What is Global Cleaning for Semiconductor and Display Equipment Parts Market?

The global Cleaning for Semiconductor and Display Equipment Parts market is a specialized sector focused on maintaining the cleanliness and functionality of equipment used in the semiconductor and display industries. This market encompasses a variety of cleaning methods and technologies designed to remove contaminants from equipment parts, ensuring optimal performance and longevity. The importance of this market cannot be overstated, as even the smallest particles can cause significant defects in semiconductor wafers and display panels, leading to reduced yield and increased production costs. The market includes services and products for both wet and dry cleaning methods, each tailored to specific types of contaminants and equipment. As the demand for advanced electronics and high-resolution displays continues to grow, the need for effective cleaning solutions becomes increasingly critical. Companies in this market are continually innovating to develop more efficient and environmentally friendly cleaning processes. The market is also influenced by stringent industry standards and regulations, which drive the adoption of advanced cleaning technologies. Overall, the global Cleaning for Semiconductor and Display Equipment Parts market plays a crucial role in the electronics manufacturing ecosystem, ensuring the production of high-quality, reliable products.

Wet Cleaning, Dry Cleaning (Physical) in the Global Cleaning for Semiconductor and Display Equipment Parts Market:

Wet cleaning and dry cleaning (physical) are two primary methods used in the global Cleaning for Semiconductor and Display Equipment Parts market. Wet cleaning involves the use of liquid chemicals to dissolve and remove contaminants from equipment parts. This method is highly effective for removing organic residues, particles, and other types of contaminants that can adhere to surfaces during the manufacturing process. Wet cleaning typically includes processes such as chemical baths, ultrasonic cleaning, and rinsing with deionized water. The choice of chemicals and cleaning parameters is critical to ensure thorough cleaning without damaging the delicate parts. On the other hand, dry cleaning (physical) methods do not involve the use of liquids. Instead, they rely on physical forces such as plasma, laser, or mechanical abrasion to remove contaminants. Plasma cleaning, for example, uses ionized gas to break down and remove organic contaminants from surfaces. Laser cleaning employs focused laser beams to vaporize contaminants without affecting the underlying material. Mechanical abrasion, although less common, involves the use of brushes or other abrasive tools to physically scrub away contaminants. Each method has its advantages and limitations. Wet cleaning is generally more effective for a broader range of contaminants but can be more complex and require careful handling of chemicals. Dry cleaning methods are often faster and can be more environmentally friendly, as they do not produce liquid waste. However, they may not be as effective for certain types of contaminants. The choice between wet and dry cleaning depends on various factors, including the type of equipment, the nature of the contaminants, and the specific requirements of the manufacturing process. Both methods are essential in maintaining the cleanliness and performance of semiconductor and display equipment parts, ensuring high-quality production and reducing the risk of defects.

Cleaning for Semiconductor Equipment Parts, Cleaning for Flat Panel Display Equipment Parts in the Global Cleaning for Semiconductor and Display Equipment Parts Market:

The usage of global cleaning for semiconductor and display equipment parts is crucial in several key areas, including cleaning for semiconductor equipment parts and cleaning for flat panel display equipment parts. In the semiconductor industry, maintaining the cleanliness of equipment parts is vital for producing defect-free wafers. Contaminants such as particles, organic residues, and metallic impurities can cause defects in the semiconductor wafers, leading to reduced yield and increased production costs. Cleaning processes are integrated into various stages of semiconductor manufacturing, from wafer fabrication to packaging. For instance, during wafer fabrication, equipment parts such as photomasks, etching chambers, and deposition tools must be meticulously cleaned to prevent contamination. Similarly, in the packaging stage, lead frames, bonding tools, and other components require thorough cleaning to ensure reliable performance. In the flat panel display industry, cleaning is equally important. Display panels, such as those used in televisions, smartphones, and monitors, require pristine surfaces to achieve high resolution and clarity. Contaminants on equipment parts can lead to defects such as dead pixels, color inconsistencies, and reduced display quality. Cleaning processes for flat panel display equipment parts include the removal of particles, organic residues, and other contaminants from substrates, masks, and deposition tools. Both wet and dry cleaning methods are employed, depending on the type of contaminants and the specific requirements of the manufacturing process. The effectiveness of these cleaning processes directly impacts the quality and performance of the final display products. Overall, the usage of global cleaning for semiconductor and display equipment parts is essential for ensuring the production of high-quality, reliable electronic devices. By maintaining the cleanliness of equipment parts, manufacturers can reduce defects, improve yield, and enhance the performance of their products.

Global Cleaning for Semiconductor and Display Equipment Parts Market Outlook:

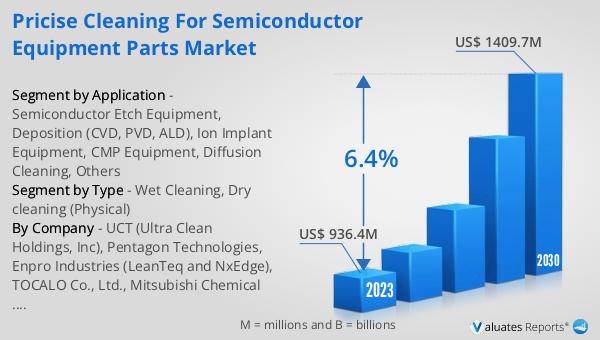

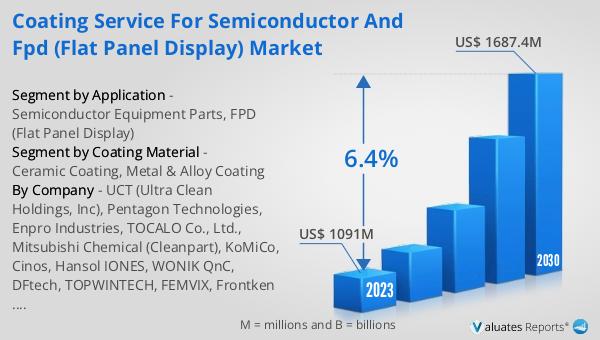

The global Cleaning for Semiconductor and Display Equipment Parts market was valued at US$ 1236.4 million in 2023 and is anticipated to reach US$ 1822.4 million by 2030, witnessing a CAGR of 5.8% during the forecast period 2024-2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased 5% from $102.6 billion in 2021 to an all-time record of $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022, despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings.

| Report Metric | Details |

| Report Name | Cleaning for Semiconductor and Display Equipment Parts Market |

| Accounted market size in 2023 | US$ 1236.4 million |

| Forecasted market size in 2030 | US$ 1822.4 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | UCT (Ultra Clean Holdings, Inc), Pentagon Technologies, Enpro Industries (LeanTeq and NxEdge), TOCALO Co., Ltd., Mitsubishi Chemical (Cleanpart), KoMiCo, Cinos, Hansol IONES, WONIK QnC, DFtech, Frontken Corporation Berhad, Value Engineering Co., Ltd, Neutron Technology Enterprise, JST Manufacturing, TOPWINTECH, Shih Her Technology, KERTZ HIGH TECH, Hung Jie Technology Corporation, Jiangsu Kaiweitesi Semiconductor Technology Co., Ltd., HCUT Co., Ltd, Ferrotec (Anhui) Technology Development Co., Ltd, Shanghai Companion, Shanghai Yingyou Optoelectronics Technology, Suzhou KemaTek, Inc., Anhui Veritech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |