What is Global Smart Meter Measurement Chip Market?

The Global Smart Meter Measurement Chip Market is a fascinating sector that's all about the brains behind smart meters. These chips are the heart of smart meters, which are used to measure utilities like electricity, gas, and water in a more sophisticated way than traditional meters. Unlike the old meters that simply recorded consumption, smart meters with these advanced chips can communicate data in real time back to the utility providers. This means better energy management, more accurate billing, and the ability to identify issues quickly. The market for these chips is growing because more countries and companies are looking to upgrade their infrastructure to be smarter and more efficient. As we move towards a more connected and environmentally conscious world, the demand for these smart meter measurement chips is only going to increase. They're a key component in the push towards reducing energy waste and improving service delivery in utilities, making them an essential piece of the global effort to create more sustainable energy systems.

Energy Metering Single Chip, Energy Measurement SoC Chip in the Global Smart Meter Measurement Chip Market:

Diving deep into the Global Smart Meter Measurement Chip Market, we find two main players: the Energy Metering Single Chip and the Energy Measurement SoC (System on Chip). The Energy Metering Single Chip is a marvel of efficiency, designed to accurately measure energy consumption with minimal components. This chip is a game-changer for residential meters, where simplicity and reliability are key. On the other hand, the Energy Measurement SoC Chip is a more complex beast. It's not just about measuring energy; it's about integrating multiple functions and communications capabilities into a single chip. This makes it perfect for commercial and industrial applications where more detailed data about energy usage is needed. Both types of chips are critical in the smart meter market, offering solutions tailored to different needs. The development of these chips is driven by the demand for more efficient energy usage and the need to reduce operational costs. As technology advances, these chips become more sophisticated, offering features like remote monitoring, tamper detection, and even predictive maintenance. This evolution is crucial for the growth of smart grids and the overall improvement of energy management systems worldwide. The innovation in this sector is a testament to the importance of smart technology in our quest for a more sustainable and efficient future.

Residential, Commercial, Industrial in the Global Smart Meter Measurement Chip Market:

The usage of the Global Smart Meter Measurement Chip Market spans across residential, commercial, and industrial sectors, each benefiting uniquely from this technology. In residential areas, these chips help households monitor their energy consumption in real-time, encouraging energy-saving behaviors and allowing for more accurate billing. This not only helps individuals manage their utility costs better but also contributes to the overall energy efficiency of communities. In the commercial sector, smart meter measurement chips offer businesses detailed insights into their energy usage patterns. This can lead to significant cost savings by identifying inefficiencies and peak usage times, allowing for smarter energy management strategies. Moreover, in industrial settings, these chips are indispensable. They provide precise and reliable measurements that are crucial for maintaining the high energy demands of industrial operations. This can help in optimizing production processes and reducing downtime due to energy supply issues. Across all these sectors, the implementation of smart meter measurement chips leads to a more sustainable and efficient use of energy, showcasing the transformative power of this technology in managing the world's energy resources better.

Global Smart Meter Measurement Chip Market Outlook:

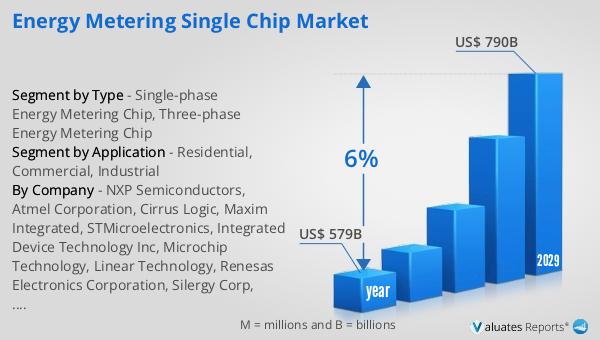

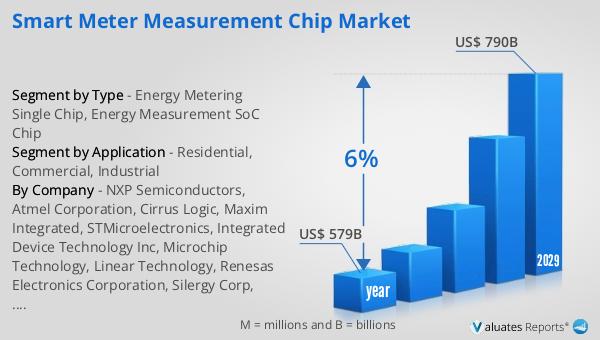

The market outlook for the semiconductor industry, which includes the Global Smart Meter Measurement Chip Market, presents a promising future. In 2022, the industry was valued at approximately 579 billion US dollars. Looking ahead to 2029, it's expected to reach around 790 billion US dollars, marking a growth trend with a Compound Annual Growth Rate (CAGR) of about 6% throughout the forecast period. This growth trajectory underscores the increasing reliance on semiconductor technology across various sectors, including utilities, telecommunications, and consumer electronics, among others. The expansion is driven by the growing demand for smarter, more efficient technology solutions, such as smart meters, which play a crucial role in modernizing and optimizing energy consumption and distribution. As the world continues to push for more sustainable and efficient energy solutions, the role of smart meter measurement chips, as part of the broader semiconductor market, becomes increasingly significant. This outlook highlights not only the robust health of the semiconductor industry but also the pivotal role it plays in supporting global efforts towards more intelligent and sustainable energy management practices.

| Report Metric | Details |

| Report Name | Smart Meter Measurement Chip Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | NXP Semiconductors, Atmel Corporation, Cirrus Logic, Maxim Integrated, STMicroelectronics, Integrated Device Technology Inc, Microchip Technology, Linear Technology, Renesas Electronics Corporation, Silergy Corp, Shanghai Belling Corp.,Ltd. (Renergy), Analog Devices |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |