which is essential for maintaining the quality and efficiency of semiconductor manufacturing processes. For example, RF connectivity cables are used in vacuum pumps to transmit radio frequency signals, while other specialized cables are used in chemical delivery systems to ensure safe and accurate delivery of chemicals. Overall, the usage of cables and cable assemblies in semiconductor manufacturing is critical for ensuring the seamless operation of various equipment and processes, thereby supporting the production of high-quality semiconductor devices.

Global Cable and Cable Assemblies for Semiconductor Equipment Market Outlook:

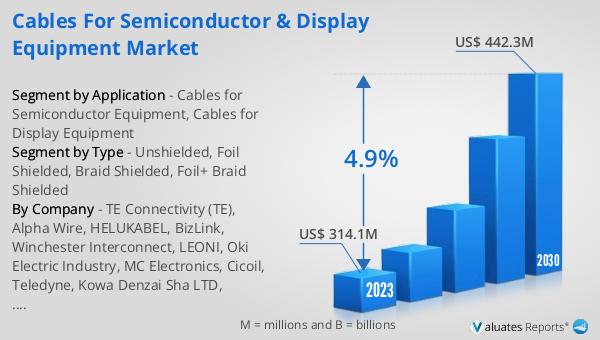

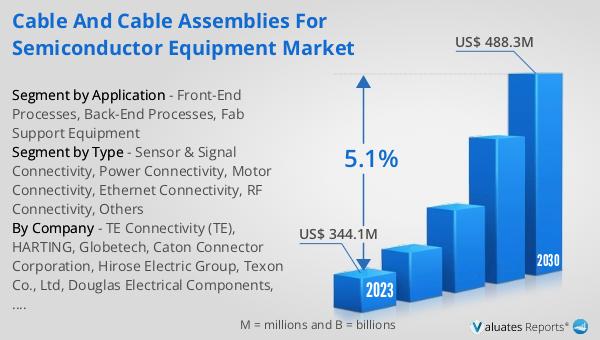

The global Cable and Cable Assemblies for Semiconductor Equipment market was valued at US$ 344.1 million in 2023 and is anticipated to reach US$ 488.3 million by 2030, witnessing a CAGR of 5.1% during the forecast period 2024-2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased 5% from $102.6 billion in 2021 to an all-time record of $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022 despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings. This growth in the semiconductor equipment market is indicative of the increasing demand for advanced semiconductor devices, which in turn drives the demand for specialized cables and cable assemblies. The continuous advancements in semiconductor technology and the increasing complexity of semiconductor manufacturing processes necessitate the use of highly reliable and sophisticated connectivity solutions. As a result, the Global Cable and Cable Assemblies for Semiconductor Equipment Market is expected to experience significant growth in the coming years, driven by the ongoing developments in the semiconductor industry and the increasing demand for high-performance semiconductor devices.

| Report Metric | Details |

| Report Name | Cable and Cable Assemblies for Semiconductor Equipment Market |

| Accounted market size in 2023 | US$ 344.1 million |

| Forecasted market size in 2030 | US$ 488.3 million |

| CAGR | 5.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | TE Connectivity (TE), HARTING, Globetech, Caton Connector Corporation, Hirose Electric Group, Texon Co., Ltd, Douglas Electrical Components, GigaLane, JAE Electronics, Inc., CeramTec, OMRON SWITCH & DEVICES Corporation, Rosenberger Group, Winchester Interconnect, LEONI, Telit, Alpha Wire, HELUKABEL, BizLink, Oki Electric Industry, MC Electronics, Cicoil, Teledyne, Kowa Denzai Sha LTD, CHUGOKU ELECTRIC WIRE & CABLE CO.,LTD., Prysmian, Nexans, LS Cable & System, TF Kable, W. L. Gore & Associates, TOTOKU INC., SAB, Daiichi Denzai (DID), NICHIGOH COMMUNICATION ELECTRIC WIRE CO.,LTD. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |