What is Global Blood Bank Centrifuge Market?

The Global Blood Bank Centrifuge Market refers to the specialized segment within the medical equipment industry that focuses on devices used for the separation of various components of blood. These centrifuges are critical in blood banks and laboratories, where they are utilized to separate blood into its primary components: red blood cells, white blood cells, plasma, and platelets. This separation process is essential for a wide range of medical and research applications, including transfusion medicine, disease diagnosis, and the development of pharmaceuticals. The market for these centrifuges is driven by the increasing demand for blood products, advancements in centrifugation technology, and the growing number of surgeries and medical procedures requiring blood transfusions. Additionally, the rising prevalence of diseases that necessitate blood transfusions, such as anemia and cancer, further propels the demand for blood bank centrifuges. As healthcare systems worldwide continue to evolve and expand, the need for efficient and reliable blood separation technologies becomes increasingly critical, making the Global Blood Bank Centrifuge Market a key area of focus for medical device manufacturers and healthcare providers alike.

3500 rpm, 3500-5000 rpm, 5000-8000 rpm, Over 8000 rpm in the Global Blood Bank Centrifuge Market:

In the Global Blood Bank Centrifuge Market, centrifuges are categorized based on their rotational speed, measured in revolutions per minute (rpm), which is a critical factor in their operation and the efficiency of blood component separation. The categories include 3500 rpm, 3500-5000 rpm, 5000-8000 rpm, and over 8000 rpm. Centrifuges operating at 3500 rpm are typically used for gently separating blood components, minimizing damage to delicate cells, and are suited for basic laboratory applications. The 3500-5000 rpm range represents a versatile class of centrifuges, balancing speed with the integrity of blood components, making them suitable for a broader range of applications in blood processing and clinical laboratories. Centrifuges in the 5000-8000 rpm category are designed for more rapid separation tasks, allowing for quicker processing times which are essential in high-demand settings. These are often used in larger blood banks and research facilities where efficiency and throughput are critical. Lastly, centrifuges operating at over 8000 rpm are at the forefront of high-speed centrifugation technology, enabling ultra-fast separation of blood components for specialized research and high-precision applications. Each speed category serves distinct purposes, catering to the varying needs of medical and research facilities, and reflects the technological advancements and specialization within the Global Blood Bank Centrifuge Market. The choice of centrifuge speed is determined by the specific requirements of the separation process, including the volume of blood to be processed, the desired purity of the separated components, and the urgency of the procedure. As such, the market offers a wide range of centrifugation solutions to meet the diverse needs of healthcare and research institutions worldwide.

Biological, Medicine, Others in the Global Blood Bank Centrifuge Market:

The Global Blood Bank Centrifuge Market finds its applications spread across various fields, notably in biological research, medicine, and other areas. In biological research, these centrifuges are indispensable tools for studying blood-based diseases, developing new treatments, and understanding the fundamental properties of blood and its components. By separating blood into its constituent parts, researchers can isolate specific cells or proteins for detailed analysis, facilitating advancements in biomedical science and contributing to the development of novel therapeutic strategies. In the realm of medicine, blood bank centrifuges play a crucial role in the preparation of blood and blood products for transfusions, a process that saves millions of lives each year. They enable the separation of whole blood into specific components, such as red blood cells, plasma, and platelets, which can be used to treat a variety of conditions, from trauma and surgery to chronic diseases and disorders requiring blood component therapy. Furthermore, these centrifuges are also used in other areas, including veterinary medicine and in the production of nutraceuticals, where the separation of blood components is necessary for diagnostic, therapeutic, or research purposes. The versatility and efficiency of blood bank centrifuges make them a cornerstone of modern healthcare and biomedical research, underscoring their importance in both clinical and non-clinical settings. The ongoing development and refinement of centrifugation technology continue to expand the potential applications of these devices, further solidifying their role in advancing medical science and improving patient care.

Global Blood Bank Centrifuge Market Outlook:

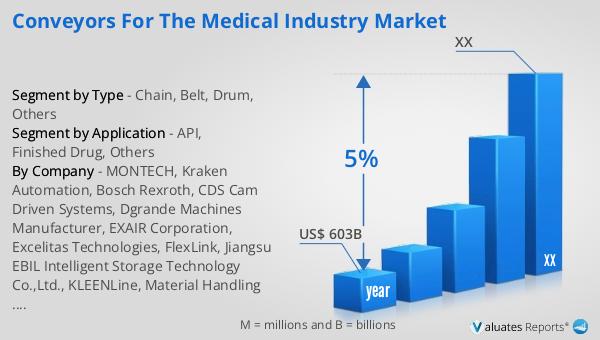

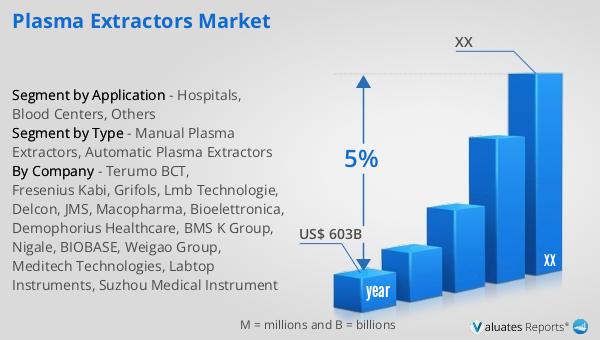

Our research indicates that the global market for medical devices is poised for significant growth, with an estimated value of US$ 603 billion in 2023. This market is expected to expand at a compound annual growth rate (CAGR) of 5% over the next six years. This projection underscores the dynamic nature of the medical device industry, reflecting both the increasing demand for advanced healthcare solutions and the continuous innovation within the sector. The growth is driven by several factors, including the aging global population, rising prevalence of chronic diseases, technological advancements in medical devices, and the growing emphasis on healthcare quality and efficiency. As medical devices become more sophisticated and integrated into patient care, their role in diagnostics, treatment, and patient monitoring becomes increasingly critical. This trend is particularly evident in the development and adoption of cutting-edge devices that offer improved outcomes, greater patient comfort, and enhanced usability for healthcare providers. The forecasted growth of the medical device market signifies a promising outlook for manufacturers, healthcare providers, and patients alike, highlighting the importance of continued investment in research and development to meet the evolving needs of the global healthcare landscape.

| Report Metric | Details |

| Report Name | Blood Bank Centrifuge Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Thermo Scientific, Lepu Medical Technology, Drucker Diagnostics, Sigma, Fanem Ltda, Meditech, Hunan Kecheng Instrument Equipment Co.,Ltd., Labdex Ltd., LABTOP, Sigma Laborzentrifugen, Cardinal Health, Biolab Scientific, KUBOT |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |