What is Global Polyphenylene Sulfide Fibers Market?

The Global Polyphenylene Sulfide (PPS) Fibers Market is a specialized segment within the broader synthetic fibers industry. Polyphenylene sulfide fibers are known for their exceptional thermal and chemical resistance, making them ideal for high-performance applications. These fibers are used in various industries, including automotive, aerospace, electronics, and filtration, due to their ability to withstand harsh environments. The market for PPS fibers is driven by the increasing demand for durable and high-performance materials that can operate under extreme conditions. As industries continue to seek materials that offer longevity and reliability, the PPS fibers market is expected to grow. The market is characterized by a few key players who dominate the production and supply of these fibers, ensuring consistent quality and innovation. The demand for PPS fibers is also influenced by regulatory standards that require materials to meet specific performance criteria, further boosting their adoption across various sectors.

PPS Filaments, PPS Staple Fibers in the Global Polyphenylene Sulfide Fibers Market:

PPS filaments and PPS staple fibers are two primary forms of polyphenylene sulfide fibers used in the global market. PPS filaments are continuous fibers that are typically used in applications requiring high strength and durability. These filaments are often employed in the production of industrial fabrics, conveyor belts, and other materials that need to withstand high temperatures and corrosive environments. On the other hand, PPS staple fibers are short fibers that are spun into yarns and fabrics. These fibers are commonly used in filtration applications, such as bag filters, due to their excellent chemical resistance and thermal stability. PPS staple fibers are also used in the production of insulation materials, where their ability to resist heat and chemicals makes them ideal for use in harsh environments. Both PPS filaments and staple fibers offer unique advantages, making them suitable for a wide range of applications. The choice between filaments and staple fibers depends on the specific requirements of the application, such as the need for strength, durability, or flexibility. The versatility of PPS fibers, combined with their exceptional performance characteristics, makes them a valuable material in various industries.

Bag Filter, Insulation Materials, Others in the Global Polyphenylene Sulfide Fibers Market:

The usage of Global Polyphenylene Sulfide Fibers Market in bag filters, insulation materials, and other applications highlights the versatility and high-performance characteristics of these fibers. In bag filters, PPS fibers are used due to their excellent chemical resistance and thermal stability. These filters are commonly used in industrial settings where they need to withstand high temperatures and corrosive environments. The ability of PPS fibers to maintain their integrity under such conditions makes them ideal for use in bag filters, ensuring efficient filtration and long service life. In insulation materials, PPS fibers are valued for their thermal resistance and durability. These fibers are used in applications where insulation materials need to withstand high temperatures and harsh chemicals, such as in the automotive and aerospace industries. The use of PPS fibers in insulation materials helps improve the performance and longevity of these materials, making them more reliable and efficient. Other applications of PPS fibers include their use in protective clothing, gaskets, and seals, where their high-performance characteristics provide enhanced protection and durability. The versatility of PPS fibers, combined with their ability to perform under extreme conditions, makes them a valuable material in various high-performance applications.

Global Polyphenylene Sulfide Fibers Market Outlook:

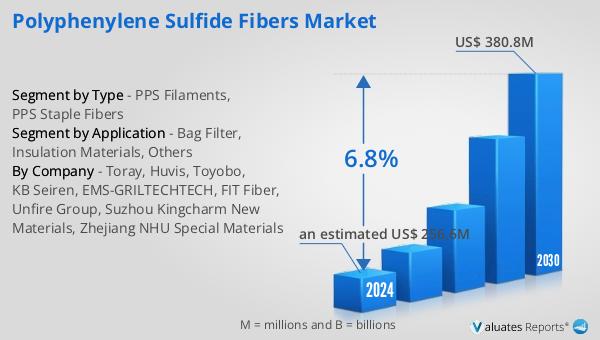

The global Polyphenylene Sulfide Fibers market is anticipated to grow significantly, reaching an estimated value of US$ 380.8 million by 2030, up from US$ 256.6 million in 2024, with a compound annual growth rate (CAGR) of 6.8% between 2024 and 2030. Key players in the global PPS fibers market include Toray, Huvis, Toyobo, KB Seiren, EMS-GRILTECH, FIT Fiber, Unfire Group, Suzhou Kingcharm New Materials, and Zhejiang NHU Special Materials, collectively accounting for about 48% of the market. Japan stands as the largest market, holding a share of over 39%. The most prevalent product in this market is PPS staple fibers, which dominate with a share exceeding 86%. The primary application for these fibers is in bag filters, which account for over 55% of the market. This market outlook underscores the significant role of PPS fibers in various high-performance applications and highlights the key players and regions driving the market's growth.

| Report Metric | Details |

| Report Name | Polyphenylene Sulfide Fibers Market |

| Accounted market size in 2024 | an estimated US$ 256.6 million |

| Forecasted market size in 2030 | US$ 380.8 million |

| CAGR | 6.8% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Toray, Huvis, Toyobo, KB Seiren, EMS-GRILTECHTECH, FIT Fiber, Unfire Group, Suzhou Kingcharm New Materials, Zhejiang NHU Special Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |