What is Global Paper Dryer Stripping Agent Market?

The Global Paper Dryer Stripping Agent Market is a specialized segment within the broader chemicals and materials industry. These agents are essential in the paper manufacturing process, particularly during the drying phase. They help in efficiently removing water from the paper, ensuring that the final product is of high quality and free from defects. The market for these agents is driven by the increasing demand for paper products across various sectors, including packaging, printing, and hygiene products. The growth in e-commerce and the need for sustainable packaging solutions have further fueled the demand for paper dryer stripping agents. Additionally, advancements in technology and the development of more efficient and environmentally friendly agents are contributing to the market's expansion. The market is characterized by a diverse range of products, each tailored to meet specific requirements of different types of paper and manufacturing processes. Companies operating in this market are continuously investing in research and development to innovate and improve the performance of their products.

Polymer Wax, Mineral Oil, Vegetable Oil, Silicone, Polyether, Others in the Global Paper Dryer Stripping Agent Market:

Polymer wax, mineral oil, vegetable oil, silicone, polyether, and other materials play crucial roles in the Global Paper Dryer Stripping Agent Market. Polymer waxes are widely used due to their excellent water-repellent properties and ability to enhance the smoothness and gloss of the paper. They are particularly effective in high-speed paper machines where quick drying is essential. Mineral oils, on the other hand, are favored for their lubricating properties, which help in reducing friction during the drying process, thereby preventing damage to the paper. Vegetable oils are gaining popularity as eco-friendly alternatives to synthetic materials. They are biodegradable and derived from renewable sources, making them a sustainable choice for environmentally conscious manufacturers. Silicone-based agents are known for their high thermal stability and resistance to oxidation, making them ideal for use in high-temperature drying processes. They also provide excellent release properties, ensuring that the paper does not stick to the drying cylinders. Polyether-based agents are valued for their versatility and ability to form stable emulsions, which are essential for uniform application and consistent performance. Other materials used in the market include various synthetic and natural compounds that offer unique benefits such as enhanced durability, improved printability, and reduced energy consumption. Each of these materials has its own set of advantages and is chosen based on the specific requirements of the paper manufacturing process. Companies in this market are constantly exploring new formulations and combinations of these materials to develop more efficient and cost-effective stripping agents. The choice of material often depends on factors such as the type of paper being produced, the speed and temperature of the drying process, and environmental regulations. As the demand for high-quality paper products continues to grow, the importance of selecting the right stripping agent becomes even more critical. Manufacturers are increasingly looking for agents that not only improve the efficiency of the drying process but also enhance the overall quality and performance of the final product.

Paper Industry, Chemical Industry in the Global Paper Dryer Stripping Agent Market:

The usage of Global Paper Dryer Stripping Agents in the paper industry is extensive and multifaceted. These agents are integral to the drying process, ensuring that the paper is dried uniformly and efficiently. In the paper industry, the primary function of these agents is to facilitate the removal of water from the paper web during the drying phase. This is crucial because any residual moisture can lead to defects such as curling, warping, or uneven texture, which can compromise the quality of the final product. By using stripping agents, manufacturers can achieve a smoother, more consistent finish, which is essential for high-quality printing and packaging applications. Additionally, these agents help in reducing the energy consumption of the drying process, making it more cost-effective and environmentally friendly. In the chemical industry, paper dryer stripping agents are used in the production of various specialty papers and paper-based products. These include coated papers, thermal papers, and other high-performance materials that require precise control over the drying process. The chemical properties of the stripping agents play a crucial role in determining the final characteristics of these products, such as their strength, durability, and printability. For instance, in the production of thermal papers, which are used in receipts and labels, the stripping agents ensure that the paper dries quickly and evenly, preventing any smudging or blurring of the printed text. Similarly, in the production of coated papers, which are used in magazines and brochures, the agents help in achieving a smooth, glossy finish that enhances the visual appeal of the printed images. Overall, the use of paper dryer stripping agents in both the paper and chemical industries is essential for maintaining high standards of quality and performance.

Global Paper Dryer Stripping Agent Market Outlook:

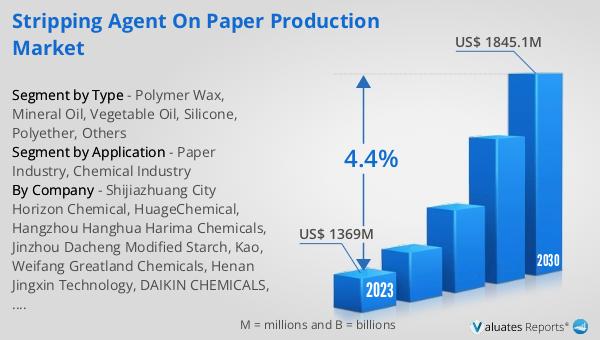

The global Paper Dryer Stripping Agent market was valued at US$ 1369 million in 2023 and is anticipated to reach US$ 1845.1 million by 2030, witnessing a CAGR of 4.4% during the forecast period 2024-2030. This growth trajectory highlights the increasing demand for these agents across various industries, driven by the need for high-quality paper products and efficient manufacturing processes. The market's expansion is also supported by technological advancements and the development of more sustainable and environmentally friendly stripping agents. Companies operating in this market are focusing on innovation and research to meet the evolving needs of their customers and to stay competitive. The projected growth in market value reflects the critical role that paper dryer stripping agents play in the paper manufacturing process, ensuring that the final products meet the highest standards of quality and performance. As the demand for paper products continues to rise, particularly in the packaging and printing sectors, the importance of these agents is expected to grow even further.

| Report Metric | Details |

| Report Name | Paper Dryer Stripping Agent Market |

| Accounted market size in 2023 | US$ 1369 million |

| Forecasted market size in 2030 | US$ 1845.1 million |

| CAGR | 4.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Shijiazhuang City Horizon Chemical, HuageChemical, Hangzhou Hanghua Harima Chemicals, Jinzhou Dacheng Modified Starch, Kao, Weifang Greatland Chemicals, Henan Jingxin Technology, DAIKIN CHEMICALS, DOW, Hitac Adhesives and Coatings, SEIKO PMC Corporation, Dainichi Chemical, Münzing Chemie |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |