What is Global Stripping Agent On Paper Production Market?

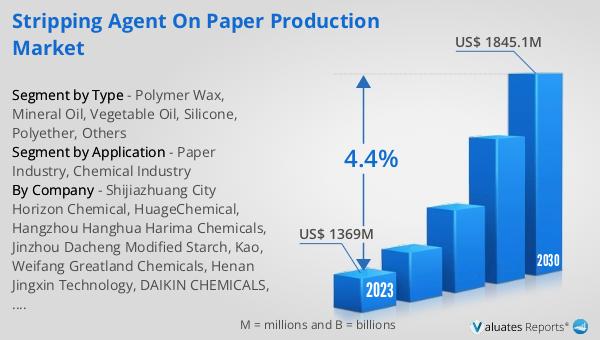

The global Stripping Agent On Paper Production market was valued at US$ 1369 million in 2023 and is anticipated to reach US$ 1845.1 million by 2030, witnessing a CAGR of 4.4% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by increasing demand for high-quality paper products and advancements in paper production technologies. Stripping agents play a crucial role in the paper manufacturing process by helping to remove unwanted substances and improve the quality of the final product. The projected growth in this market is a testament to the ongoing innovations and the rising need for efficient and effective paper production methods. As industries continue to evolve and the demand for paper products remains robust, the importance of stripping agents in ensuring the production of superior paper quality cannot be overstated. This growth is also reflective of the broader trends in the paper industry, where sustainability and efficiency are becoming increasingly important. The market's expansion is expected to bring about new opportunities for manufacturers and suppliers of stripping agents, as they strive to meet the evolving needs of the paper production industry.

Polymer Wax, Mineral Oil, Vegetable Oil, Silicone, Polyether, Others in the Global Stripping Agent On Paper Production Market:

The Global Stripping Agent On Paper Production Market encompasses a variety of materials, each with unique properties and applications. Polymer wax, for instance, is widely used due to its excellent lubricating and release properties, which help in the smooth separation of paper layers during production. This material is particularly valued for its ability to enhance the surface quality of paper, making it smoother and more uniform. Mineral oil, on the other hand, is known for its effectiveness in reducing friction and preventing the buildup of unwanted residues on machinery, thereby ensuring a more efficient production process. Vegetable oil, derived from natural sources, is gaining popularity due to its eco-friendly nature and biodegradability. It serves as an effective stripping agent while also aligning with the growing trend towards sustainable and environmentally friendly production practices. Silicone-based stripping agents are prized for their high thermal stability and excellent release properties, making them ideal for high-temperature paper production processes. Polyether, another important material, is known for its versatility and effectiveness in various paper production applications. It helps in reducing the adhesion between paper layers, thereby facilitating easier separation and handling. Other materials used as stripping agents include a range of synthetic and natural compounds, each selected based on specific production requirements and desired paper qualities. The choice of stripping agent can significantly impact the efficiency of the production process, the quality of the final product, and the overall sustainability of the manufacturing operations. As the paper production industry continues to evolve, the demand for innovative and effective stripping agents is expected to grow, driving further advancements in this market.

Paper Industry, Chemical Industry in the Global Stripping Agent On Paper Production Market:

The usage of Global Stripping Agent On Paper Production Market in the Paper Industry is pivotal for ensuring the production of high-quality paper products. Stripping agents are essential in the paper manufacturing process as they help in the removal of unwanted substances such as adhesives, inks, and coatings from the paper surface. This not only improves the quality and appearance of the final product but also enhances the efficiency of the production process by preventing the buildup of residues on machinery. In the Chemical Industry, stripping agents are used in various applications, including the production of specialty chemicals and the treatment of industrial waste. They play a crucial role in the purification and separation processes, helping to remove impurities and unwanted by-products. This ensures that the final chemical products meet the required quality standards and are free from contaminants. The use of stripping agents in these industries is driven by the need for efficient and effective production processes, as well as the growing demand for high-quality products. As industries continue to evolve and the demand for sustainable and environmentally friendly production practices increases, the importance of stripping agents in ensuring the production of superior quality products cannot be overstated. The ongoing advancements in stripping agent technologies are expected to further enhance their effectiveness and efficiency, driving growth in the Global Stripping Agent On Paper Production Market.

Global Stripping Agent On Paper Production Market Outlook:

English: #MarketResearch #PaperProduction #StrippingAgents #PolymerWax #MineralOil #VegetableOil #Silicone #Polyether #ChemicalIndustry #SustainableProduction

| Report Metric | Details |

| Report Name | Stripping Agent On Paper Production Market |

| Accounted market size in 2023 | US$ 1369 million |

| Forecasted market size in 2030 | US$ 1845.1 million |

| CAGR | 4.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Shijiazhuang City Horizon Chemical, HuageChemical, Hangzhou Hanghua Harima Chemicals, Jinzhou Dacheng Modified Starch, Kao, Weifang Greatland Chemicals, Henan Jingxin Technology, DAIKIN CHEMICALS, DOW, Hitac Adhesives and Coatings, SEIKO PMC Corporation, Dainichi Chemical, Münzing Chemie |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |