What is Global Maintenance Hemodialysis Catheter Market?

The Global Maintenance Hemodialysis Catheter Market refers to the worldwide industry focused on the production, distribution, and utilization of hemodialysis catheters used for long-term and short-term dialysis treatments. Hemodialysis catheters are essential medical devices that facilitate the removal of waste products and excess fluids from the blood when the kidneys are no longer able to perform these functions effectively. This market encompasses a wide range of products, including different types of catheters designed for various durations of use, as well as the associated maintenance and replacement services. The market is driven by the increasing prevalence of chronic kidney diseases, advancements in medical technology, and the growing demand for efficient and reliable dialysis treatments. Companies operating in this market are continuously innovating to improve the safety, efficacy, and patient comfort associated with hemodialysis catheters. The global reach of this market ensures that patients across different regions have access to life-saving dialysis treatments, thereby improving their quality of life and overall health outcomes.

Long-Term Hemodialysis Catheters, Short-Term Hemodialysis Catheters in the Global Maintenance Hemodialysis Catheter Market:

Long-term hemodialysis catheters and short-term hemodialysis catheters are two primary categories within the Global Maintenance Hemodialysis Catheter Market, each serving distinct purposes based on the duration and frequency of dialysis treatments required by patients. Long-term hemodialysis catheters, also known as tunneled catheters, are designed for patients who need dialysis over an extended period, typically several months to years. These catheters are surgically implanted under the skin and tunneled to a central vein, providing a stable and reliable access point for repeated dialysis sessions. The design of long-term catheters prioritizes durability and patient comfort, with features such as antimicrobial coatings to reduce the risk of infection and materials that minimize irritation and clotting. On the other hand, short-term hemodialysis catheters, also known as non-tunneled catheters, are intended for temporary use, usually for a few weeks to a few months. These catheters are inserted directly into a central vein, often in emergency situations or when immediate dialysis is required. Short-term catheters are typically easier to insert and remove, making them suitable for acute kidney injury or while waiting for a more permanent dialysis access solution, such as an arteriovenous fistula or graft. Both types of catheters play a crucial role in the management of kidney failure, ensuring that patients receive timely and effective dialysis treatments. The choice between long-term and short-term catheters depends on various factors, including the patient's overall health, the severity of kidney disease, and the anticipated duration of dialysis. The Global Maintenance Hemodialysis Catheter Market is characterized by continuous innovation and improvement in catheter design, materials, and insertion techniques, aimed at enhancing patient outcomes and reducing complications. Companies in this market invest heavily in research and development to create catheters that offer better biocompatibility, lower infection rates, and improved ease of use for healthcare providers. Additionally, the market includes a range of maintenance services, such as regular catheter flushing, monitoring for signs of infection or malfunction, and timely replacement when necessary. These services are essential to ensure the longevity and effectiveness of hemodialysis catheters, ultimately contributing to better patient care and quality of life.

Hospital, Clinic, Medical Research Center in the Global Maintenance Hemodialysis Catheter Market:

The usage of Global Maintenance Hemodialysis Catheter Market products spans various healthcare settings, including hospitals, clinics, and medical research centers, each with specific needs and applications. In hospitals, hemodialysis catheters are commonly used in nephrology departments and intensive care units (ICUs) to provide immediate and life-saving dialysis treatments for patients with acute kidney injury or chronic kidney disease. Hospitals often handle complex cases that require advanced catheter technologies and skilled medical professionals to manage the insertion, maintenance, and monitoring of these devices. The availability of a wide range of hemodialysis catheters in hospitals ensures that patients receive the most appropriate and effective treatment based on their individual medical conditions. Clinics, on the other hand, typically cater to patients with chronic kidney disease who require regular and ongoing dialysis treatments. These outpatient facilities rely on long-term hemodialysis catheters to provide stable and reliable access for repeated dialysis sessions. Clinics focus on maintaining the functionality and safety of these catheters through regular monitoring, cleaning, and replacement when necessary. The use of hemodialysis catheters in clinics is essential for managing the long-term health and well-being of patients, allowing them to receive consistent and high-quality care. Medical research centers play a crucial role in advancing the Global Maintenance Hemodialysis Catheter Market by conducting studies and trials to evaluate new catheter designs, materials, and technologies. These centers collaborate with manufacturers, healthcare providers, and regulatory bodies to develop innovative solutions that address the challenges associated with hemodialysis catheters, such as infection risk, clotting, and patient discomfort. Research centers also contribute to the development of best practices and guidelines for the safe and effective use of hemodialysis catheters, ultimately improving patient outcomes and advancing the field of nephrology. The integration of hemodialysis catheters in these diverse healthcare settings highlights the importance of a comprehensive and collaborative approach to managing kidney disease. By leveraging the expertise and resources of hospitals, clinics, and medical research centers, the Global Maintenance Hemodialysis Catheter Market continues to evolve and improve, ensuring that patients receive the best possible care and treatment.

Global Maintenance Hemodialysis Catheter Market Outlook:

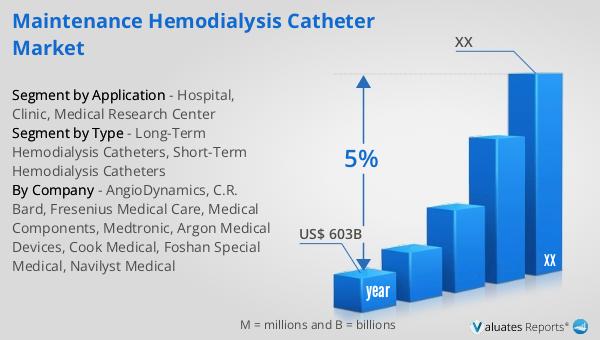

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This substantial market size underscores the critical role that medical devices play in modern healthcare, encompassing a wide range of products from diagnostic tools to therapeutic equipment. The steady growth rate reflects ongoing advancements in medical technology, increasing healthcare expenditures, and the rising prevalence of chronic diseases that necessitate the use of sophisticated medical devices. Companies operating in this market are continually innovating to meet the evolving needs of healthcare providers and patients, driving improvements in device performance, safety, and accessibility. The global reach of the medical device market ensures that innovations and advancements are disseminated across different regions, contributing to improved health outcomes worldwide. As the market continues to expand, it presents significant opportunities for stakeholders, including manufacturers, healthcare providers, and investors, to contribute to the development and distribution of cutting-edge medical technologies that enhance patient care and quality of life.

| Report Metric | Details |

| Report Name | Maintenance Hemodialysis Catheter Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | AngioDynamics, C.R. Bard, Fresenius Medical Care, Medical Components, Medtronic, Argon Medical Devices, Cook Medical, Foshan Special Medical, Navilyst Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |