What is Global Medical Liposuction Instrument Market?

The Global Medical Liposuction Instrument Market refers to the worldwide industry focused on the production, distribution, and utilization of devices specifically designed for liposuction procedures. Liposuction is a popular cosmetic surgery aimed at removing excess fat from various parts of the body, such as the abdomen, thighs, and arms, to improve body contour and aesthetics. The market encompasses a wide range of instruments, including cannulas, aspirators, and pumps, which are essential for performing these procedures. The demand for these instruments is driven by the increasing prevalence of obesity, rising awareness about body aesthetics, and advancements in surgical techniques. Additionally, the market is influenced by factors such as technological innovations, regulatory approvals, and the growing number of cosmetic surgeries worldwide. The Global Medical Liposuction Instrument Market is characterized by a diverse range of products and services offered by numerous manufacturers and suppliers, catering to the needs of healthcare professionals and patients alike.

Single Pump, Double Pump, Others in the Global Medical Liposuction Instrument Market:

In the Global Medical Liposuction Instrument Market, devices are categorized based on their functionality and design, with Single Pump, Double Pump, and Others being the primary classifications. Single Pump systems are typically used in smaller-scale procedures or in settings where simplicity and ease of use are paramount. These systems consist of a single suction pump that creates the necessary vacuum to remove fat from the body. They are often favored for their cost-effectiveness and straightforward operation, making them suitable for clinics and smaller medical facilities. On the other hand, Double Pump systems are more advanced and are designed for larger-scale procedures or settings that require higher efficiency and precision. These systems feature two suction pumps, which can operate simultaneously or independently, providing greater control and flexibility during the liposuction process. Double Pump systems are often used in hospitals and specialized surgical centers where complex and extensive liposuction procedures are performed. The "Others" category includes a variety of specialized instruments and accessories that complement the primary pump systems. This can include advanced cannulas with different tip designs for specific body areas, power-assisted liposuction devices that use mechanical vibrations to break down fat cells, and laser-assisted liposuction instruments that utilize laser energy to liquefy fat before removal. Each of these instruments offers unique benefits and is chosen based on the specific needs of the procedure and the preferences of the surgeon. The choice between Single Pump, Double Pump, and other specialized instruments depends on various factors, including the complexity of the procedure, the volume of fat to be removed, the patient's anatomy, and the surgeon's expertise. As the demand for liposuction continues to grow, manufacturers are constantly innovating and improving these instruments to enhance their performance, safety, and ease of use. This ongoing development ensures that healthcare professionals have access to the latest and most effective tools for performing liposuction, ultimately benefiting patients by providing better outcomes and a higher standard of care.

Hospital, Clinic, Others in the Global Medical Liposuction Instrument Market:

The usage of Global Medical Liposuction Instruments varies significantly across different healthcare settings, including hospitals, clinics, and other facilities. In hospitals, these instruments are often used in comprehensive surgical departments where a wide range of cosmetic and reconstructive procedures are performed. Hospitals typically have access to the most advanced and sophisticated liposuction instruments, including Double Pump systems and specialized devices, due to their larger budgets and the need to cater to complex cases. These settings also benefit from having multidisciplinary teams of surgeons, anesthesiologists, and other healthcare professionals who can provide comprehensive care to patients undergoing liposuction. Clinics, on the other hand, may focus more on outpatient procedures and often utilize Single Pump systems due to their cost-effectiveness and ease of use. These facilities are typically smaller and may not have the same level of resources as hospitals, but they offer a more personalized and convenient experience for patients seeking cosmetic enhancements. Clinics are popular for their accessibility and shorter recovery times, making them an attractive option for individuals looking for less invasive procedures. The "Others" category includes a variety of settings such as private practices, specialized cosmetic surgery centers, and even some wellness and spa facilities that offer non-surgical fat reduction treatments. These settings may use a combination of traditional liposuction instruments and newer, non-invasive technologies such as laser or ultrasound-assisted devices. The choice of instruments in these settings is often influenced by the specific services offered and the target clientele. For example, a high-end cosmetic surgery center may invest in the latest laser-assisted liposuction devices to attract clients looking for cutting-edge treatments, while a wellness center may focus on non-invasive options that require minimal downtime. Regardless of the setting, the primary goal of using these instruments is to provide safe, effective, and aesthetically pleasing results for patients. The versatility and range of available liposuction instruments allow healthcare providers to tailor their approach to meet the unique needs and preferences of each patient, ensuring a high level of satisfaction and improved quality of life.

Global Medical Liposuction Instrument Market Outlook:

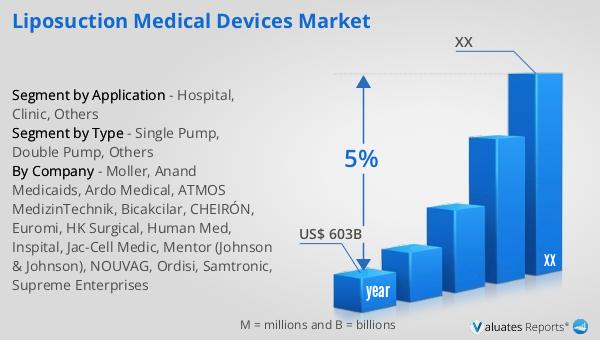

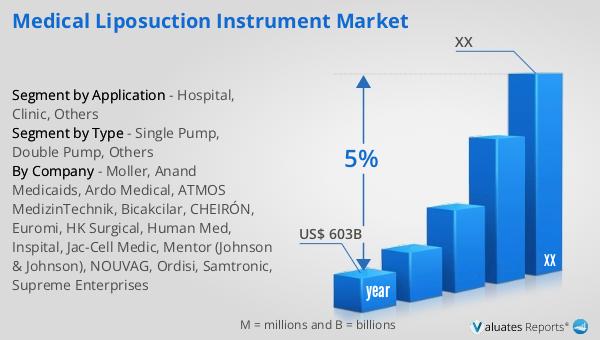

According to our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This significant market size underscores the critical role that medical devices play in modern healthcare, encompassing a wide array of products from diagnostic tools to therapeutic equipment. The steady growth rate reflects ongoing advancements in medical technology, increasing healthcare expenditures, and the rising demand for innovative solutions to address various health conditions. As the population ages and the prevalence of chronic diseases continues to rise, the need for effective and efficient medical devices becomes even more pronounced. This growth trajectory also highlights the importance of regulatory frameworks and quality standards in ensuring the safety and efficacy of medical devices. Companies operating in this market must navigate complex regulatory landscapes and invest in research and development to stay competitive and meet the evolving needs of healthcare providers and patients. The expanding global market for medical devices presents numerous opportunities for innovation and collaboration, driving improvements in patient care and outcomes.

| Report Metric | Details |

| Report Name | Medical Liposuction Instrument Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Moller, Anand Medicaids, Ardo Medical, ATMOS MedizinTechnik, Bicakcilar, CHEIRÓN, Euromi, HK Surgical, Human Med, Inspital, Jac-Cell Medic, Mentor (Johnson & Johnson), NOUVAG, Ordisi, Samtronic, Supreme Enterprises |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |