What is Global Air Brake System Market?

The Global Air Brake System Market refers to the worldwide industry focused on the production, distribution, and utilization of air brake systems. These systems are crucial for the safety and efficiency of heavy-duty vehicles such as trucks, trailers, and buses. Air brake systems use compressed air to activate the braking mechanism, providing a reliable and powerful means of stopping large vehicles. The market encompasses various components, including compressors, reservoirs, valves, and brake chambers, all working together to ensure optimal braking performance. The demand for air brake systems is driven by the increasing need for safety in commercial vehicles, stringent regulations, and the growth of the transportation and logistics sectors. Companies in this market are continuously innovating to improve the efficiency, reliability, and cost-effectiveness of their products. The market is also influenced by regional factors, such as the adoption of advanced braking technologies in developed countries and the growing automotive industry in emerging economies. Overall, the Global Air Brake System Market plays a vital role in enhancing vehicle safety and performance on a global scale.

Air Disc Brake, Air Drum Brake in the Global Air Brake System Market:

Air Disc Brakes and Air Drum Brakes are two primary types of braking systems used in the Global Air Brake System Market. Air Disc Brakes are known for their superior performance, especially in terms of stopping power and heat dissipation. They consist of a rotor, caliper, and brake pads, and work by using compressed air to press the brake pads against the rotor, creating friction that slows down the vehicle. This type of brake is highly efficient and provides consistent braking force, making it ideal for heavy-duty applications such as trucks and buses. Air Disc Brakes are also easier to maintain and have a longer lifespan compared to drum brakes, which contributes to their growing popularity in the market. On the other hand, Air Drum Brakes have been traditionally used in commercial vehicles due to their robust design and cost-effectiveness. They consist of a drum, brake shoes, and a wheel cylinder. When the brake pedal is pressed, compressed air forces the brake shoes against the drum, creating friction that slows down the vehicle. Although Air Drum Brakes are less expensive and simpler in design, they tend to have lower performance in terms of heat dissipation and stopping power compared to disc brakes. However, they are still widely used in many regions due to their durability and lower maintenance costs. The choice between Air Disc Brakes and Air Drum Brakes often depends on the specific requirements of the vehicle and the operating conditions. For instance, vehicles that require frequent and heavy braking, such as city buses and long-haul trucks, may benefit more from Air Disc Brakes due to their superior performance and reliability. In contrast, vehicles operating in less demanding conditions may opt for Air Drum Brakes to take advantage of their cost-effectiveness and simplicity. Both types of brakes play a crucial role in the Global Air Brake System Market, catering to different needs and preferences of vehicle manufacturers and operators. As technology advances, we can expect further improvements in both Air Disc and Air Drum Brakes, enhancing their performance, safety, and efficiency.

Heavy Trucks and Trailers, Buses, Others in the Global Air Brake System Market:

The Global Air Brake System Market finds extensive usage in various areas, including Heavy Trucks and Trailers, Buses, and other commercial vehicles. In Heavy Trucks and Trailers, air brake systems are essential for ensuring the safety and efficiency of these large and heavy vehicles. These vehicles often carry substantial loads and travel long distances, making reliable braking systems crucial. Air brakes provide the necessary stopping power and durability to handle the demands of heavy-duty applications. They also offer better heat dissipation and consistent performance, which are vital for maintaining safety on the road. In addition, air brake systems in heavy trucks and trailers are designed to meet stringent safety regulations, ensuring that these vehicles can operate safely under various conditions. Buses, another significant segment of the Global Air Brake System Market, also rely heavily on air brake systems. Buses, especially those used for public transportation, require reliable and efficient braking systems to ensure passenger safety. Air brakes provide the necessary stopping power and responsiveness needed for frequent stops and starts in urban environments. They also offer better control and stability, which are essential for maintaining safety in crowded and busy areas. Furthermore, air brake systems in buses are designed to be durable and low-maintenance, reducing downtime and operational costs for bus operators. Other commercial vehicles, such as delivery trucks, construction vehicles, and emergency vehicles, also benefit from the use of air brake systems. These vehicles often operate in demanding conditions and require reliable braking systems to ensure safety and efficiency. Air brakes provide the necessary performance and durability to handle the challenges of these applications. They also offer better control and stability, which are crucial for maintaining safety in various operating conditions. Overall, the Global Air Brake System Market plays a vital role in enhancing the safety and performance of commercial vehicles across different segments. The use of air brake systems in Heavy Trucks and Trailers, Buses, and other commercial vehicles ensures that these vehicles can operate safely and efficiently, meeting the demands of various applications and operating conditions.

Global Air Brake System Market Outlook:

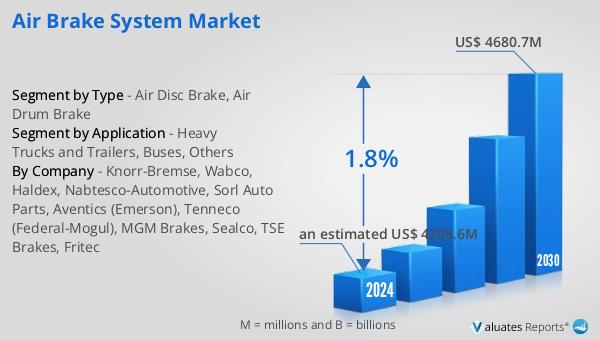

The global Air Brake System market is anticipated to grow from an estimated US$ 4205.6 million in 2024 to US$ 4680.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 1.8% during the forecast period from 2024 to 2030. Key players in the global air brake system market include Knorr-Bremse, Wabco, Haldex, Nabtesco Automotive, Sorl Auto Parts, Aventics, Emerson, Tenneco, Federal-Mogul, MGM Brakes, Sealco, TSE Brakes, and Fritec, collectively accounting for approximately 62% of the market share. The Asia-Pacific region holds the largest market share, exceeding 56%, indicating significant demand and growth potential in this area. Within the market, air disc brakes represent the largest segment, holding a share of over 79%, highlighting their widespread adoption and preference due to their superior performance and reliability. The heavy trucks and trailers segment is the largest application area, accounting for over 63% of the market share, underscoring the critical role of air brake systems in ensuring the safety and efficiency of these heavy-duty vehicles.

| Report Metric | Details |

| Report Name | Air Brake System Market |

| Accounted market size in 2024 | an estimated US$ 4205.6 million |

| Forecasted market size in 2030 | US$ 4680.7 million |

| CAGR | 1.8% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Knorr-Bremse, Wabco, Haldex, Nabtesco-Automotive, Sorl Auto Parts, Aventics (Emerson), Tenneco (Federal-Mogul), MGM Brakes, Sealco, TSE Brakes, Fritec |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |