What is Global Chemistry 4.0 Market?

The Global Chemistry 4.0 Market represents a transformative shift in the chemical industry, integrating advanced digital technologies to enhance efficiency, sustainability, and innovation. This market encompasses the adoption of Industry 4.0 principles, such as the Internet of Things (IoT), Artificial Intelligence (AI), and automation, to revolutionize chemical manufacturing and processes. By leveraging these technologies, companies can achieve real-time monitoring, predictive maintenance, and optimized production, leading to significant cost savings and reduced environmental impact. The Global Chemistry 4.0 Market is driven by the need for smarter, more agile operations that can respond quickly to changing market demands and regulatory requirements. This market is poised for substantial growth as industries worldwide recognize the benefits of digital transformation in the chemical sector.

IoT, AI, Automation, Other in the Global Chemistry 4.0 Market:

The integration of IoT, AI, and automation within the Global Chemistry 4.0 Market is reshaping the landscape of the chemical industry. IoT enables the interconnection of devices and systems, allowing for seamless data exchange and real-time monitoring of chemical processes. Sensors and smart devices collect vast amounts of data, which can be analyzed to optimize production, enhance safety, and reduce waste. AI plays a crucial role in processing this data, providing insights and predictive analytics that help in decision-making. Machine learning algorithms can identify patterns and anomalies, enabling predictive maintenance and reducing downtime. Automation, on the other hand, streamlines operations by automating repetitive tasks, improving precision, and increasing efficiency. Robotics and automated systems can handle hazardous materials, reducing the risk to human workers and ensuring consistent quality. These technologies collectively contribute to a more sustainable and efficient chemical industry. For instance, AI-driven models can predict equipment failures before they occur, allowing for timely maintenance and avoiding costly shutdowns. IoT-enabled devices can monitor environmental conditions and adjust processes in real-time to minimize energy consumption and emissions. Automation can also facilitate the development of new chemical formulations by rapidly testing and iterating different combinations. Beyond these core technologies, other advancements such as blockchain for supply chain transparency and digital twins for virtual simulations are also gaining traction in the Global Chemistry 4.0 Market. Blockchain can ensure the traceability of raw materials and finished products, enhancing trust and compliance with regulations. Digital twins, which are virtual replicas of physical assets, allow for simulation and optimization of processes before implementation, reducing risks and costs. The convergence of these technologies is driving the chemical industry towards a more connected, intelligent, and sustainable future. Companies that embrace Chemistry 4.0 are better positioned to innovate, reduce operational costs, and meet the growing demands for environmentally friendly products. As the market continues to evolve, the adoption of IoT, AI, automation, and other digital technologies will be pivotal in shaping the future of the chemical industry.

Medical, Agriculture, Transportation, Consumer Goods, Other in the Global Chemistry 4.0 Market:

The Global Chemistry 4.0 Market finds extensive applications across various sectors, including medical, agriculture, transportation, consumer goods, and others. In the medical field, Chemistry 4.0 technologies are revolutionizing drug discovery and development. AI and machine learning algorithms can analyze vast datasets to identify potential drug candidates, predict their efficacy, and optimize formulations. IoT devices enable real-time monitoring of pharmaceutical manufacturing processes, ensuring quality control and compliance with regulatory standards. Automation in laboratories accelerates research and development, allowing for faster and more accurate testing of new compounds. In agriculture, Chemistry 4.0 is enhancing crop protection and yield optimization. IoT sensors monitor soil conditions, weather patterns, and crop health, providing farmers with actionable insights to make informed decisions. AI-driven analytics can predict pest outbreaks and recommend targeted interventions, reducing the need for chemical pesticides and promoting sustainable farming practices. Automation in agricultural processes, such as precision spraying and automated harvesting, increases efficiency and reduces labor costs. The transportation sector benefits from Chemistry 4.0 through the development of advanced materials and fuels. AI and IoT technologies enable the creation of lightweight, durable materials that improve fuel efficiency and reduce emissions. Real-time monitoring of vehicle performance and predictive maintenance systems enhance safety and reliability. In the consumer goods industry, Chemistry 4.0 drives innovation in product development and manufacturing. AI algorithms analyze consumer preferences and market trends, guiding the creation of new products that meet evolving demands. IoT-enabled smart manufacturing processes ensure consistent quality and reduce waste. Automation in production lines increases throughput and lowers costs. Other sectors, such as energy and environmental management, also leverage Chemistry 4.0 technologies to achieve sustainability goals. AI and IoT solutions optimize energy consumption, reduce emissions, and enhance resource management. Automation in waste treatment and recycling processes improves efficiency and minimizes environmental impact. Overall, the Global Chemistry 4.0 Market is transforming industries by integrating digital technologies that enhance efficiency, sustainability, and innovation.

Global Chemistry 4.0 Market Outlook:

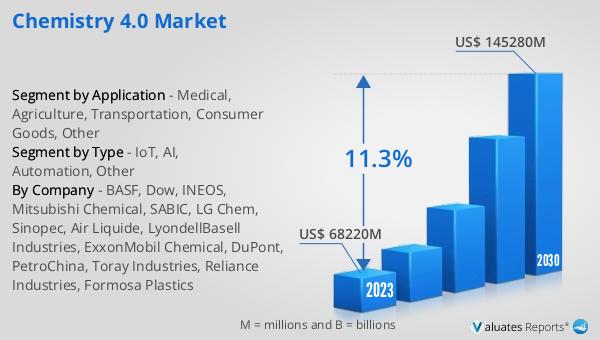

The global market for Chemistry 4.0 was valued at approximately US$ 68,220 million in 2023 and is projected to reach a revised size of US$ 145,280 million by 2030, with a compound annual growth rate (CAGR) of 11.3% during the forecast period from 2024 to 2030. The leading three companies in this market collectively hold a market share exceeding 5%. The Asia-Pacific region stands as the largest market, accounting for around 40% of the total market share. When it comes to product types, IoT emerges as the largest segment, representing about 25% of the market. In terms of applications, the transportation sector holds a significant share, also around 25%. This data underscores the rapid growth and widespread adoption of Chemistry 4.0 technologies across various regions and industries. The substantial market size and high growth rate highlight the increasing importance of digital transformation in the chemical industry. The dominance of the Asia-Pacific region indicates a strong demand for advanced chemical solutions in this area, driven by industrial growth and technological advancements. The significant share of IoT in product types reflects the critical role of interconnected devices and systems in optimizing chemical processes. Similarly, the notable share of the transportation sector in applications emphasizes the impact of Chemistry 4.0 on developing advanced materials and fuels, enhancing vehicle performance, and reducing environmental impact.

| Report Metric | Details |

| Report Name | Chemistry 4.0 Market |

| Forecasted market size in 2030 | US$ 145280 million |

| CAGR | 11.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | BASF, Dow, INEOS, Mitsubishi Chemical, SABIC, LG Chem, Sinopec, Air Liquide, LyondellBasell Industries, ExxonMobil Chemical, DuPont, PetroChina, Toray Industries, Reliance Industries, Formosa Plastics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |