What is Global Automatic Screen Printing Machine Market?

The Global Automatic Screen Printing Machine Market refers to the worldwide industry focused on the production, distribution, and utilization of machines designed for automatic screen printing. These machines are used to transfer ink onto various substrates through a mesh screen, except in areas made impermeable to the ink by a blocking stencil. The automation aspect of these machines enhances efficiency, consistency, and speed in the printing process, making them highly valuable in various industries. The market encompasses a wide range of machines, from small-scale units for specialized applications to large, industrial-grade machines capable of handling high-volume production. The demand for these machines is driven by their ability to produce high-quality prints with precision and repeatability, which is crucial for industries such as electronics, packaging, textiles, and advertising. As technology advances, these machines are becoming more sophisticated, offering features like multi-color printing, high-speed operation, and integration with digital systems for better control and monitoring. The global market is also influenced by factors such as economic conditions, technological advancements, and the growing need for efficient and cost-effective printing solutions.

Color Screen Printing, Monochromatic Screen Printing in the Global Automatic Screen Printing Machine Market:

Color screen printing and monochromatic screen printing are two primary methods utilized within the Global Automatic Screen Printing Machine Market. Color screen printing involves the use of multiple screens, each corresponding to a different color, to create vibrant, multi-colored images. This process is widely used in industries where visual appeal and detailed graphics are essential, such as in the production of promotional materials, apparel, and packaging. The precision of automatic screen printing machines ensures that each color layer aligns perfectly, resulting in high-quality prints with sharp details and consistent color reproduction. On the other hand, monochromatic screen printing uses a single color of ink to produce images or text. This method is often employed for simpler designs or where color is not a critical factor, such as in the printing of labels, technical diagrams, or single-color logos. Monochromatic printing is generally faster and more cost-effective than color printing, making it suitable for high-volume production runs. Both methods benefit from the automation provided by modern screen printing machines, which enhance productivity, reduce labor costs, and minimize errors. The choice between color and monochromatic screen printing depends on the specific requirements of the project, including the desired visual impact, budget, and production volume. As the Global Automatic Screen Printing Machine Market continues to evolve, advancements in technology are likely to further enhance the capabilities and efficiency of both color and monochromatic screen printing processes.

Electronics Industry, Packaging Industry, Crafts Printing, Print Ads, Spinning Industry, Other in the Global Automatic Screen Printing Machine Market:

The Global Automatic Screen Printing Machine Market finds extensive usage across various industries, each benefiting from the unique capabilities of these machines. In the electronics industry, automatic screen printing machines are used to print intricate circuit patterns on substrates like PCBs (Printed Circuit Boards). The precision and repeatability of these machines ensure that the electronic components function correctly, which is crucial for the reliability of electronic devices. In the packaging industry, these machines are employed to print high-quality graphics and information on packaging materials, enhancing the visual appeal and providing essential product details. This is particularly important for branding and marketing purposes. Crafts printing also leverages automatic screen printing machines to produce detailed and colorful designs on various materials, including textiles, ceramics, and paper. This allows artists and craftsmen to create unique, high-quality products efficiently. Print ads benefit from the ability of these machines to produce large volumes of posters, banners, and other promotional materials with consistent quality and vibrant colors. In the spinning industry, automatic screen printing machines are used to print patterns and designs on fabrics, contributing to the production of fashionable and appealing textiles. Other industries, such as automotive and medical, also utilize these machines for specialized printing applications, such as printing on automotive parts or medical devices. The versatility, efficiency, and precision of automatic screen printing machines make them indispensable tools across these diverse sectors, driving their demand and adoption in the global market.

Global Automatic Screen Printing Machine Market Outlook:

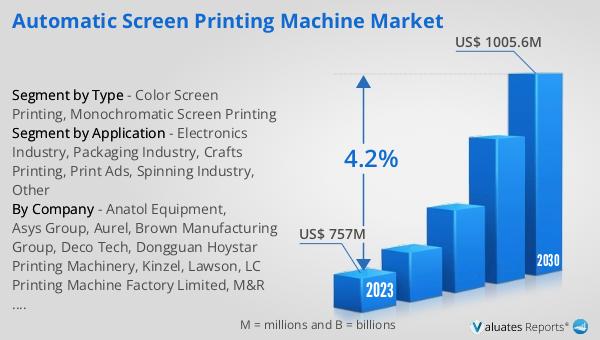

The global Automatic Screen Printing Machine market was valued at US$ 757 million in 2023 and is anticipated to reach US$ 1005.6 million by 2030, witnessing a CAGR of 4.2% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for efficient and high-quality printing solutions across various industries. The market's expansion is driven by technological advancements that enhance the capabilities of these machines, making them more versatile and user-friendly. Additionally, the growing need for automation in manufacturing processes to improve productivity and reduce labor costs is contributing to the market's positive outlook. As industries continue to seek innovative ways to enhance their production capabilities and meet consumer demands, the adoption of automatic screen printing machines is expected to rise, further fueling market growth.

| Report Metric | Details |

| Report Name | Automatic Screen Printing Machine Market |

| Accounted market size in 2023 | US$ 757 million |

| Forecasted market size in 2030 | US$ 1005.6 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Anatol Equipment, Asys Group, Aurel, Brown Manufacturing Group, Deco Tech, Dongguan Hoystar Printing Machinery, Kinzel, Lawson, LC Printing Machine Factory Limited, M&R Print, MACHINES DUBUIT, MHM, Mino Group, MOSS, OMSO, Sakurai, Shenzhen Quantong Screen Printing, Shijiazhuang Hongye, Siasprint Group, SPS Technoscreen, ST Drucksysteme, Systematic Automation, Tas, THIEME, Vastex, WINON INDUSTRIAL, Workhorse Products, Xinfeng Printing Machinery, Zhejiang Jinbao Machinery, Zhen Xing Screen Printing |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |