What is Global Pharmaceutical Automatic Light Inspection Machine Market?

The Global Pharmaceutical Automatic Light Inspection Machine Market refers to the industry focused on the production and distribution of machines designed to inspect pharmaceutical products using light-based technology. These machines are essential in ensuring the quality and safety of pharmaceutical products by detecting defects such as cracks, foreign particles, and other inconsistencies in vials, ampoules, and syringes. The market encompasses a variety of machines, including fully automated and semi-automated systems, which are used by pharmaceutical companies, biotechnology firms, and medical device manufacturers. The demand for these machines is driven by the increasing need for stringent quality control measures in the pharmaceutical industry, regulatory requirements, and the growing production of injectable drugs. The market is characterized by technological advancements, with manufacturers continuously innovating to improve the accuracy, speed, and efficiency of these inspection machines.

Fully Automated Light Inspection Machine, Semi-Automated Light Inspection Machine in the Global Pharmaceutical Automatic Light Inspection Machine Market:

Fully Automated Light Inspection Machines are advanced systems designed to perform the inspection process without human intervention. These machines use sophisticated imaging technology and algorithms to detect defects in pharmaceutical products with high precision. They are capable of inspecting a large number of products in a short period, making them ideal for high-volume production lines. The fully automated systems are equipped with features such as high-resolution cameras, advanced lighting systems, and software that can analyze images in real-time. These machines can detect a wide range of defects, including cracks, chips, foreign particles, and cosmetic imperfections. The primary advantage of fully automated systems is their ability to provide consistent and reliable inspection results, reducing the risk of human error. They also offer the benefit of increased efficiency and productivity, as they can operate continuously without the need for breaks. On the other hand, Semi-Automated Light Inspection Machines require some level of human intervention during the inspection process. These machines are typically used in smaller production facilities or for products that require a more hands-on approach. Semi-automated systems combine manual and automated processes, where the machine performs the initial inspection, and a human operator verifies the results. This hybrid approach allows for greater flexibility and can be more cost-effective for smaller batches of products. Semi-automated machines are often used for products that are difficult to inspect using fully automated systems or for applications where a high level of customization is required. Both fully automated and semi-automated light inspection machines play a crucial role in the pharmaceutical industry by ensuring the quality and safety of products. The choice between the two types of machines depends on various factors, including the volume of production, the complexity of the products being inspected, and the specific requirements of the manufacturing process.

Pharmaceutical, Biotechnology, Medical Device, Others in the Global Pharmaceutical Automatic Light Inspection Machine Market:

The usage of Global Pharmaceutical Automatic Light Inspection Machines spans across various sectors, including pharmaceuticals, biotechnology, medical devices, and others. In the pharmaceutical industry, these machines are essential for ensuring the quality and safety of injectable drugs. They are used to inspect vials, ampoules, and syringes for defects such as cracks, chips, and foreign particles. The stringent regulatory requirements in the pharmaceutical industry necessitate the use of advanced inspection technologies to ensure that products meet the highest standards of quality and safety. In the biotechnology sector, automatic light inspection machines are used to inspect biologics and biosimilars. These products are often more complex than traditional pharmaceuticals and require advanced inspection technologies to detect even the smallest defects. The use of automatic light inspection machines in biotechnology helps to ensure the safety and efficacy of these products, which is critical given their use in treating serious medical conditions. In the medical device industry, automatic light inspection machines are used to inspect a wide range of products, including syringes, catheters, and implantable devices. These machines help to ensure that medical devices are free from defects and meet the stringent quality standards required for use in medical procedures. The use of automatic light inspection machines in the medical device industry helps to reduce the risk of product recalls and ensures that patients receive safe and effective medical devices. Other sectors that use automatic light inspection machines include the food and beverage industry, where they are used to inspect packaging for defects, and the cosmetics industry, where they are used to inspect containers for cracks and other imperfections. The versatility of automatic light inspection machines makes them valuable tools in a wide range of industries, helping to ensure the quality and safety of products.

Global Pharmaceutical Automatic Light Inspection Machine Market Outlook:

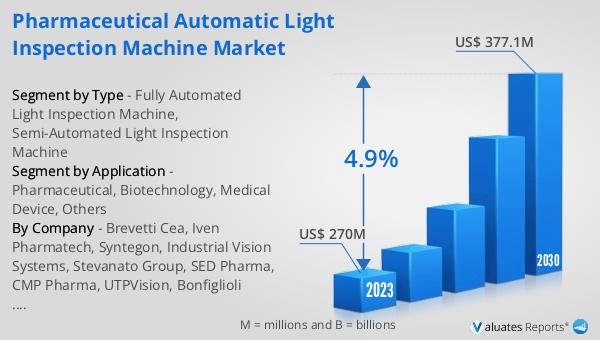

The global Pharmaceutical Automatic Light Inspection Machine market was valued at US$ 270 million in 2023 and is anticipated to reach US$ 377.1 million by 2030, witnessing a CAGR of 4.9% during the forecast period 2024-2030. This market growth is driven by the increasing demand for high-quality pharmaceutical products and the need for stringent quality control measures. The adoption of advanced inspection technologies by pharmaceutical companies, biotechnology firms, and medical device manufacturers is expected to fuel the growth of this market. The market is characterized by continuous technological advancements, with manufacturers focusing on developing more efficient and accurate inspection machines. The growing production of injectable drugs and the increasing regulatory requirements for quality control are also contributing to the market's growth. As the pharmaceutical industry continues to expand, the demand for automatic light inspection machines is expected to rise, driving further innovation and development in this market.

| Report Metric | Details |

| Report Name | Pharmaceutical Automatic Light Inspection Machine Market |

| Accounted market size in 2023 | US$ 270 million |

| Forecasted market size in 2030 | US$ 377.1 million |

| CAGR | 4.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Brevetti Cea, Iven Pharmatech, Syntegon, Industrial Vision Systems, Stevanato Group, SED Pharma, CMP Pharma, UTPVision, Bonfiglioli Engineering, Körber Pharma, Tofflon, Truking Technology, ANTARES VISION, FE Pharmatech, CMP PHAR.MA SRL |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |