What is Global Actigraphy Sensors and Polysomnography Devices Market?

The global Actigraphy Sensors and Polysomnography Devices market is a specialized segment within the broader medical devices industry, focusing on tools used to monitor and diagnose sleep disorders. Actigraphy sensors are wearable devices that track movement and activity levels, providing valuable data on sleep patterns and circadian rhythms. Polysomnography devices, on the other hand, are more comprehensive and typically used in clinical settings to record various physiological parameters during sleep, such as brain waves, oxygen levels, heart rate, and eye movements. These devices are crucial for diagnosing conditions like sleep apnea, insomnia, and other sleep-related disorders. The market for these devices is driven by increasing awareness of sleep health, advancements in technology, and a growing prevalence of sleep disorders globally. The integration of these devices into homecare settings, hospitals, and diagnostic laboratories has expanded their accessibility and utility, making them indispensable tools in modern healthcare.

Actigraphy Devices, PSG Devices in the Global Actigraphy Sensors and Polysomnography Devices Market:

Actigraphy devices are compact, wearable gadgets that monitor and record physical activity and rest cycles over extended periods. They are typically worn on the wrist like a watch and use accelerometers to detect movement. The data collected by actigraphy devices is used to assess sleep patterns, circadian rhythms, and overall activity levels. These devices are particularly useful for diagnosing sleep disorders such as insomnia, circadian rhythm disorders, and restless legs syndrome. They offer a non-invasive, cost-effective alternative to more complex sleep studies, making them suitable for use in both clinical and home settings. Polysomnography (PSG) devices, on the other hand, are more sophisticated and are considered the gold standard for diagnosing sleep disorders. PSG involves an overnight sleep study conducted in a sleep lab or hospital, where multiple physiological parameters are recorded simultaneously. These parameters include brain activity (EEG), eye movements (EOG), muscle activity (EMG), heart rate (ECG), respiratory effort, airflow, and blood oxygen levels (SpO2). The comprehensive data collected by PSG devices allows for a detailed analysis of sleep architecture and the identification of various sleep disorders, including obstructive sleep apnea, central sleep apnea, periodic limb movement disorder, and narcolepsy. The global market for actigraphy sensors and polysomnography devices is driven by several factors, including the rising prevalence of sleep disorders, increasing awareness of the importance of sleep health, and advancements in technology. The integration of wireless and wearable technologies has made these devices more user-friendly and accessible, further boosting their adoption. Additionally, the growing trend of remote patient monitoring and telemedicine has expanded the use of these devices beyond traditional clinical settings. Major players in the market, such as Philips, Garmin, Fitbit, ResMed, Natus Medical, Nox Medical, SOMNOmedics, Compumedics, BMC Medical, Cleveland, Cidelec, and ActiGraph, are continuously innovating to enhance the functionality and accuracy of their products. These companies account for about 80% of the market share, indicating a highly competitive landscape. The Americas is the largest market for actigraphy sensors and polysomnography devices, with a share of over 59%. This can be attributed to the high prevalence of sleep disorders, advanced healthcare infrastructure, and increasing awareness of sleep health in the region. In conclusion, actigraphy devices and polysomnography devices play a crucial role in the diagnosis and management of sleep disorders. Their ability to provide valuable insights into sleep patterns and physiological parameters makes them indispensable tools in modern healthcare. As technology continues to advance, these devices are expected to become even more accurate, user-friendly, and accessible, further driving their adoption in various settings.

Homecare Settings, Hospitals, Diagnostic Laboratories, Others in the Global Actigraphy Sensors and Polysomnography Devices Market:

The usage of global actigraphy sensors and polysomnography devices spans across various settings, including homecare, hospitals, diagnostic laboratories, and other specialized environments. In homecare settings, actigraphy devices are particularly popular due to their ease of use and non-invasive nature. Patients can wear these devices in the comfort of their homes, allowing for continuous monitoring of sleep patterns and activity levels over extended periods. This is especially beneficial for individuals with chronic sleep disorders or those undergoing treatment for sleep-related issues. The data collected can be shared with healthcare providers for remote analysis, enabling timely interventions and personalized treatment plans. Polysomnography devices are also making their way into homecare settings, thanks to advancements in portable and wireless technology. Home-based PSG studies offer a convenient alternative to traditional sleep lab studies, reducing the need for hospital visits and making sleep diagnostics more accessible to a broader population. In hospitals, polysomnography devices are extensively used in sleep labs and specialized sleep centers. These devices provide comprehensive data on various physiological parameters, enabling accurate diagnosis and treatment of complex sleep disorders. Hospitals often have dedicated sleep specialists who interpret the data and develop tailored treatment plans for patients. Actigraphy devices are also used in hospital settings, particularly for monitoring patients with conditions that affect sleep, such as neurological disorders, psychiatric conditions, and chronic pain. The integration of these devices into hospital workflows enhances patient care by providing continuous, real-time data that can inform clinical decisions. Diagnostic laboratories play a crucial role in the global actigraphy sensors and polysomnography devices market. These labs are equipped with advanced PSG devices and staffed by trained technicians who conduct overnight sleep studies. The data collected is analyzed by sleep specialists to diagnose a wide range of sleep disorders. Actigraphy devices are also used in diagnostic labs for long-term monitoring of sleep patterns and circadian rhythms. The combination of actigraphy and PSG data provides a comprehensive view of a patient's sleep health, enabling accurate diagnosis and effective treatment. Other settings where these devices are used include research institutions, wellness centers, and corporate wellness programs. In research institutions, actigraphy and PSG devices are used to study sleep patterns, circadian rhythms, and the impact of various interventions on sleep health. Wellness centers and corporate wellness programs use these devices to promote healthy sleep habits and improve overall well-being. By monitoring sleep patterns and providing personalized feedback, these programs help individuals make informed decisions about their sleep health. In conclusion, the usage of global actigraphy sensors and polysomnography devices is widespread and diverse, spanning homecare settings, hospitals, diagnostic laboratories, and other specialized environments. These devices provide valuable insights into sleep patterns and physiological parameters, enabling accurate diagnosis and effective treatment of sleep disorders. As technology continues to advance, the adoption of these devices is expected to increase, further enhancing their role in modern healthcare.

Global Actigraphy Sensors and Polysomnography Devices Market Outlook:

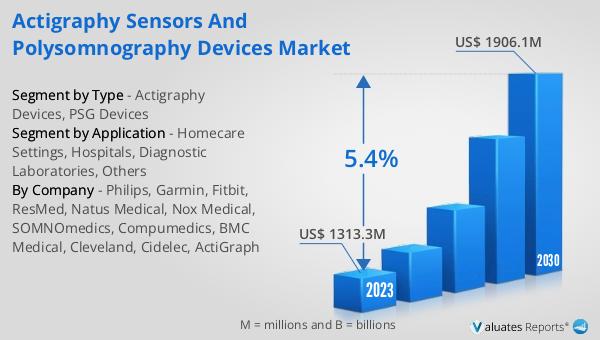

The global Actigraphy Sensors and Polysomnography Devices market is anticipated to grow significantly, reaching an estimated value of US$ 1906.1 million by 2030, up from US$ 1390.3 million in 2024. This growth is projected to occur at a compound annual growth rate (CAGR) of 5.4% between 2024 and 2030. The market is dominated by key players such as Philips, Garmin, Fitbit, ResMed, Natus Medical, Nox Medical, SOMNOmedics, Compumedics, BMC Medical, Cleveland, Cidelec, and ActiGraph, who collectively account for approximately 80% of the market share. The Americas hold the largest market share, exceeding 59%, which can be attributed to the high prevalence of sleep disorders, advanced healthcare infrastructure, and growing awareness of sleep health in the region. These companies are continuously innovating to enhance the functionality and accuracy of their products, making them more user-friendly and accessible. The integration of wireless and wearable technologies has further boosted the adoption of these devices, expanding their use beyond traditional clinical settings. The growing trend of remote patient monitoring and telemedicine has also contributed to the market's expansion, making sleep diagnostics more accessible to a broader population. In conclusion, the global Actigraphy Sensors and Polysomnography Devices market is poised for significant growth, driven by advancements in technology, increasing awareness of sleep health, and the rising prevalence of sleep disorders.

| Report Metric | Details |

| Report Name | Actigraphy Sensors and Polysomnography Devices Market |

| Accounted market size in 2024 | an estimated US$ 1390.3 million |

| Forecasted market size in 2030 | US$ 1906.1 million |

| CAGR | 5.4% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Philips, Garmin, Fitbit, ResMed, Natus Medical, Nox Medical, SOMNOmedics, Compumedics, BMC Medical, Cleveland, Cidelec, ActiGraph |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |