What is Global Aircraft Skin Stretch Forming Machines Market?

The global Aircraft Skin Stretch Forming Machines market is a specialized segment within the aerospace manufacturing industry. These machines are used to shape and form the outer skin of aircraft, which is typically made from materials like aluminum and its alloys. The process involves stretching the metal sheets over a form or mold to achieve the desired aerodynamic shape. This technique is crucial for ensuring the structural integrity and aerodynamic efficiency of the aircraft. The market for these machines is driven by the increasing demand for new aircraft, advancements in aerospace technology, and the need for lightweight, durable materials. Manufacturers in this market are focused on developing machines that offer high precision, efficiency, and the ability to handle various types of materials. The market is also influenced by the growing trend towards automation and the use of advanced manufacturing techniques to improve productivity and reduce costs.

Below 800 Tons, 800 Tons-1200 Tons, Above 1200 Tons in the Global Aircraft Skin Stretch Forming Machines Market:

In the Global Aircraft Skin Stretch Forming Machines Market, machines are categorized based on their tonnage capacity, which refers to the maximum force they can exert. Machines with a capacity below 800 tons are typically used for smaller components and less complex shapes. These machines are often employed in the production of smaller aircraft or for parts that do not require extensive forming. They are valued for their precision and ability to handle delicate materials without causing damage. Machines with a capacity between 800 tons and 1200 tons are more versatile and can handle a wider range of components. They are commonly used in the production of medium-sized aircraft and for parts that require more significant forming. These machines offer a good balance between power and precision, making them suitable for a variety of applications. Machines with a capacity above 1200 tons are the most powerful and are used for the largest and most complex components. These machines are essential for the production of large commercial aircraft and military aircraft, where the components need to withstand high levels of stress and strain. They are designed to handle the most demanding forming tasks and are equipped with advanced features to ensure accuracy and efficiency. The choice of machine depends on the specific requirements of the component being produced, including its size, shape, and material properties. Manufacturers in this market are continually working to improve the capabilities of these machines, with a focus on increasing their power, precision, and efficiency. This involves the use of advanced materials, innovative design techniques, and the integration of automation and digital technologies. The goal is to provide machines that can meet the evolving needs of the aerospace industry, ensuring that aircraft are built to the highest standards of quality and performance.

Aluminum Magnesium Alloy, Aluminum Lithium Alloy, Others in the Global Aircraft Skin Stretch Forming Machines Market:

The usage of Global Aircraft Skin Stretch Forming Machines Market extends to various materials, including Aluminum Magnesium Alloy, Aluminum Lithium Alloy, and others. Aluminum Magnesium Alloy is widely used in the aerospace industry due to its excellent strength-to-weight ratio and corrosion resistance. These alloys are particularly suitable for components that need to be lightweight yet strong, such as the outer skin of the aircraft. The stretch forming machines used for these alloys must be capable of handling the specific properties of the material, ensuring that it is formed accurately without compromising its structural integrity. Aluminum Lithium Alloy is another important material in the aerospace industry, known for its high strength and low density. This alloy is used in applications where weight reduction is critical, such as in the construction of fuselage panels and wing skins. The stretch forming machines used for Aluminum Lithium Alloy need to be highly precise and capable of handling the material's unique properties. This includes maintaining the correct temperature and pressure during the forming process to prevent any defects or weaknesses in the final product. Other materials used in the aerospace industry include various advanced composites and high-strength alloys. These materials are chosen for their specific properties, such as high strength, durability, and resistance to extreme temperatures. The stretch forming machines used for these materials must be versatile and adaptable, capable of handling a wide range of material properties and forming requirements. This involves the use of advanced control systems and sensors to monitor and adjust the forming process in real-time, ensuring that the final product meets the required specifications. The ability to work with a variety of materials is a key factor in the success of manufacturers in the Global Aircraft Skin Stretch Forming Machines Market. By offering machines that can handle different materials and forming requirements, manufacturers can meet the diverse needs of the aerospace industry and contribute to the development of more efficient and reliable aircraft.

Global Aircraft Skin Stretch Forming Machines Market Outlook:

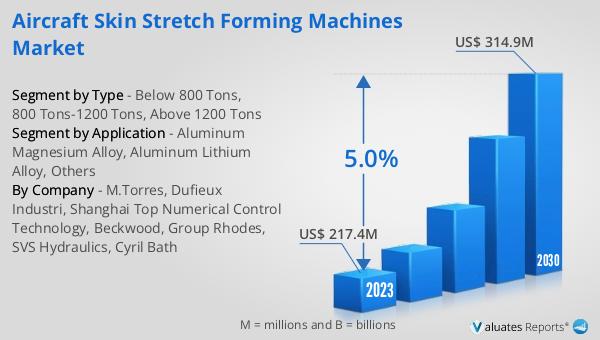

The global Aircraft Skin Stretch Forming Machines market was valued at US$ 217.4 million in 2023 and is anticipated to reach US$ 314.9 million by 2030, witnessing a CAGR of 5.0% during the forecast period 2024-2030. This growth reflects the increasing demand for advanced manufacturing technologies in the aerospace industry. As the industry continues to evolve, there is a growing need for machines that can deliver high precision, efficiency, and versatility. The market is driven by factors such as the rising production of new aircraft, advancements in material science, and the adoption of automation and digital technologies. Manufacturers are focusing on developing machines that can handle a wide range of materials and forming requirements, ensuring that they can meet the diverse needs of their customers. The market outlook is positive, with significant opportunities for growth and innovation in the coming years.

| Report Metric | Details |

| Report Name | Aircraft Skin Stretch Forming Machines Market |

| Accounted market size in 2023 | US$ 217.4 million |

| Forecasted market size in 2030 | US$ 314.9 million |

| CAGR | 5.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | M.Torres, Dufieux Industri, Shanghai Top Numerical Control Technology, Beckwood, Group Rhodes, SVS Hydraulics, Cyril Bath |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |