What is Global Soy Plant Protein Market?

The Global Soy Plant Protein Market refers to the worldwide industry focused on the production, distribution, and consumption of soy-based protein products. Soy plant protein is derived from soybeans and is a popular alternative to animal-based proteins due to its nutritional benefits, including high protein content, essential amino acids, and low fat. This market encompasses various forms of soy protein, such as soy protein concentrate, soy protein isolate, and textured soy protein, which are used in a wide range of applications. The demand for soy plant protein is driven by the growing trend towards plant-based diets, increasing awareness of health and wellness, and the need for sustainable food sources. The market is also influenced by factors such as technological advancements in food processing, the rise of vegan and vegetarian lifestyles, and the expanding use of soy protein in various industries, including food and beverages, health products, and animal feed. As consumers become more health-conscious and environmentally aware, the Global Soy Plant Protein Market is expected to continue its growth trajectory, offering numerous opportunities for innovation and development in the coming years.

Concentrated Protein, Isolate Protein, Tissue Protein in the Global Soy Plant Protein Market:

Concentrated Protein, Isolate Protein, and Tissue Protein are three primary forms of soy plant protein that play significant roles in the Global Soy Plant Protein Market. Concentrated Protein, also known as soy protein concentrate, is produced by removing the soluble carbohydrates from defatted soy flour, resulting in a product that contains about 70% protein. This type of protein retains most of the soy's fiber and is commonly used in food products such as baked goods, cereals, and meat analogs due to its functional properties like water retention and emulsification. Soy Protein Isolate, on the other hand, is a more refined form of soy protein, containing at least 90% protein. It is made by further processing soy protein concentrate to remove almost all fats and carbohydrates, leaving a highly pure protein product. This form is often used in high-protein foods, beverages, and supplements, as it provides a high-quality protein source with minimal taste and color impact. Textured Soy Protein, also known as tissue protein, is created by processing soy flour into a fibrous, meat-like texture. This type of protein is widely used in meat substitutes and extenders, offering a plant-based alternative that mimics the texture and mouthfeel of meat. Each of these soy protein forms has unique characteristics and applications, making them versatile ingredients in the food industry. The growing demand for plant-based proteins has led to increased innovation and development in these soy protein products, catering to the diverse needs of consumers seeking healthy, sustainable, and functional food options.

Food and Drink, Health Products, Feed, Others in the Global Soy Plant Protein Market:

The usage of Global Soy Plant Protein Market spans across various sectors, including Food and Drink, Health Products, Feed, and others. In the Food and Drink sector, soy plant protein is extensively used to create a wide range of products such as meat substitutes, dairy alternatives, protein bars, and beverages. Its high protein content and functional properties make it an ideal ingredient for enhancing the nutritional profile of foods while catering to the growing demand for plant-based diets. Soy protein is also used in baked goods, snacks, and cereals, providing a versatile and nutritious option for consumers. In the Health Products sector, soy plant protein is a popular ingredient in dietary supplements, protein powders, and meal replacement products. Its complete amino acid profile and easy digestibility make it a preferred choice for athletes, fitness enthusiasts, and individuals seeking to improve their overall health and wellness. Soy protein is also associated with various health benefits, including heart health, weight management, and muscle recovery, further driving its usage in health products. In the Feed sector, soy plant protein is a valuable source of protein for animal feed, particularly in livestock and aquaculture industries. It provides essential nutrients for animal growth and development, contributing to the overall efficiency and sustainability of animal farming. Additionally, soy protein is used in pet food formulations, offering a high-quality protein source for pets. Beyond these primary sectors, soy plant protein finds applications in other areas such as pharmaceuticals, cosmetics, and industrial products. Its versatility and functional properties make it a valuable ingredient in various formulations, driving its demand across multiple industries. As the awareness of the benefits of plant-based proteins continues to grow, the usage of soy plant protein is expected to expand further, offering numerous opportunities for innovation and development.

Global Soy Plant Protein Market Outlook:

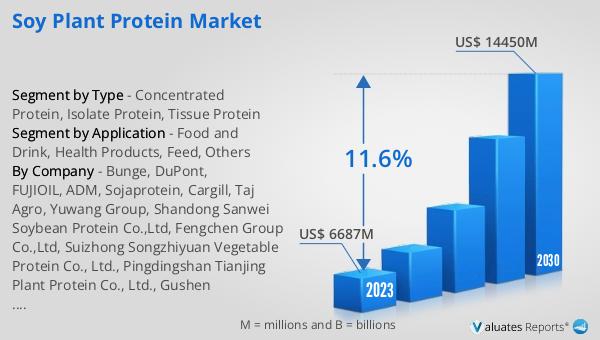

The global Soy Plant Protein market was valued at US$ 6687 million in 2023 and is anticipated to reach US$ 14450 million by 2030, witnessing a CAGR of 11.6% during the forecast period 2024-2030. This significant growth reflects the increasing consumer demand for plant-based protein sources, driven by health consciousness, environmental concerns, and the rising popularity of vegan and vegetarian diets. The market's expansion is also supported by advancements in food technology and processing methods, which have improved the quality and functionality of soy protein products. As more consumers seek sustainable and nutritious food options, the soy plant protein market is poised to experience robust growth, offering a wide range of opportunities for manufacturers, suppliers, and innovators in the industry. The projected growth underscores the importance of soy plant protein as a key component in the global shift towards more sustainable and health-conscious food systems.

| Report Metric | Details |

| Report Name | Soy Plant Protein Market |

| Accounted market size in 2023 | US$ 6687 million |

| Forecasted market size in 2030 | US$ 14450 million |

| CAGR | 11.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bunge, DuPont, FUJIOIL, ADM, Sojaprotein, Cargill, Taj Agro, Yuwang Group, Shandong Sanwei Soybean Protein Co.,Ltd, Fengchen Group Co.,Ltd, Suizhong Songzhiyuan Vegetable Protein Co., Ltd., Pingdingshan Tianjing Plant Protein Co., Ltd., Gushen Biotechnology Group Co., Ltd., Jiangsu Haozhi Health Technology Co., Ltd., Shandong Wandefu Industrial Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |