What is Global Biosourced Fragrance Market?

The Global Biosourced Fragrance Market refers to the industry that produces and sells fragrances derived from natural, renewable sources. These fragrances are extracted from plants, animals, and other natural materials, as opposed to synthetic fragrances created through chemical processes. The market for biosourced fragrances is growing due to increasing consumer demand for natural and sustainable products. Consumers are becoming more aware of the environmental and health impacts of synthetic chemicals, leading to a preference for natural alternatives. Biosourced fragrances are used in a wide range of products, including perfumes, cosmetics, food and beverages, and household products. The market is characterized by a diverse range of products and a high level of innovation, as companies continuously seek new sources and methods for extracting natural fragrances. The global biosourced fragrance market is also influenced by regulatory standards and certifications that ensure the authenticity and sustainability of natural products.

Botanical Source, Animal Source in the Global Biosourced Fragrance Market:

Botanical sources in the Global Biosourced Fragrance Market include a wide variety of plants, flowers, fruits, and herbs. These natural materials are harvested and processed to extract essential oils and other aromatic compounds. Common botanical sources include lavender, rose, jasmine, citrus fruits, and mint. These plants are often grown in specific regions known for their optimal growing conditions, such as the lavender fields of Provence or the rose gardens of Bulgaria. The extraction process can vary, but it typically involves methods like steam distillation, cold pressing, or solvent extraction. Each method has its advantages and is chosen based on the type of plant material and the desired fragrance profile. Botanical fragrances are highly valued for their complexity and depth, offering a wide range of scent notes from floral and fruity to woody and spicy. On the other hand, animal sources for biosourced fragrances are less common but have a long history in perfumery. Traditional animal-derived fragrances include musk, ambergris, and civet. These substances are secreted by animals and have unique scent profiles that are difficult to replicate synthetically. However, the use of animal-derived fragrances has declined due to ethical concerns and animal welfare regulations. Many companies now use synthetic alternatives or plant-based substitutes that mimic the scent of these traditional animal-derived fragrances. The shift towards ethical and sustainable practices has led to increased research and development in finding new botanical sources that can replace animal-derived ingredients. This has also spurred innovation in extraction techniques and the development of new fragrance compounds. Overall, both botanical and animal sources play a crucial role in the Global Biosourced Fragrance Market, offering a diverse range of scents that cater to different consumer preferences and ethical considerations.

Food and Drink, Daily Chemicals, Others in the Global Biosourced Fragrance Market:

The Global Biosourced Fragrance Market finds extensive usage in various sectors, including food and drink, daily chemicals, and other miscellaneous applications. In the food and drink industry, biosourced fragrances are used to enhance the flavor and aroma of products. Natural extracts from fruits, herbs, and spices are commonly used in beverages, confectionery, and baked goods to provide a more authentic and appealing taste experience. For example, vanilla extract, derived from vanilla beans, is a popular ingredient in many desserts and beverages. Similarly, citrus oils are used to add a fresh and zesty flavor to soft drinks and candies. The use of biosourced fragrances in food and drink products is often preferred due to their natural origin and perceived health benefits compared to synthetic additives. In the daily chemicals sector, biosourced fragrances are widely used in personal care products, household cleaners, and laundry detergents. Consumers are increasingly seeking products that are not only effective but also environmentally friendly and safe for their health. Natural fragrances derived from plants and flowers are used in shampoos, soaps, lotions, and deodorants to provide a pleasant scent while also offering potential therapeutic benefits. For instance, lavender oil is known for its calming properties and is commonly used in personal care products to promote relaxation. In household cleaners and laundry detergents, biosourced fragrances help mask unpleasant odors and leave a fresh, clean scent. The use of natural fragrances in these products aligns with the growing trend towards green and sustainable living. Beyond food and drink and daily chemicals, biosourced fragrances are also used in a variety of other applications. These include aromatherapy, where essential oils are used for their therapeutic properties to improve mental and physical well-being. Natural fragrances are also used in candles, air fresheners, and other home fragrance products to create a pleasant and inviting atmosphere. Additionally, biosourced fragrances are used in the production of natural insect repellents, leveraging the repellent properties of certain plant extracts. Overall, the versatility and natural appeal of biosourced fragrances make them a popular choice across multiple industries, catering to the growing consumer demand for natural and sustainable products.

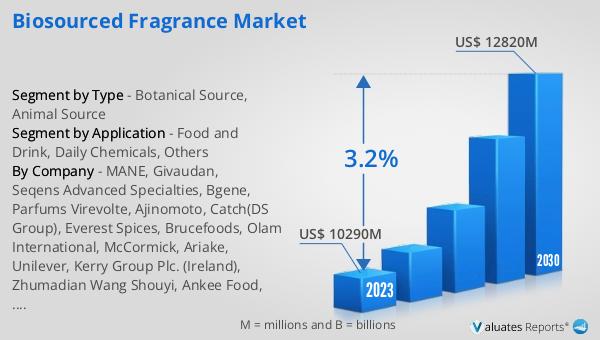

Global Biosourced Fragrance Market Outlook:

The global biosourced fragrance market was valued at approximately $10.29 billion in 2023 and is projected to reach around $12.82 billion by 2030, reflecting a compound annual growth rate (CAGR) of 3.2% during the forecast period from 2024 to 2030. This growth is driven by increasing consumer preference for natural and sustainable products, as well as advancements in extraction and production technologies. The market's expansion is also supported by the rising awareness of the environmental and health impacts of synthetic fragrances, leading to a shift towards natural alternatives. Companies in the biosourced fragrance market are continuously innovating to meet the evolving demands of consumers, developing new products and exploring new sources of natural fragrances. Regulatory standards and certifications play a crucial role in ensuring the authenticity and sustainability of biosourced fragrances, further boosting consumer confidence and market growth. The market's steady growth trajectory indicates a promising future for biosourced fragrances, as more consumers and industries embrace natural and eco-friendly products.

| Report Metric | Details |

| Report Name | Biosourced Fragrance Market |

| Accounted market size in 2023 | US$ 10290 million |

| Forecasted market size in 2030 | US$ 12820 million |

| CAGR | 3.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | MANE, Givaudan, Seqens Advanced Specialties, Bgene, Parfums Virevolte, Ajinomoto, Catch(DS Group), Everest Spices, Brucefoods, Olam International, McCormick, Ariake, Unilever, Kerry Group Plc. (Ireland), Zhumadian Wang Shouyi, Ankee Food, Nestle |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |