What is Global Automated Food Robot Market?

The Global Automated Food Robot Market refers to the industry focused on the development, production, and deployment of robots specifically designed for food-related tasks. These robots are utilized in various stages of food production, processing, packaging, and distribution. The market encompasses a wide range of robotic technologies, including articulated robots, parallel robots, and collaborative robots, each tailored to perform specific functions within the food industry. The primary goal of these automated systems is to enhance efficiency, accuracy, and hygiene in food handling processes, thereby reducing human error and contamination risks. As the demand for automation in the food sector grows, driven by factors such as labor shortages, increasing production demands, and stringent food safety regulations, the Global Automated Food Robot Market is expected to expand significantly. These robots are not only transforming traditional food manufacturing practices but also paving the way for innovative solutions in food retail and logistics, ultimately contributing to a more streamlined and safe food supply chain.

Articulated Type, Parallel Type, Collaborative Type in the Global Automated Food Robot Market:

In the Global Automated Food Robot Market, there are several types of robots that play crucial roles in various food-related applications. Articulated robots, for instance, are highly versatile and are characterized by their rotary joints, which allow for a wide range of movements. These robots are commonly used in tasks such as picking and placing items, packaging, and palletizing. Their flexibility and precision make them ideal for handling delicate food products without causing damage. Parallel robots, also known as delta robots, are another type of automated food robot. These robots are known for their high-speed capabilities and are often used in applications that require rapid and repetitive movements, such as sorting and assembling food items. Their unique design, which includes multiple arms connected to a common base, allows them to perform tasks with exceptional speed and accuracy. Collaborative robots, or cobots, are designed to work alongside human workers in a shared workspace. These robots are equipped with advanced sensors and safety features that enable them to operate safely in close proximity to humans. In the food industry, cobots are used for tasks such as assisting in food preparation, packaging, and quality control. Their ability to work collaboratively with humans helps to enhance productivity and reduce the physical strain on workers. Each type of robot in the Global Automated Food Robot Market offers distinct advantages, and their deployment is often determined by the specific needs and requirements of the food processing and handling tasks at hand.

Food Factory, Supermarket, Logistics Company in the Global Automated Food Robot Market:

The usage of automated food robots in various sectors such as food factories, supermarkets, and logistics companies is transforming the way food is processed, handled, and distributed. In food factories, automated robots are employed to perform a wide range of tasks, from ingredient mixing and cooking to packaging and labeling. These robots help to streamline production processes, ensuring consistent quality and reducing the risk of contamination. For example, articulated robots can be used to handle raw ingredients with precision, while parallel robots can quickly sort and package finished products. In supermarkets, automated food robots are revolutionizing the way food is stocked and managed. Robots equipped with advanced sensors and AI capabilities can monitor inventory levels, restock shelves, and even assist customers in finding products. This not only enhances the shopping experience but also ensures that shelves are always stocked with fresh products. Additionally, collaborative robots can work alongside supermarket staff to perform tasks such as cleaning and organizing shelves, allowing human workers to focus on more customer-centric activities. In logistics companies, automated food robots play a crucial role in the efficient transportation and distribution of food products. These robots can be used to sort and load packages, ensuring that food items are handled with care and delivered promptly. For instance, parallel robots can quickly sort packages based on their destination, while articulated robots can load and unload trucks with precision. The use of automated food robots in logistics helps to reduce the risk of damage to food products during transit and ensures timely delivery to retailers and consumers. Overall, the integration of automated food robots in food factories, supermarkets, and logistics companies is driving significant improvements in efficiency, accuracy, and safety across the food supply chain.

Global Automated Food Robot Market Outlook:

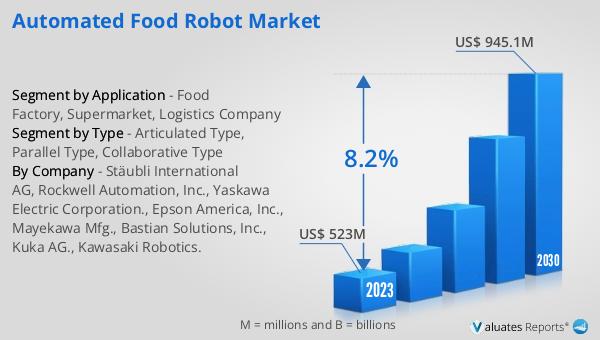

The global Automated Food Robot market was valued at US$ 523 million in 2023 and is anticipated to reach US$ 945.1 million by 2030, witnessing a CAGR of 8.2% during the forecast period from 2024 to 2030. This substantial growth reflects the increasing adoption of automation technologies in the food industry, driven by the need for enhanced efficiency, accuracy, and hygiene in food handling processes. The market's expansion is also fueled by factors such as labor shortages, rising production demands, and stringent food safety regulations. As food manufacturers, retailers, and logistics companies continue to seek innovative solutions to streamline their operations and meet consumer expectations, the demand for automated food robots is expected to rise significantly. These robots are not only transforming traditional food manufacturing practices but also paving the way for new applications in food retail and logistics, ultimately contributing to a more efficient and safe food supply chain. The projected growth of the global Automated Food Robot market underscores the critical role that automation will play in shaping the future of the food industry.

| Report Metric | Details |

| Report Name | Automated Food Robot Market |

| Accounted market size in 2023 | US$ 523 million |

| Forecasted market size in 2030 | US$ 945.1 million |

| CAGR | 8.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Stäubli International AG, Rockwell Automation, Inc., Yaskawa Electric Corporation., Epson America, Inc., Mayekawa Mfg., Bastian Solutions, Inc., Kuka AG., Kawasaki Robotics. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |