What is Global Electronic Clutch Water Pump Market?

The Global Electronic Clutch Water Pump Market refers to the industry focused on the production and distribution of water pumps that utilize electronic clutches. These pumps are primarily used in automotive applications to manage the flow of coolant within the engine, thereby optimizing engine performance and fuel efficiency. Unlike traditional water pumps that operate continuously, electronic clutch water pumps can be engaged or disengaged based on the engine's cooling needs. This selective operation helps in reducing energy consumption and emissions, making vehicles more environmentally friendly. The market for these advanced water pumps is growing rapidly due to increasing demand for fuel-efficient and eco-friendly vehicles. Technological advancements and stringent emission regulations are also driving the adoption of electronic clutch water pumps across various regions. The market encompasses a wide range of products, including pumps for passenger vehicles, commercial vehicles, and specialized applications, making it a crucial component of the modern automotive industry.

Mechanical Clutch Water Pump, Hydraulic Clutch Water Pump in the Global Electronic Clutch Water Pump Market:

The Global Electronic Clutch Water Pump Market includes various types of water pumps, such as Mechanical Clutch Water Pumps and Hydraulic Clutch Water Pumps. Mechanical Clutch Water Pumps operate using a mechanical linkage to engage or disengage the pump based on the engine's cooling requirements. These pumps are typically more straightforward in design and are often used in older vehicle models or in applications where cost is a significant concern. They offer reliable performance but may not provide the same level of efficiency as their electronic counterparts. On the other hand, Hydraulic Clutch Water Pumps use hydraulic fluid to control the engagement and disengagement of the pump. These pumps are more complex and can offer better performance and efficiency compared to mechanical pumps. They are often used in high-performance vehicles or in applications where precise control over the cooling system is required. Both types of pumps play a crucial role in the overall functionality of the vehicle's cooling system, ensuring that the engine operates within the optimal temperature range. The choice between mechanical and hydraulic clutch water pumps often depends on the specific requirements of the vehicle and the preferences of the manufacturer. As the automotive industry continues to evolve, there is a growing trend towards the adoption of more advanced and efficient water pump technologies, including electronic clutch water pumps. These pumps offer several advantages over traditional mechanical and hydraulic pumps, including improved fuel efficiency, reduced emissions, and enhanced engine performance. The increasing focus on sustainability and environmental regulations is also driving the demand for these advanced water pump solutions. Overall, the Global Electronic Clutch Water Pump Market is characterized by a diverse range of products and technologies, each offering unique benefits and applications.

Passenger Vehicle, Commercial Vehicle in the Global Electronic Clutch Water Pump Market:

The usage of Global Electronic Clutch Water Pump Market in passenger vehicles and commercial vehicles is significant and varied. In passenger vehicles, electronic clutch water pumps are primarily used to enhance fuel efficiency and reduce emissions. These pumps can be precisely controlled to operate only when needed, thereby reducing the load on the engine and improving overall vehicle performance. This is particularly important in modern passenger vehicles, where there is a growing emphasis on sustainability and environmental responsibility. The ability to optimize the cooling system also contributes to a more comfortable driving experience, as it helps maintain the engine at an optimal temperature, reducing the risk of overheating and improving the longevity of the vehicle. In commercial vehicles, the benefits of electronic clutch water pumps are equally compelling. These vehicles often operate under more demanding conditions and require robust and reliable cooling systems to ensure consistent performance. Electronic clutch water pumps provide the necessary control and efficiency to manage the cooling needs of commercial vehicles, which can vary significantly depending on the load and driving conditions. By optimizing the cooling system, these pumps help improve fuel efficiency and reduce maintenance costs, which are critical factors for commercial vehicle operators. Additionally, the use of electronic clutch water pumps in commercial vehicles can contribute to lower emissions, helping companies meet regulatory requirements and reduce their environmental impact. Overall, the adoption of electronic clutch water pumps in both passenger and commercial vehicles is driven by the need for improved efficiency, performance, and sustainability. As the automotive industry continues to evolve, the demand for these advanced water pump solutions is expected to grow, further highlighting their importance in modern vehicle design and operation.

Global Electronic Clutch Water Pump Market Outlook:

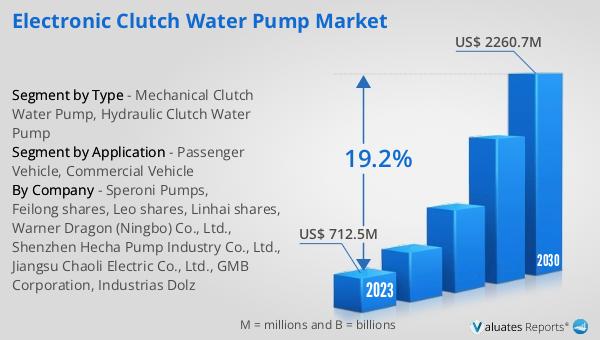

The global Electronic Clutch Water Pump market was valued at US$ 712.5 million in 2023 and is anticipated to reach US$ 2260.7 million by 2030, witnessing a CAGR of 19.2% during the forecast period 2024-2030. According to the China Machinery Industry Federation, the operating income of the construction machinery industry will drop by more than 12% in 2022. This significant growth in the Electronic Clutch Water Pump market can be attributed to several factors, including the increasing demand for fuel-efficient and eco-friendly vehicles, advancements in technology, and stringent emission regulations. The market's rapid expansion is also driven by the growing awareness of the benefits of electronic clutch water pumps, such as improved engine performance, reduced energy consumption, and lower emissions. As more automotive manufacturers and consumers recognize the advantages of these advanced water pump solutions, the market is expected to continue its upward trajectory. The decline in the construction machinery industry's operating income highlights the challenges faced by traditional industries, further emphasizing the need for innovative and efficient technologies like electronic clutch water pumps. Overall, the market outlook for the Global Electronic Clutch Water Pump Market is positive, with significant growth potential in the coming years.

| Report Metric | Details |

| Report Name | Electronic Clutch Water Pump Market |

| Accounted market size in 2023 | US$ 712.5 million |

| Forecasted market size in 2030 | US$ 2260.7 million |

| CAGR | 19.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Speroni Pumps, Feilong shares, Leo shares, Linhai shares, Warner Dragon (Ningbo) Co., Ltd., Shenzhen Hecha Pump Industry Co., Ltd., Jiangsu Chaoli Electric Co., Ltd., GMB Corporation, Industrias Dolz |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |