What is Global Stereoscopic Cinema Market?

The Global Stereoscopic Cinema Market refers to the industry that produces and distributes films and other visual content using stereoscopic technology. This technology creates the illusion of depth in an image by presenting two offset images separately to the left and right eye of the viewer. The brain then combines these two images to create a perception of 3D depth. This market encompasses various aspects, including the production of stereoscopic films, the development of specialized cameras and equipment, and the distribution and exhibition of these films in cinemas and other venues. The demand for immersive and engaging viewing experiences has driven the growth of this market, with advancements in technology making stereoscopic cinema more accessible and appealing to a broader audience. The market also includes the development of software and tools for creating and editing stereoscopic content, as well as the training and education of professionals in the field. Overall, the Global Stereoscopic Cinema Market is a dynamic and evolving industry that continues to innovate and expand, offering new opportunities for filmmakers, technology developers, and audiences alike.

Digital 3D Version, IMAX/IMAX 3D in the Global Stereoscopic Cinema Market:

Digital 3D and IMAX/IMAX 3D are two prominent formats within the Global Stereoscopic Cinema Market that have significantly contributed to its growth and popularity. Digital 3D refers to the use of digital projection technology to display 3D films. Unlike traditional film-based 3D, digital 3D offers higher quality images, better color accuracy, and more consistent performance. This format uses polarized glasses to separate the left and right eye images, creating a seamless and immersive 3D experience. Digital 3D has become the standard for most modern 3D films, with many cinemas around the world equipped with the necessary technology to screen these films. On the other hand, IMAX/IMAX 3D represents a premium format that offers an even more immersive experience. IMAX theaters are known for their large screens, high-resolution projection systems, and powerful sound systems. IMAX 3D takes this experience to the next level by incorporating stereoscopic 3D technology. The combination of the large screen, high resolution, and 3D effects creates a truly immersive experience that is unmatched by other formats. IMAX 3D films are often shot using specialized IMAX cameras, which capture more detail and provide a higher quality image. This format is particularly popular for blockbuster films and major releases, as it offers a unique and memorable viewing experience. Both Digital 3D and IMAX/IMAX 3D have played a crucial role in the growth of the Global Stereoscopic Cinema Market, attracting audiences with their enhanced visual and auditory experiences. These formats have also driven innovation in the industry, leading to the development of new technologies and techniques for creating and displaying 3D content. As a result, the Global Stereoscopic Cinema Market continues to evolve and expand, offering new opportunities for filmmakers, technology developers, and audiences alike.

Cinema, Entertainment Venue, Residential, Others in the Global Stereoscopic Cinema Market:

The usage of the Global Stereoscopic Cinema Market extends beyond traditional cinema settings, finding applications in various areas such as entertainment venues, residential settings, and other sectors. In cinemas, stereoscopic technology has revolutionized the movie-going experience by providing audiences with immersive and engaging 3D films. This has led to an increase in ticket sales and the popularity of 3D movies, as viewers seek out the enhanced visual experience that stereoscopic cinema offers. Cinemas have invested in specialized equipment, such as 3D projectors and polarized glasses, to accommodate the growing demand for 3D films. In entertainment venues, such as theme parks and museums, stereoscopic cinema is used to create captivating and educational experiences. For example, 3D films and simulations are often featured in theme park attractions, providing visitors with thrilling and realistic experiences. Museums use stereoscopic technology to enhance exhibits, allowing visitors to explore historical events, natural wonders, and scientific phenomena in a more interactive and engaging way. In residential settings, the adoption of stereoscopic technology has been driven by the availability of 3D televisions and home theater systems. Consumers can now enjoy 3D movies and content from the comfort of their own homes, creating a more immersive and enjoyable viewing experience. This has led to an increase in the production and distribution of 3D Blu-ray discs and streaming services that offer 3D content. Additionally, the Global Stereoscopic Cinema Market has found applications in other sectors, such as education and healthcare. In education, stereoscopic technology is used to create interactive and engaging learning experiences, helping students to better understand complex concepts and visualize abstract ideas. In healthcare, 3D imaging and simulations are used for medical training and surgical planning, providing doctors and medical professionals with more accurate and detailed visual information. Overall, the usage of the Global Stereoscopic Cinema Market in various areas highlights its versatility and potential for creating immersive and engaging experiences across different sectors.

Global Stereoscopic Cinema Market Outlook:

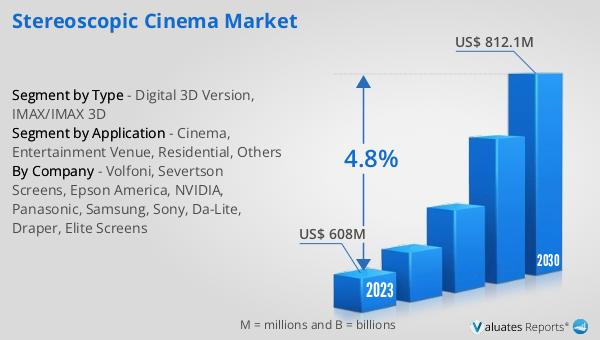

The global Stereoscopic Cinema market was valued at US$ 608 million in 2023 and is anticipated to reach US$ 812.1 million by 2030, witnessing a CAGR of 4.8% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by the increasing demand for immersive and engaging viewing experiences. The advancements in stereoscopic technology, coupled with the growing popularity of 3D films, have contributed to the market's expansion. The adoption of stereoscopic cinema in various sectors, such as entertainment venues, residential settings, and education, has further fueled its growth. As more cinemas and entertainment venues invest in specialized equipment and technology to accommodate 3D films, the market is expected to continue its upward trend. Additionally, the availability of 3D televisions and home theater systems has made stereoscopic content more accessible to consumers, driving demand in the residential sector. The use of stereoscopic technology in education and healthcare also highlights its potential for creating interactive and engaging experiences in these fields. Overall, the global Stereoscopic Cinema market is poised for significant growth, offering new opportunities for filmmakers, technology developers, and audiences alike.

| Report Metric | Details |

| Report Name | Stereoscopic Cinema Market |

| Accounted market size in 2023 | US$ 608 million |

| Forecasted market size in 2030 | US$ 812.1 million |

| CAGR | 4.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Volfoni, Severtson Screens, Epson America, NVIDIA, Panasonic, Samsung, Sony, Da-Lite, Draper, Elite Screens |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |