What is Global Soy-Based Surfactants Market?

The Global Soy-Based Surfactants Market refers to the worldwide industry focused on the production and distribution of surfactants derived from soybeans. Surfactants are compounds that lower the surface tension between two substances, such as a liquid and a solid, and are commonly used in detergents, emulsifiers, and foaming agents. Soy-based surfactants are eco-friendly alternatives to traditional petroleum-based surfactants, offering biodegradability and reduced environmental impact. These surfactants are derived from various soy components, including soy lecithin, soy fatty acid esters, and soy ether amines. The market for soy-based surfactants is driven by increasing consumer awareness of sustainable products, stringent environmental regulations, and the growing demand for natural and organic personal care products. As industries seek greener alternatives, the adoption of soy-based surfactants is expected to rise, contributing to the market's growth. The market encompasses various applications, including household detergents, agricultural chemicals, and other industrial uses, highlighting the versatility and importance of soy-based surfactants in promoting sustainability across different sectors.

Soy Lecithin, Soy Fatty Acid Esters, Soy Ether Amines, Others in the Global Soy-Based Surfactants Market:

Soy lecithin, soy fatty acid esters, soy ether amines, and other soy-based surfactants play crucial roles in the Global Soy-Based Surfactants Market. Soy lecithin is a natural emulsifier derived from soybean oil, widely used in food, pharmaceuticals, and cosmetics. It helps blend ingredients that typically do not mix well, such as oil and water, enhancing the texture and stability of products. In the food industry, soy lecithin is used in chocolates, baked goods, and margarine to improve consistency and shelf life. In cosmetics, it acts as a moisturizer and stabilizer in creams and lotions. Soy fatty acid esters are another important category, formed by reacting fatty acids from soybeans with alcohols. These esters are used in personal care products, lubricants, and as emulsifiers in various industrial applications. They offer excellent biodegradability and are preferred for their non-toxic nature. Soy ether amines, derived from soybean oil, are used as surfactants in agricultural chemicals, detergents, and personal care products. They help in the formulation of herbicides and pesticides, enhancing their effectiveness and reducing environmental impact. Other soy-based surfactants include soy protein-based surfactants and soy saponins, which find applications in niche markets. Soy protein-based surfactants are used in personal care products for their mildness and conditioning properties, while soy saponins are used in pharmaceuticals and cosmetics for their foaming and emulsifying abilities. The versatility of these soy-based surfactants makes them valuable in various industries, promoting sustainability and reducing reliance on petroleum-based alternatives. As the demand for eco-friendly products continues to rise, the adoption of soy-based surfactants is expected to grow, driving innovation and development in the market.

Household Detergents, Agricultural Chemicals, Others in the Global Soy-Based Surfactants Market:

The Global Soy-Based Surfactants Market finds extensive usage in household detergents, agricultural chemicals, and other applications. In household detergents, soy-based surfactants are used as cleaning agents due to their excellent emulsifying and foaming properties. They help in breaking down and removing dirt, grease, and stains from fabrics and surfaces, making them effective in laundry detergents, dishwashing liquids, and all-purpose cleaners. The biodegradability of soy-based surfactants makes them an eco-friendly choice, reducing the environmental impact of household cleaning products. In agricultural chemicals, soy-based surfactants are used as adjuvants in herbicides, pesticides, and fungicides. They enhance the efficacy of these chemicals by improving their spreadability, adhesion, and penetration on plant surfaces. This results in better pest and weed control, leading to higher crop yields and reduced chemical usage. The use of soy-based surfactants in agriculture also promotes sustainable farming practices by minimizing the environmental impact of chemical applications. Other applications of soy-based surfactants include their use in personal care products, industrial cleaners, and oilfield chemicals. In personal care products, soy-based surfactants are used in shampoos, conditioners, and body washes for their mildness and conditioning properties. They help in creating rich lathers and improving the texture of formulations. In industrial cleaners, soy-based surfactants are used for their degreasing and emulsifying abilities, making them effective in removing heavy oils and greases from machinery and equipment. In oilfield chemicals, soy-based surfactants are used in drilling fluids and enhanced oil recovery processes to improve the efficiency of oil extraction. The versatility and eco-friendly nature of soy-based surfactants make them valuable in various applications, driving their demand in the market.

Global Soy-Based Surfactants Market Outlook:

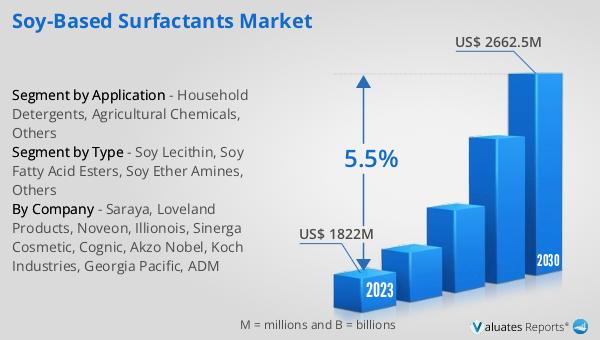

The global Soy-Based Surfactants market was valued at US$ 1822 million in 2023 and is anticipated to reach US$ 2662.5 million by 2030, witnessing a CAGR of 5.5% during the forecast period 2024-2030. This significant growth reflects the increasing demand for eco-friendly and sustainable surfactants across various industries. The market's expansion is driven by factors such as rising consumer awareness of environmental issues, stringent regulations on the use of petroleum-based surfactants, and the growing preference for natural and organic products. As industries continue to seek greener alternatives, the adoption of soy-based surfactants is expected to rise, contributing to the market's growth. The versatility of soy-based surfactants, derived from components like soy lecithin, soy fatty acid esters, and soy ether amines, makes them suitable for a wide range of applications, including household detergents, agricultural chemicals, and personal care products. The market's growth is also supported by ongoing research and development efforts to improve the performance and cost-effectiveness of soy-based surfactants. As a result, the global Soy-Based Surfactants market is poised for substantial growth, driven by the increasing demand for sustainable and eco-friendly solutions.

| Report Metric | Details |

| Report Name | Soy-Based Surfactants Market |

| Accounted market size in 2023 | US$ 1822 million |

| Forecasted market size in 2030 | US$ 2662.5 million |

| CAGR | 5.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Saraya, Loveland Products, Noveon, Illionois, Sinerga Cosmetic, Cognic, Akzo Nobel, Koch Industries, Georgia Pacific, ADM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |