What is Global EV Connectors Market?

The Global EV Connectors Market refers to the worldwide industry focused on the production and distribution of connectors used in electric vehicles (EVs). These connectors are essential components that facilitate the transfer of electricity from charging stations to the vehicle's battery. As the demand for electric vehicles continues to rise due to environmental concerns and government regulations promoting cleaner energy, the market for EV connectors is also expanding. These connectors come in various types and standards, designed to meet different charging speeds and compatibility requirements. The market encompasses a wide range of products, including slow, fast, and rapid connectors, each catering to specific needs and preferences of EV users. The growth of this market is driven by advancements in technology, increasing investments in EV infrastructure, and the growing adoption of electric vehicles globally. As a result, the Global EV Connectors Market is becoming a crucial segment within the broader automotive and energy sectors, playing a significant role in the transition towards sustainable transportation.

Slow Connectors, Fast Connectors, Rapid Connectors in the Global EV Connectors Market:

In the Global EV Connectors Market, connectors are categorized based on their charging speeds: slow connectors, fast connectors, and rapid connectors. Slow connectors are typically used for overnight charging at home or in workplaces where vehicles can be left to charge for extended periods. These connectors usually provide a lower power output, making them suitable for situations where charging speed is not a critical factor. Fast connectors, on the other hand, offer a higher power output and are commonly found in public charging stations. They are designed to charge an EV in a few hours, making them ideal for urban areas where drivers need a quicker turnaround. Rapid connectors are the fastest among the three, capable of charging an EV to 80% in as little as 30 minutes. These connectors are often used in highway rest stops and other locations where drivers need to recharge quickly during long trips. Each type of connector has its own set of standards and specifications, ensuring compatibility with different EV models and charging infrastructures. The choice of connector depends on various factors, including the vehicle's battery capacity, the availability of charging stations, and the user's charging habits. As the EV market continues to grow, the demand for all three types of connectors is expected to increase, driven by the need for more versatile and efficient charging solutions.

Battery Electric Vehicles (BEVs), Plug-In Hybrid Electric Vehicles (PHEVs), Others in the Global EV Connectors Market:

The usage of Global EV Connectors Market extends to various types of electric vehicles, including Battery Electric Vehicles (BEVs), Plug-In Hybrid Electric Vehicles (PHEVs), and others. BEVs rely entirely on electric power and require efficient and reliable connectors for charging. These vehicles benefit from all types of connectors, with slow connectors being ideal for home charging, fast connectors for urban charging stations, and rapid connectors for long-distance travel. PHEVs, which combine an internal combustion engine with an electric motor, also utilize EV connectors for charging their batteries. While PHEVs can switch to gasoline when the battery is depleted, having access to fast and rapid connectors can enhance their electric range and reduce reliance on fossil fuels. Other types of electric vehicles, such as electric buses, trucks, and motorcycles, also depend on EV connectors for their charging needs. These vehicles often require specialized connectors to handle higher power outputs and ensure safe and efficient charging. The versatility of EV connectors makes them a critical component in the broader adoption of electric vehicles across different segments. As more countries and cities invest in EV infrastructure, the availability and accessibility of various types of connectors will play a key role in supporting the transition to electric mobility.

Global EV Connectors Market Outlook:

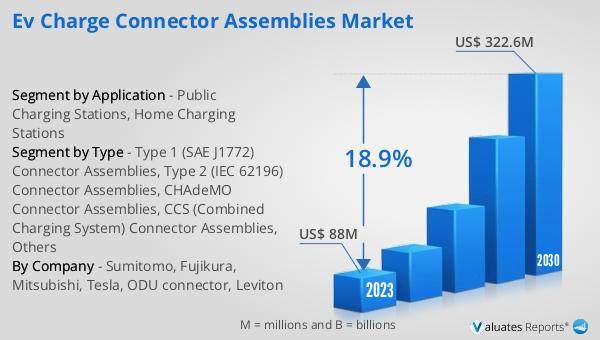

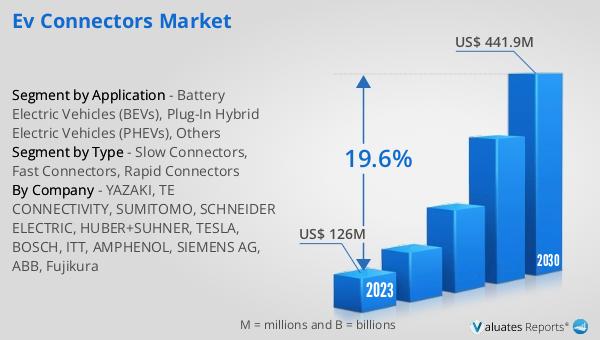

The global EV Connectors market, valued at US$ 126 million in 2023, is projected to grow significantly, reaching US$ 441.9 million by 2030. This growth represents a compound annual growth rate (CAGR) of 19.6% during the forecast period from 2024 to 2030. The increasing adoption of electric vehicles, driven by environmental concerns and supportive government policies, is a major factor contributing to this market expansion. As more consumers and businesses shift towards electric mobility, the demand for reliable and efficient EV connectors is expected to rise. This growth trajectory highlights the importance of continued investment in EV infrastructure and technological advancements to meet the evolving needs of the market. The projected increase in market value underscores the critical role of EV connectors in the broader transition to sustainable transportation.

| Report Metric | Details |

| Report Name | EV Connectors Market |

| Accounted market size in 2023 | US$ 126 million |

| Forecasted market size in 2030 | US$ 441.9 million |

| CAGR | 19.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | YAZAKI, TE CONNECTIVITY, SUMITOMO, SCHNEIDER ELECTRIC, HUBER+SUHNER, TESLA, BOSCH, ITT, AMPHENOL, SIEMENS AG, ABB, Fujikura |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |