What is Global Infrared Lens (IR Lens) Market?

The Global Infrared Lens (IR Lens) Market is a rapidly growing sector within the optics and photonics industry. Infrared lenses are specialized optical components designed to focus infrared light, which is invisible to the human eye but can be detected by electronic sensors. These lenses are crucial in various applications, including thermal imaging, night vision, and spectroscopy. The market for IR lenses is driven by advancements in technology, increasing demand for security and surveillance systems, and the growing adoption of infrared technology in automotive and medical fields. The global market encompasses a wide range of products, from simple lenses to complex assemblies, catering to diverse industries such as military and defense, healthcare, automotive, and industrial automation. As the demand for high-quality, reliable infrared lenses continues to rise, manufacturers are focusing on innovation and improving the performance of their products to meet the evolving needs of their customers.

Prime Infrared Lens, Zoom Infrared Lens in the Global Infrared Lens (IR Lens) Market:

Prime Infrared Lenses and Zoom Infrared Lenses are two primary categories within the Global Infrared Lens (IR Lens) Market, each serving distinct purposes and applications. Prime infrared lenses have a fixed focal length, meaning they cannot zoom in or out. These lenses are known for their simplicity, durability, and superior image quality. They are often used in applications where a specific field of view is required, such as in thermal imaging cameras for industrial inspections or medical diagnostics. Prime lenses are favored for their ability to provide sharp, high-contrast images, making them ideal for detailed analysis and precise measurements. On the other hand, Zoom Infrared Lenses offer variable focal lengths, allowing users to adjust the magnification and field of view. This flexibility makes zoom lenses suitable for dynamic environments where the distance to the target may change, such as in security and surveillance systems or military operations. Zoom lenses are equipped with complex optical designs and advanced materials to maintain image quality across different magnifications. They are particularly useful in applications that require continuous monitoring and the ability to quickly adapt to varying conditions. Both prime and zoom infrared lenses are integral to the IR lens market, addressing the diverse needs of various industries. Manufacturers are continually innovating to enhance the performance, durability, and affordability of these lenses, ensuring they meet the stringent requirements of their respective applications.

Military & Defense, Security System, Automotive, Medical, Industry and Public Safety in the Global Infrared Lens (IR Lens) Market:

The usage of Global Infrared Lens (IR Lens) Market spans several critical areas, including Military & Defense, Security Systems, Automotive, Medical, Industry, and Public Safety. In the Military & Defense sector, IR lenses are essential for night vision equipment, thermal imaging devices, and missile guidance systems. These lenses enable soldiers to see in complete darkness, detect heat signatures, and accurately target enemies, thereby enhancing operational effectiveness and safety. In Security Systems, IR lenses are used in surveillance cameras to monitor premises in low-light or no-light conditions. They help in detecting intruders, identifying suspicious activities, and ensuring the safety of people and property. The Automotive industry leverages IR lenses in advanced driver-assistance systems (ADAS) and autonomous vehicles. These lenses are used in night vision systems to detect pedestrians, animals, and obstacles on the road, thereby preventing accidents and improving road safety. In the Medical field, IR lenses are utilized in diagnostic equipment such as thermal imaging cameras to detect abnormalities in body temperature, which can indicate various health conditions. They are also used in non-invasive medical procedures, providing a safer alternative to traditional methods. The Industrial sector employs IR lenses in machinery and equipment for monitoring and maintenance purposes. They help in detecting overheating components, ensuring the smooth operation of machines, and preventing potential failures. Lastly, in Public Safety, IR lenses are used by firefighters to see through smoke and locate individuals trapped in burning buildings. They are also used in search and rescue operations to find missing persons in challenging environments. The versatility and effectiveness of IR lenses make them indispensable across these diverse applications, driving their demand in the global market.

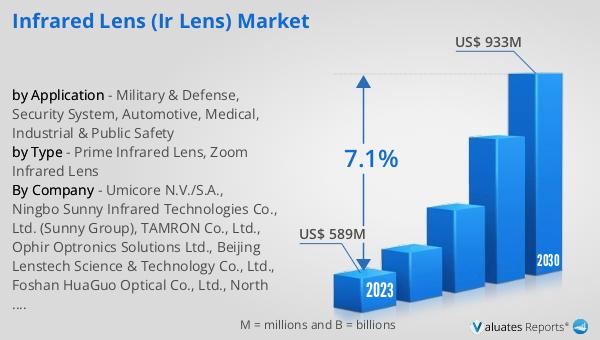

Global Infrared Lens (IR Lens) Market Outlook:

The global Infrared Lens (IR Lens) market is anticipated to grow significantly in the coming years. By 2030, the market is expected to reach a valuation of approximately US$ 938 million, up from an estimated US$ 571.8 million in 2024. This growth represents a compound annual growth rate (CAGR) of 8.6% during the forecast period from 2024 to 2030. This robust growth can be attributed to several factors, including the increasing adoption of infrared technology across various industries, advancements in IR lens manufacturing, and the rising demand for high-quality imaging solutions. As industries continue to recognize the benefits of infrared lenses in enhancing safety, security, and operational efficiency, the market is poised for substantial expansion. Manufacturers are likely to focus on innovation and the development of cost-effective solutions to cater to the growing demand, ensuring that the market remains dynamic and competitive.

| Report Metric | Details |

| Report Name | Infrared Lens (IR Lens) Market |

| Accounted market size in 2024 | an estimated US$ 571.8 million |

| Forecasted market size in 2030 | US$ 938 million |

| CAGR | 8.6% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Umicore, Ophir Optronics Solutions Ltd., TAMRON, Beijing Lenstech Science & Technology Co., Ltd., Northern Night Vision Technology Research Institute Group Co., Ltd., Kunming Full-wave Infrared Technology Co., Ltd., LightPath Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |