What is Global Nitrogen Tire Inflator Market?

The Global Nitrogen Tire Inflator Market refers to the industry focused on the production and distribution of devices that inflate tires using nitrogen gas instead of regular air. Nitrogen tire inflators are becoming increasingly popular due to the benefits nitrogen offers over compressed air. Nitrogen molecules are larger and less likely to escape through the rubber of the tire, leading to more stable tire pressure over time. This stability can result in better fuel efficiency, longer tire life, and improved safety. The market encompasses various types of inflators, including manual, semi-automatic, and automatic models, catering to different user needs and preferences. These inflators are used in a variety of vehicles, from passenger cars and motorcycles to buses and trucks. The market is driven by the growing awareness of the benefits of nitrogen inflation, advancements in inflator technology, and the increasing number of vehicles on the road globally. As more consumers and businesses recognize the advantages of nitrogen-filled tires, the demand for nitrogen tire inflators is expected to continue rising.

Manual, Semi-Automatic, Automatic in the Global Nitrogen Tire Inflator Market:

Manual, semi-automatic, and automatic nitrogen tire inflators each offer unique features and benefits, catering to different user needs within the Global Nitrogen Tire Inflator Market. Manual nitrogen tire inflators are the most basic type, requiring the user to manually control the inflation process. These inflators are typically more affordable and straightforward to use, making them suitable for individual car owners or small businesses with limited budgets. They often come with a pressure gauge and a simple valve system, allowing users to monitor and adjust the tire pressure manually. However, the manual process can be time-consuming and requires a certain level of skill and attention to ensure accurate inflation. Semi-automatic nitrogen tire inflators offer a middle ground between manual and fully automatic models. These inflators automate some aspects of the inflation process, such as maintaining a consistent flow of nitrogen and automatically stopping when the desired pressure is reached. This reduces the need for constant monitoring and manual adjustments, making the process more efficient and user-friendly. Semi-automatic inflators are often equipped with digital displays and preset pressure settings, allowing users to easily select the appropriate pressure for their tires. They are ideal for small to medium-sized businesses, such as auto repair shops and tire service centers, that require a balance of affordability and convenience. Automatic nitrogen tire inflators represent the most advanced and user-friendly option within the market. These inflators fully automate the inflation process, requiring minimal user intervention. Users simply need to connect the inflator to the tire and set the desired pressure, and the device takes care of the rest. Automatic inflators are equipped with sophisticated sensors and control systems that ensure precise and consistent inflation, reducing the risk of human error. They often feature advanced digital interfaces, multiple preset pressure options, and the ability to inflate multiple tires simultaneously. These inflators are ideal for large-scale operations, such as commercial fleets, automotive dealerships, and high-volume tire service centers, where efficiency and accuracy are paramount. Each type of nitrogen tire inflator has its own set of advantages and is suited to different applications and user needs. Manual inflators are cost-effective and simple, making them accessible to individual users and small businesses. Semi-automatic inflators offer a good balance of convenience and affordability, making them suitable for small to medium-sized businesses. Automatic inflators provide the highest level of efficiency and accuracy, making them ideal for large-scale operations. As the Global Nitrogen Tire Inflator Market continues to grow, advancements in technology and increasing awareness of the benefits of nitrogen inflation are likely to drive further innovation and adoption of these devices across various sectors.

Passenger Car, Motorcycles, BUS, Trucks, Others in the Global Nitrogen Tire Inflator Market:

The usage of nitrogen tire inflators spans across various types of vehicles, including passenger cars, motorcycles, buses, trucks, and others, each benefiting from the unique advantages of nitrogen inflation. In passenger cars, nitrogen tire inflators are increasingly popular due to the enhanced fuel efficiency and extended tire life they offer. Nitrogen-filled tires maintain a more consistent pressure, reducing the frequency of tire maintenance and improving overall vehicle performance. This is particularly beneficial for everyday drivers who seek to maximize their vehicle's efficiency and safety. Additionally, the use of nitrogen can help prevent tire blowouts, providing an added layer of safety for drivers and passengers. Motorcycles also benefit significantly from nitrogen tire inflators. Motorcycles require precise tire pressure to ensure optimal handling and performance. Nitrogen's ability to maintain stable pressure over time means that motorcycle tires can perform consistently, enhancing rider safety and comfort. This is especially important for high-performance motorcycles used in racing or long-distance touring, where tire performance is critical. The use of nitrogen can also reduce the risk of tire degradation due to moisture, which is a common issue with compressed air. In the context of buses, nitrogen tire inflators play a crucial role in maintaining the safety and efficiency of public transportation. Buses often operate under heavy loads and cover long distances, making tire maintenance a critical aspect of their operation. Nitrogen-filled tires can help reduce the frequency of tire checks and replacements, leading to lower maintenance costs and improved operational efficiency. The consistent tire pressure provided by nitrogen also enhances the safety of buses, reducing the risk of tire-related accidents and ensuring a smoother ride for passengers. Trucks, particularly those used in commercial transportation and logistics, also benefit from the use of nitrogen tire inflators. Trucks often carry heavy loads and travel long distances, making tire performance and maintenance a significant concern. Nitrogen-filled tires can help improve fuel efficiency, reduce tire wear, and lower the risk of blowouts, all of which contribute to the overall efficiency and safety of trucking operations. For fleet operators, the use of nitrogen can lead to significant cost savings in terms of fuel and tire maintenance, as well as reduced downtime due to tire-related issues. Other vehicles, such as agricultural machinery, construction equipment, and recreational vehicles, also benefit from the use of nitrogen tire inflators. These vehicles often operate in demanding environments where tire performance is critical. Nitrogen's ability to maintain stable pressure and reduce the risk of moisture-related tire degradation makes it an ideal choice for these applications. For example, in agricultural machinery, consistent tire pressure can improve traction and reduce soil compaction, leading to better crop yields. In construction equipment, nitrogen-filled tires can enhance stability and safety, reducing the risk of accidents on job sites. Overall, the usage of nitrogen tire inflators across various types of vehicles highlights the versatility and benefits of nitrogen inflation. From passenger cars and motorcycles to buses, trucks, and specialized vehicles, nitrogen tire inflators contribute to improved fuel efficiency, extended tire life, enhanced safety, and reduced maintenance costs. As awareness of these benefits continues to grow, the adoption of nitrogen tire inflators is likely to increase across different sectors, driving further growth in the Global Nitrogen Tire Inflator Market.

Global Nitrogen Tire Inflator Market Outlook:

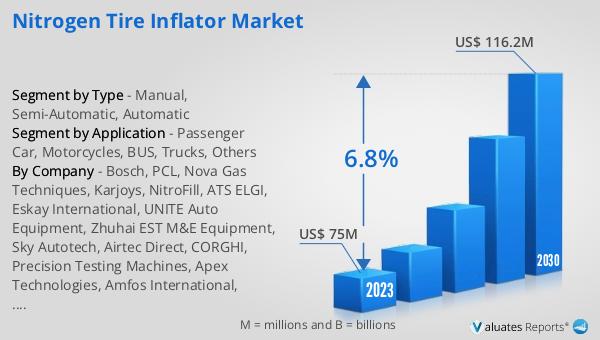

The global Nitrogen Tire Inflator market was valued at US$ 75 million in 2023 and is anticipated to reach US$ 116.2 million by 2030, witnessing a CAGR of 6.8% during the forecast period 2024-2030. This market outlook indicates a robust growth trajectory for the industry, driven by increasing awareness of the benefits of nitrogen inflation and advancements in inflator technology. The projected growth reflects the rising demand for nitrogen tire inflators across various sectors, including automotive, transportation, and logistics. As more consumers and businesses recognize the advantages of nitrogen-filled tires, such as improved fuel efficiency, extended tire life, and enhanced safety, the market is expected to expand significantly. The forecasted CAGR of 6.8% underscores the strong potential for growth and innovation within the industry, as manufacturers continue to develop more advanced and user-friendly inflator models to meet the evolving needs of their customers. This positive market outlook highlights the importance of nitrogen tire inflators in enhancing vehicle performance and safety, and the increasing adoption of these devices across different applications is likely to drive sustained growth in the coming years.

| Report Metric | Details |

| Report Name | Nitrogen Tire Inflator Market |

| Accounted market size in 2023 | US$ 75 million |

| Forecasted market size in 2030 | US$ 116.2 million |

| CAGR | 6.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bosch, PCL, Nova Gas Techniques, Karjoys, NitroFill, ATS ELGI, Eskay International, UNITE Auto Equipment, Zhuhai EST M&E Equipment, Sky Autotech, Airtec Direct, CORGHI, Precision Testing Machines, Apex Technologies, Amfos International, Radiant Automotive Commercial Equipments, Icon Autocraft, Atal Tools, Coburg Equipments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |