What is Global Cloud-native Application Protection Platform Market?

The Global Cloud-native Application Protection Platform (CNAPP) market is a rapidly evolving sector that focuses on providing security solutions specifically designed for cloud-native applications. These platforms are built to protect applications that are developed and deployed using cloud-native technologies such as containers, microservices, and serverless architectures. CNAPPs offer a comprehensive suite of security features including vulnerability management, compliance monitoring, threat detection, and runtime protection. They are essential for organizations that are increasingly adopting cloud-native approaches to improve scalability, flexibility, and efficiency. The market for CNAPPs is driven by the growing need for robust security measures to protect sensitive data and ensure regulatory compliance in cloud environments. As more businesses transition to cloud-native architectures, the demand for advanced security solutions like CNAPPs is expected to rise significantly.

Public Cloud, Hybrid Cloud in the Global Cloud-native Application Protection Platform Market:

Public Cloud and Hybrid Cloud are two key deployment models in the Global Cloud-native Application Protection Platform (CNAPP) market. Public Cloud refers to cloud services offered by third-party providers over the internet, making them accessible to anyone who wishes to use or purchase them. These services are typically offered on a pay-per-use basis, which makes them cost-effective for businesses of all sizes. Public Cloud environments are highly scalable and flexible, allowing organizations to quickly adjust their resources based on demand. However, they also present unique security challenges, as data and applications are hosted on shared infrastructure. CNAPPs in Public Cloud environments focus on securing these shared resources, ensuring data privacy, and protecting against cyber threats. On the other hand, Hybrid Cloud is a combination of both public and private cloud environments, allowing data and applications to be shared between them. This model offers greater flexibility and more deployment options, enabling businesses to optimize their existing infrastructure while leveraging the benefits of the cloud. Hybrid Cloud environments are particularly beneficial for organizations that have specific regulatory or compliance requirements, as they can keep sensitive data on-premises while using the public cloud for less critical workloads. CNAPPs in Hybrid Cloud environments provide a unified security framework that spans both public and private clouds, ensuring consistent security policies and controls across all environments. They help organizations manage the complexities of hybrid deployments, offering visibility and control over their entire cloud infrastructure. Both Public and Hybrid Cloud models are integral to the CNAPP market, as they address different needs and challenges faced by organizations in their cloud adoption journey. As businesses continue to embrace cloud-native technologies, the role of CNAPPs in securing these environments becomes increasingly critical.

Large Enterprises, SMEs in the Global Cloud-native Application Protection Platform Market:

The usage of Global Cloud-native Application Protection Platform (CNAPP) in Large Enterprises and Small and Medium-sized Enterprises (SMEs) varies based on their unique needs and challenges. Large Enterprises often have complex IT infrastructures and a wide range of applications that require robust security measures. They typically operate in highly regulated industries such as finance, healthcare, and government, where data security and compliance are paramount. For these organizations, CNAPPs offer comprehensive security solutions that can protect their extensive cloud-native environments. These platforms provide advanced threat detection, vulnerability management, and compliance monitoring, ensuring that large enterprises can maintain a strong security posture while meeting regulatory requirements. Additionally, CNAPPs help large enterprises manage the scale and complexity of their cloud deployments, offering centralized visibility and control over their entire cloud infrastructure. On the other hand, SMEs often have limited resources and may not have dedicated security teams. They need cost-effective and easy-to-deploy security solutions that can protect their cloud-native applications without requiring extensive expertise. CNAPPs are particularly beneficial for SMEs as they offer automated security features that can detect and mitigate threats in real-time. These platforms provide SMEs with the tools they need to secure their cloud environments, ensuring data privacy and protection against cyber threats. Moreover, CNAPPs can help SMEs achieve compliance with industry standards and regulations, which is increasingly important as they grow and expand their operations. By leveraging CNAPPs, SMEs can focus on their core business activities while ensuring that their cloud-native applications are secure. Overall, the adoption of CNAPPs in both Large Enterprises and SMEs highlights the growing importance of cloud-native security solutions in today's digital landscape. As organizations of all sizes continue to migrate to the cloud, the demand for effective and scalable security platforms like CNAPPs is expected to increase.

Global Cloud-native Application Protection Platform Market Outlook:

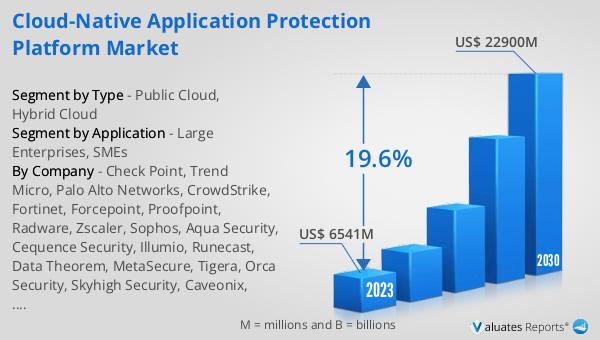

The global Cloud-native Application Protection Platform (CNAPP) market was valued at approximately $6.541 billion in 2023 and is projected to reach around $22.9 billion by 2030. This significant growth is expected to occur at a compound annual growth rate (CAGR) of 19.6% during the forecast period from 2024 to 2030. This impressive growth trajectory underscores the increasing importance of CNAPPs in the realm of cloud security. As businesses continue to adopt cloud-native technologies, the need for robust security solutions that can protect these environments becomes more critical. CNAPPs offer a comprehensive suite of security features designed to address the unique challenges of cloud-native applications, making them an essential component of modern IT infrastructure. The projected growth of the CNAPP market reflects the rising demand for these advanced security solutions, driven by the need to protect sensitive data, ensure regulatory compliance, and mitigate cyber threats in cloud environments.

| Report Metric | Details |

| Report Name | Cloud-native Application Protection Platform Market |

| Accounted market size in 2023 | US$ 6541 million |

| Forecasted market size in 2030 | US$ 22900 million |

| CAGR | 19.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Check Point, Trend Micro, Palo Alto Networks, CrowdStrike, Fortinet, Forcepoint, Proofpoint, Radware, Zscaler, Sophos, Aqua Security, Cequence Security, Illumio, Runecast, Data Theorem, MetaSecure, Tigera, Orca Security, Skyhigh Security, Caveonix, Ermetic, Banyan Cloud, AccuKnox |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |