What is Global Ultrasonic Electrosurgical Unit Market?

The Global Ultrasonic Electrosurgical Unit Market refers to the worldwide industry focused on the development, production, and distribution of ultrasonic electrosurgical units. These units are advanced medical devices that utilize ultrasonic energy to cut, coagulate, dissect, and ablate tissues during surgical procedures. Unlike traditional electrosurgical units that use electrical currents, ultrasonic units employ high-frequency sound waves to achieve precise and controlled surgical outcomes. This technology is particularly valued for its ability to minimize thermal damage to surrounding tissues, reduce blood loss, and enhance surgical precision. The market encompasses a wide range of applications, including general surgery, gynecology, urology, and more, making it a critical component of modern surgical practices. The increasing demand for minimally invasive surgeries, coupled with advancements in medical technology, has significantly contributed to the growth of this market. Additionally, the rising prevalence of chronic diseases and the growing aging population are driving the need for more efficient and effective surgical solutions, further propelling the market's expansion.

Monopolar (Monopolar Cutting/Monopolar Coagulation), Bipolar (Bipolar Cutting/Bipolar Coagulation) in the Global Ultrasonic Electrosurgical Unit Market:

Monopolar and bipolar are two primary modalities used in ultrasonic electrosurgical units, each with distinct mechanisms and applications. Monopolar electrosurgery involves a single active electrode that delivers the ultrasonic energy to the target tissue, while a return electrode is placed elsewhere on the patient's body to complete the circuit. This method is commonly used for cutting and coagulating tissues. Monopolar cutting utilizes high-frequency ultrasonic waves to precisely cut through tissues with minimal thermal damage, making it ideal for procedures requiring fine incisions. Monopolar coagulation, on the other hand, focuses on controlling bleeding by coagulating blood vessels, which is crucial in surgeries where blood loss needs to be minimized. Bipolar electrosurgery, in contrast, uses two electrodes that are both placed at the surgical site. The ultrasonic energy passes between these electrodes, allowing for more localized and controlled tissue effects. Bipolar cutting is particularly useful in delicate surgeries where precision is paramount, such as neurosurgery or ophthalmic procedures. It offers the advantage of reducing the risk of unintended tissue damage and minimizing the spread of thermal energy. Bipolar coagulation is employed to achieve hemostasis by coagulating blood vessels within the surgical field, ensuring effective bleeding control. The choice between monopolar and bipolar modalities depends on the specific surgical requirements, with each offering unique benefits tailored to different types of procedures. The versatility and precision of these technologies have made them indispensable tools in modern surgical practices, contributing to improved patient outcomes and enhanced surgical efficiency.

Endoscopic Surgery, Cardiac Surgery, Dental Surgery, Cosmetic Surgery in the Global Ultrasonic Electrosurgical Unit Market:

The Global Ultrasonic Electrosurgical Unit Market finds extensive usage across various surgical disciplines, including endoscopic surgery, cardiac surgery, dental surgery, and cosmetic surgery. In endoscopic surgery, ultrasonic electrosurgical units are employed to perform minimally invasive procedures through small incisions, reducing patient recovery time and minimizing postoperative complications. The precision of ultrasonic energy allows for delicate tissue dissection and coagulation, making it ideal for procedures such as laparoscopic cholecystectomy, appendectomy, and colorectal surgery. In cardiac surgery, these units are used to perform intricate procedures on the heart and blood vessels. The ability to control bleeding and minimize thermal damage is crucial in this field, where precision and safety are paramount. Ultrasonic electrosurgical units are utilized in procedures such as coronary artery bypass grafting, valve repair, and atrial fibrillation surgery. In dental surgery, these units offer a high degree of precision for procedures involving soft and hard tissues. They are used for tasks such as tooth extraction, periodontal surgery, and implant placement, providing enhanced control and reducing the risk of damage to surrounding structures. In cosmetic surgery, ultrasonic electrosurgical units are employed to achieve precise tissue sculpting and coagulation, essential for procedures such as liposuction, facelifts, and rhinoplasty. The ability to minimize thermal damage and control bleeding contributes to improved aesthetic outcomes and faster patient recovery. The versatility and precision of ultrasonic electrosurgical units make them invaluable tools across these diverse surgical fields, enhancing the quality of care and patient outcomes.

Global Ultrasonic Electrosurgical Unit Market Outlook:

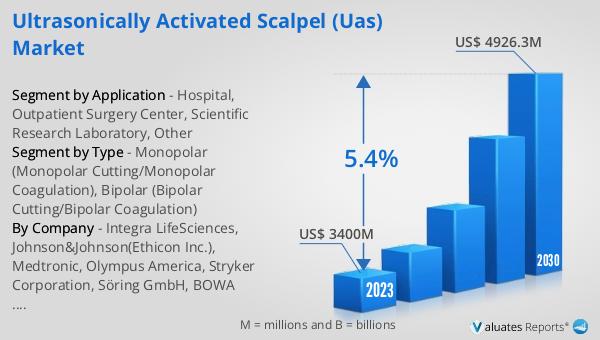

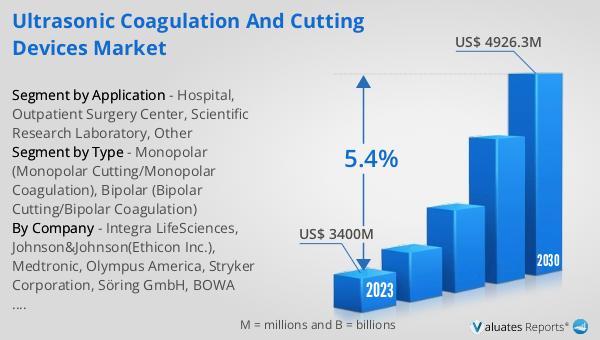

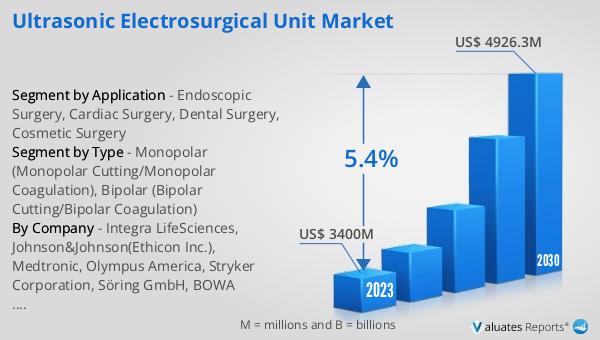

The global Ultrasonic Electrosurgical Unit market was valued at US$ 3400 million in 2023 and is anticipated to reach US$ 4926.3 million by 2030, witnessing a CAGR of 5.4% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced surgical technologies that offer precision, safety, and efficiency. The rising prevalence of chronic diseases, coupled with the growing aging population, is driving the need for more effective surgical solutions. Additionally, the trend towards minimally invasive surgeries is further propelling the adoption of ultrasonic electrosurgical units. These units provide surgeons with the ability to perform complex procedures with greater accuracy and control, reducing the risk of complications and improving patient outcomes. The market's expansion is also supported by continuous advancements in medical technology, leading to the development of more sophisticated and versatile ultrasonic electrosurgical units. As healthcare systems worldwide strive to enhance surgical care and patient safety, the demand for these advanced devices is expected to continue growing, making the global Ultrasonic Electrosurgical Unit market a critical component of the modern healthcare landscape.

| Report Metric | Details |

| Report Name | Ultrasonic Electrosurgical Unit Market |

| Accounted market size in 2023 | US$ 3400 million |

| Forecasted market size in 2030 | US$ 4926.3 million |

| CAGR | 5.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Integra LifeSciences, Johnson&Johnson(Ethicon Inc.), Medtronic, Olympus America, Stryker Corporation, Söring GmbH, BOWA MEDICAL, Bioventus(MISONIX,Inc.), Genesis MedTech(Reach Surgical), Apollo Technosystems, Ethicon Endo-Surgery, VDW GmbH, Advanced Instrumentations, MISONIX,Inc., B. Braun Holding GmbH&Co.KG, CONMED, Heritage Electromedicine GmbH, LED SpA, Cooper Medical,Inc., Miconvey, Lepu Medical Technology, Innolcon Medical Technology Co.,Ltd., Hocermed (Tianjin) Medical Technology Co.,Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |