What is Medical Health Scale - Global Market?

The Medical Health Scale - Global Market refers to the worldwide industry that focuses on the production, distribution, and utilization of medical health scales. These scales are essential tools in healthcare settings, used to measure and monitor patients' weight and other health metrics. The market encompasses a wide range of products, including digital scales, mechanical scales, and specialized scales designed for specific medical purposes. The demand for medical health scales is driven by the increasing emphasis on health and wellness, the rising prevalence of chronic diseases, and the growing need for accurate and reliable health monitoring tools. Technological advancements have led to the development of more sophisticated scales with features like wireless connectivity, data integration, and enhanced precision. The global market is characterized by a diverse range of manufacturers and suppliers, each offering products tailored to different healthcare needs. As healthcare systems worldwide continue to evolve, the Medical Health Scale - Global Market is expected to expand, driven by the need for efficient and effective health monitoring solutions. This market plays a crucial role in supporting healthcare professionals in delivering quality care and improving patient outcomes.

with Armrests, without Armrests in the Medical Health Scale - Global Market:

In the Medical Health Scale - Global Market, products can be categorized based on their design, specifically whether they come with or without armrests. Scales with armrests are particularly beneficial in healthcare settings where patients may require additional support while being weighed. These scales are designed to provide stability and comfort, making them ideal for use with elderly patients, individuals with mobility issues, or those recovering from surgery. The armrests offer a secure grip, reducing the risk of falls and ensuring accurate weight measurements. This feature is especially important in hospitals and physiotherapy centers, where patient safety is a top priority. On the other hand, scales without armrests are more commonly used in settings where space is limited or where the primary focus is on quick and efficient weight measurement. These scales are often more compact and portable, making them suitable for use in households or clinics with limited space. They are also easier to clean and maintain, which is an important consideration in environments where hygiene is critical. The choice between scales with or without armrests often depends on the specific needs of the healthcare facility and the patient population it serves. In hospitals, scales with armrests are frequently used in wards and outpatient departments to accommodate a wide range of patients. They provide the necessary support for patients who may be weak or unsteady, ensuring that weight measurements are both safe and accurate. In contrast, scales without armrests are often found in emergency departments or clinics where speed and efficiency are essential. These scales allow healthcare professionals to quickly assess a patient's weight without the need for additional support features. In physiotherapy centers, scales with armrests are invaluable for patients undergoing rehabilitation. They provide the stability needed for patients who may have difficulty standing unaided, allowing therapists to accurately monitor progress and adjust treatment plans accordingly. The armrests also offer a sense of security for patients, encouraging them to participate more fully in their rehabilitation programs. In household settings, the choice between scales with or without armrests often depends on the needs of the individual or family. For those with elderly family members or individuals with mobility challenges, scales with armrests can provide the necessary support for safe and accurate weight monitoring. These scales can help families keep track of health metrics and ensure that any changes in weight are promptly addressed. For households without such needs, scales without armrests offer a convenient and space-saving solution for regular weight monitoring. In summary, the Medical Health Scale - Global Market offers a variety of products designed to meet the diverse needs of healthcare providers and patients. Whether with or without armrests, these scales play a crucial role in ensuring accurate and reliable health monitoring across different settings. The choice between the two often depends on factors such as patient demographics, space availability, and specific healthcare requirements. As the market continues to evolve, manufacturers are likely to develop new and innovative designs that further enhance the functionality and usability of medical health scales.

Hospital, Household, Physiotherapy Center, Other in the Medical Health Scale - Global Market:

Medical health scales are utilized in various settings, each with its unique requirements and challenges. In hospitals, these scales are indispensable tools for monitoring patient health. They are used in different departments, including wards, outpatient clinics, and emergency rooms, to provide accurate weight measurements that are crucial for diagnosing and managing medical conditions. In addition to weight, some advanced scales can measure other health metrics such as body mass index (BMI), body fat percentage, and muscle mass, providing healthcare professionals with comprehensive data to inform treatment decisions. In households, medical health scales serve as essential tools for individuals and families to monitor their health and wellness. They allow users to track weight changes over time, which can be an important indicator of overall health. For individuals managing chronic conditions such as diabetes or heart disease, regular weight monitoring can help in maintaining a healthy lifestyle and preventing complications. In physiotherapy centers, medical health scales are used to assess patients' progress during rehabilitation. Accurate weight measurements are essential for designing effective treatment plans and monitoring the effectiveness of interventions. Scales with additional features, such as those that measure body composition, can provide valuable insights into a patient's recovery and help therapists tailor their approach to meet individual needs. Other settings where medical health scales are used include gyms, wellness centers, and research facilities. In gyms and wellness centers, these scales help individuals track their fitness progress and set realistic goals for weight management and body composition. In research facilities, medical health scales are used in studies related to health and nutrition, providing accurate data that supports scientific research and contributes to the development of new health interventions. Overall, the usage of medical health scales in these various settings highlights their importance in promoting health and wellness. They provide valuable data that supports healthcare professionals in delivering quality care and empowers individuals to take charge of their health. As technology continues to advance, medical health scales are likely to become even more sophisticated, offering new features and capabilities that enhance their utility across different settings.

Medical Health Scale - Global Market Outlook:

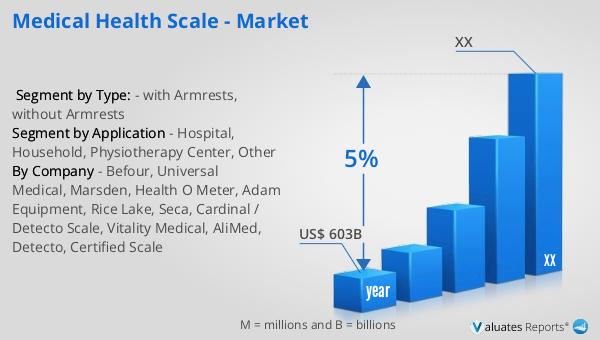

Our analysis indicates that the global market for medical devices, which includes medical health scales, is projected to reach approximately $603 billion by 2023. This substantial market size reflects the growing demand for medical devices worldwide, driven by factors such as an aging population, increasing prevalence of chronic diseases, and advancements in medical technology. The market is expected to grow at a compound annual growth rate (CAGR) of 5% over the next six years, highlighting the steady expansion of the industry. This growth is likely to be fueled by ongoing innovations in medical device technology, as well as increasing investments in healthcare infrastructure and services. The rising awareness of health and wellness among consumers is also contributing to the demand for medical devices, including health scales, as individuals seek to monitor and manage their health more effectively. As the market continues to evolve, manufacturers and suppliers are expected to focus on developing products that meet the diverse needs of healthcare providers and consumers, ensuring that medical devices remain an integral part of the global healthcare landscape.

| Report Metric | Details |

| Report Name | Medical Health Scale - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Befour, Universal Medical, Marsden, Health O Meter, Adam Equipment, Rice Lake, Seca, Cardinal / Detecto Scale, Vitality Medical, AliMed, Detecto, Certified Scale |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |