What is Global Whole Blood Coagulation Analyzer Market?

The Global Whole Blood Coagulation Analyzer Market is a specialized segment within the broader medical device industry, focusing on devices that measure the blood's ability to clot. These analyzers are crucial in diagnosing and managing various blood disorders, including hemophilia, deep vein thrombosis, and other clotting abnormalities. They are also essential in monitoring patients on anticoagulant therapy, ensuring that their blood remains within a therapeutic range to prevent either excessive bleeding or clotting. The market for these devices is driven by the increasing prevalence of blood-related disorders, advancements in medical technology, and the growing demand for point-of-care testing. Additionally, the aging global population and the rising number of surgical procedures contribute to the market's expansion. These analyzers come in various forms, including handheld, portable, and benchtop models, each catering to different healthcare settings and needs. The market is characterized by continuous innovation, with manufacturers striving to develop more accurate, faster, and user-friendly devices. Overall, the Global Whole Blood Coagulation Analyzer Market plays a vital role in modern healthcare, providing essential tools for the effective management of blood coagulation disorders.

Handheld, Portable, Benchtop in the Global Whole Blood Coagulation Analyzer Market:

Handheld, portable, and benchtop whole blood coagulation analyzers each serve unique roles within the Global Whole Blood Coagulation Analyzer Market, catering to different healthcare environments and requirements. Handheld analyzers are compact, easy-to-use devices designed for point-of-care testing. They are particularly useful in emergency settings, outpatient clinics, and home care scenarios where quick and accurate results are needed. These devices are battery-operated, making them highly portable and convenient for use in various locations. Despite their small size, handheld analyzers are equipped with advanced technology to provide reliable results, often within minutes. Portable analyzers, while slightly larger than handheld models, offer a balance between mobility and functionality. They are designed for use in settings that require frequent movement of equipment, such as ambulances, field hospitals, and smaller clinics. Portable analyzers typically come with rechargeable batteries and can be easily transported, making them ideal for situations where space and power supply are limited. They offer more features and capabilities than handheld devices, including the ability to run multiple tests simultaneously. Benchtop analyzers, on the other hand, are larger, stationary devices intended for use in laboratories and hospitals. These analyzers offer the highest level of functionality, accuracy, and throughput, making them suitable for high-volume testing environments. Benchtop models are equipped with advanced software and hardware, allowing for comprehensive analysis and data management. They can handle a wide range of tests, from basic coagulation profiles to more complex assays, and are often integrated with laboratory information systems for seamless data transfer and reporting. The choice between handheld, portable, and benchtop analyzers depends on various factors, including the specific needs of the healthcare setting, the volume of tests required, and the available resources. Each type of analyzer has its advantages and limitations, and healthcare providers must carefully consider these factors when selecting the appropriate device for their needs. Overall, the diversity of whole blood coagulation analyzers available in the market ensures that there is a suitable option for every healthcare scenario, from small clinics to large hospitals and research institutions.

Hospital, Clinic, Research Institute in the Global Whole Blood Coagulation Analyzer Market:

The usage of Global Whole Blood Coagulation Analyzers in hospitals, clinics, and research institutes highlights their versatility and importance in different healthcare settings. In hospitals, these analyzers are indispensable tools in various departments, including emergency rooms, operating theaters, and intensive care units. They are used to monitor patients undergoing surgery, those with trauma, and individuals with conditions that affect blood clotting. The ability to quickly and accurately assess coagulation status is critical in these settings, as it can significantly impact patient outcomes. Hospitals often rely on benchtop analyzers for their high throughput and comprehensive testing capabilities, ensuring that they can handle the large volume of tests required in such a busy environment. In clinics, whole blood coagulation analyzers are used for routine monitoring and diagnosis of patients with coagulation disorders. These settings often benefit from portable or handheld analyzers due to their ease of use and quick turnaround times. Clinics that manage patients on anticoagulant therapy, such as those with atrial fibrillation or deep vein thrombosis, use these devices to regularly check their patients' coagulation status and adjust medications as needed. The portability of these analyzers allows for point-of-care testing, which can improve patient compliance and satisfaction by providing immediate results and reducing the need for multiple visits. Research institutes utilize whole blood coagulation analyzers to advance the understanding of coagulation mechanisms and develop new treatments for coagulation disorders. These institutions often require high-precision and versatile analyzers capable of performing a wide range of tests. Benchtop analyzers are commonly used in research settings due to their advanced features and ability to handle complex assays. Researchers rely on these devices to conduct experiments, validate new diagnostic methods, and study the effects of various interventions on blood coagulation. The data generated from these studies contribute to the development of new therapies and improve clinical practices. Overall, the application of whole blood coagulation analyzers across hospitals, clinics, and research institutes underscores their critical role in modern healthcare. These devices not only aid in the diagnosis and management of coagulation disorders but also support ongoing research efforts to enhance our understanding and treatment of these conditions.

Global Whole Blood Coagulation Analyzer Market Outlook:

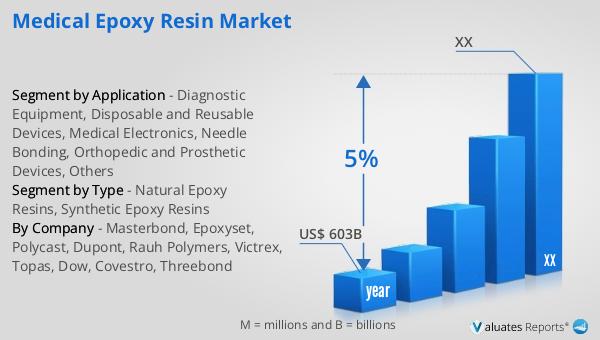

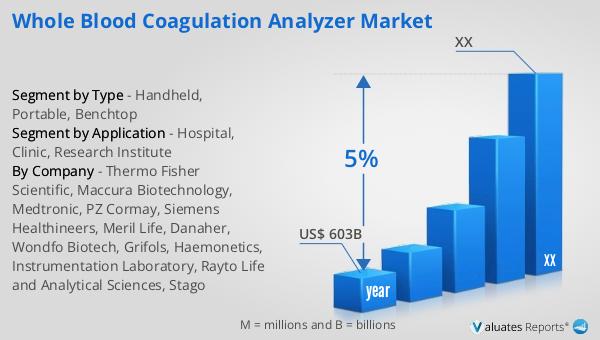

According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023, and will be growing at a CAGR of 5% during next six years. This data provides a comprehensive outlook on the future of the medical device industry, highlighting its significant growth potential. The market's estimated value of US$ 603 billion in 2023 underscores the substantial demand for medical devices worldwide. This demand is driven by various factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and the growing aging population. The projected compound annual growth rate (CAGR) of 5% over the next six years indicates a steady and robust expansion of the market. This growth rate reflects the continuous innovation and development within the industry, as well as the increasing adoption of medical devices in healthcare settings. The market outlook suggests that the medical device industry will continue to play a crucial role in improving patient outcomes and enhancing the quality of healthcare services globally. As the market evolves, it is expected to witness the introduction of new and advanced devices that cater to the diverse needs of patients and healthcare providers. Overall, the positive market outlook for medical devices highlights the industry's resilience and its critical contribution to the global healthcare landscape.

| Report Metric | Details |

| Report Name | Whole Blood Coagulation Analyzer Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Thermo Fisher Scientific, Maccura Biotechnology, Medtronic, PZ Cormay, Siemens Healthineers, Meril Life, Danaher, Wondfo Biotech, Grifols, Haemonetics, Instrumentation Laboratory, Rayto Life and Analytical Sciences, Stago |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |